Syllabus: GS2/Health/GS3/Indian Economy

In Context

- Credit rating agency ICRA has released a research report on the Indian hospital industry.

Key Highlights of the Report

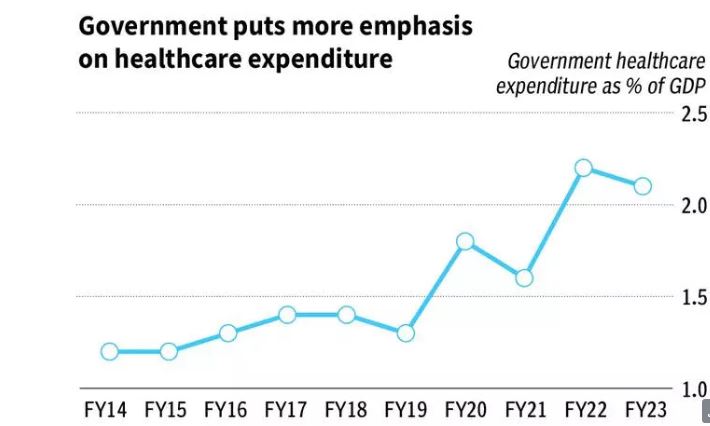

- Post Covid, the government healthcare expenditure has increased from 1.2-1.4 percent to 1.6-2.2 percent of GDP.

- Average revenue per occupied bed day (ARPOB) increased from ₹34,277 to ₹49,836 during FY20-H1 FY24.

- India has one of the lowest per capita bed counts in the world.

Healthcare Sector of India

- Healthcare Sector: It comprises hospitals, medical devices, clinical trials, outsourcing, telemedicine, medical tourism, health insurance and medical equipment.

- India’s healthcare delivery system is categorised into two major components – public and private.

- Public Sector: It comprises limited secondary and tertiary care institutions in key cities and focuses on providing basic healthcare facilities in the form of Primary Healthcare Centers (PHCs) in rural areas.

- Private Sector: The private sector provides the majority of secondary, tertiary, and quaternary care institutions with a major concentration in metros, tier-I, and tier-II cities.

- Medical Tourism: India ranks 10th in Medical Tourism Index (MTI) for 2020-2021 out of 46 destinations in the world.

- Future Projection: The hospital sector in India was valued at INR 7940.87 Bn in FY21 in terms of revenue & is expected to reach INR 18,348.78 Bn by FY 2027, growing at a CAGR of 18.24%.

- The Indian medical tourism market was valued at US$ 2.89 billion in 2020 and is expected to reach US$ 13.42 billion by 2026.

Major Challenges Faced by Healthcare Sector in India:

- Lack of infrastructure: India has been struggling with deficient infrastructure in the form of lack of well-equipped medical institutes.

- The government mandated that private medical colleges must be built on at least five acres of land hence, they were built in rural areas, where there was a lack of adequately qualified, full-time doctors due to living conditions, besides low pay scales.

- The National Medical Commission (NMC) has put forward the idea to do away with the requirement of minimum five acres of land.

- Shortage of Efficient and Trained Manpower: There is a severe shortage of trained manpower, this includes doctors, nurses, paramedics and primary healthcare workers.

- The doctor-to-patient ratio remains low, which is merely 0.7 doctors per 1,000 people whereas the World Health Organisation (WHO) average is 2.5 doctors per 1,000 people.

- Population Density and Demographics: The sheer size and diversity of the population pose unique challenges in providing healthcare services to all.

- Aging population and the associated increase in chronic diseases add to the healthcare burden.

- High out-of-pocket Expenditure: While public hospitals offer free health services, these facilities are understaffed, poorly equipped, and located mainly in urban areas leaving no alternatives but to access private institutions and incurring high out-of-pocket expenses in healthcare.

- Disease Burden: High prevalence of communicable diseases (such as tuberculosis) and the increasing burden of non-communicable diseases (like diabetes, cardiovascular diseases) pose a dual challenge.

