Syllabus: GS 2/Polity and Governance

In Context

- The recent agitations by the governments of Kerala and Karnataka, and the support extended by several State governments, have highlighted many disquieting issues in the practice of fiscal federalism in India.

Fiscal Federalism in India

- The founding fathers of the Constitution provided that the Centre shall share its tax revenues with the states as well as provide grants from the Consolidated Fund as per a formula decided by the Finance Commission every five years.

- India has a three-tier federal tax system, with the powers of the Centre, states, and local bodies to collect taxes clearly demarcated.

- The Central government has the power to collect taxes on incomes of individuals and businesses, as well as indirect taxes such as the central goods and services tax, integrated goods and services tax, and customs.

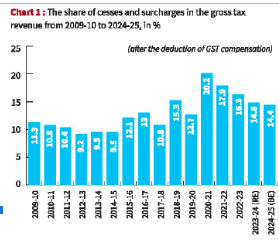

- The Centre also collects surcharges and cesses on taxes.

- States collect state GST, stamp duty, land revenue, state excise, and professional tax.

- Local bodies collect property/house tax, tolls, and taxes on utilities such as electricity and water.

| Constitutional Provisions – The Constitution of India delineates tax bases between the Union and States listing them in the Union List and the State List respectively (as provided in the Seventh Schedule under Art 246). a. There was/is no taxation provision in the Concurrent List. – However, when GST had to be introduced, it needed to be provided for a concurrent base for which Article 246A was inserted (as 101st Amendment in August 2016). a. This enabled the Union to make law for CGST (central GST) and IGST (integrated GST) and the States could legislate for SGST. – Article 270 of the Constitution provides for the scheme of distribution of net tax proceeds collected by the Union government between the Centre and the States. |

Issues Highlights by States

- There are complaints of increasing vertical(sharing of resources between the Union and States ) and horizontal inequalities in devolution.

- The Union government has sought to keep an increasing share of its proceeds out of the divisible pool so that they need not be shared with States.

- It has also not been devolving the shares of net proceeds to the States as mandated by successive FCs.

- Several cesses and surcharges like Agriculture Infrastructure and Development Cess were introduced by the Union government.

- The expansion of cesses and surcharges have led to the exclusion of an increasing share of the gross tax revenue from net proceeds.

- Between 2009-10 and 2023-24, a cumulative total of ₹36.6 lakh crore was collected by the Union government as cesses and surcharges.

- This amount was not shared with States and was used solely by the Union government.

- Cesses and surcharges have also been subjected to critical scrutiny by the CAG.

- the State governments are forced to contribute significantly larger amounts to run the schemes meaningfully.

| Do you know ? – The net divisible pool, or net proceeds, is that part of the gross tax revenue from which a share would have to be vertically devolved by the Union to all States. – Annual estimates of net proceeds can be obtained by deducting cesses, surcharges, and costs of collection of taxes from the gross tax revenue. a. Such shares are assigned by each FC for a five-year period. b. Cesses and surcharges under Article 270 and Article 271 were kept out of the net proceeds. |

Conclusion and Way Forward

- To conclude, sharing of resources from the divisible pool, and the extent of cesses and surcharges, must be matters of critical importance for the 16th FC.

- The FC must take initiative to correct historical wrongs in vertical devolution through compensations to the States.

- It must instruct the Union government to publish accurate estimates of “net proceeds” in the budget documents.

- It must also arrange to provide shortfalls in devolution over the last decade as a lump sum untied grant to States.

- On its part, the Union government must legislatively act to have strict limits on the collection of cesses and surcharges; cesses and surcharges should automatically expire after a short period and must not be rechristened under another name.

- It is also imperative that the States uphold principles of fiscal federalism by devolving adequate resources to local bodies for vibrant and accountable development.

| Mains Practice Question [Q] What are the grievances raised by various states in India regarding Tax devolution?Is India’s fiscal federalism breaking apart?How the stance of the 16th Finance Commission (FC) would be critical to the survival of fiscal federalism in India? |

Previous article

The Global Order and Role of United Nations

Next article

Legalising the Minimum Support Price (MSP)