- Every year, roughly 5.8 million Indians die from heart and lung diseases, stroke, cancer and diabetes.

- Lack of Diagnostic Services: The penetration of diagnostic services in India is mainly concentrated around metros and big cities.

- Shortage of hygiene infrastructure, lack of awareness, limited access to facilities, lack of trained medical personnel, dearth of medicines and good doctors are the challenges faced by more than 70 percent of India’s population living in rural areas.

- Public-Private Partnership Issues: Challenges in fostering effective collaboration between the public and private sectors in healthcare.

- Ensuring that the private healthcare sector serves the larger public health goals.

Measures Needed for India to become Global Healthcare Provider:

- Increase in Public Spending: India’s healthcare spending is 3.6% of GDP, including out-of-pocket and public expenditure.

- India spends the least among BRICS countries: Brazil spends the most (9.2%), followed by South Africa (8.1%), Russia (5.3%), China (5%).

- Infrastructure Development: Invest in building and upgrading healthcare infrastructure, including hospitals, clinics, and research facilities.

- Healthcare Education and Training: Strengthen medical education and training programs to produce skilled healthcare professionals.

- Research and Innovation: Foster a culture of research and innovation in healthcare. Provide incentives for pharmaceutical and biotech companies to conduct research and develop new treatments.

- Telemedicine and Digital Health: Promote the use of telemedicine and digital health solutions to increase access to healthcare services, especially in rural areas.

- Regulatory Reforms: Streamline and simplify regulatory processes to facilitate faster approval of drugs, medical devices, and healthcare technologies.

- Ensure a transparent and efficient regulatory framework.

- Public-Private Partnerships (PPPs): Encourage collaborations between the government, private sector, and non-profit organizations to leverage resources and expertise.

- Health Insurance and Financing: Implement and expand health insurance schemes to provide financial protection to citizens.

- Develop innovative financing models to fund healthcare projects and initiatives.

- Disease Prevention and Health Promotion: Focus on preventive healthcare measures to reduce the burden of diseases.

- Quality Standards and Accreditation: Establish and enforce stringent quality standards for healthcare services.

- Encourage healthcare facilities to obtain international accreditation to enhance their credibility.

- Medical Tourism Promotion: Develop and promote medical tourism by offering high-quality healthcare services at competitive prices.

- Improve visa and travel infrastructure to attract patients from other countries.

Recent steps Taken by the Government for the Growth of Healthcare Sector

- National Digital Health Mission (NDHM): Launched in 2020, NDHM aims to create a digital health ecosystem, including health IDs for citizens and the establishment of a national digital health infrastructure.

- Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY): AB-PMJAY, launched in 2018, is a national health protection scheme that provides financial protection to over 100 million families for secondary and tertiary care hospitalization.

- National Health Policy 2017: The National Health Policy outlines the government’s vision to achieve the highest possible level of health and well-being for all and emphasizes preventive and promotive healthcare.

- Health and Wellness Centers (HWCs): The government is working towards transforming primary health centers into HWCs to provide comprehensive primary healthcare services, including preventive and promotive care.

- Pradhan Mantri Swasthya Suraksha Yojana (PMSSY): PMSSY aims to enhance tertiary care capacities and strengthen medical education in the country by setting up new AIIMS (All India Institutes of Medical Sciences) institutions and upgrading existing government medical colleges.

- Research and Development Initiatives: The government has been encouraging research and development in healthcare, including support for the development of vaccines, drugs, and medical technologies.

- National Medical Commission (NMC) Act: The NMC Act, passed in 2019, aims to bring reforms in medical education and practice by replacing the Medical Council of India (MCI) and promoting transparency and accountability.

- Jan Aushadhi Scheme: The Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP) aims to provide quality generic medicines at affordable prices through Jan Aushadhi Kendras.

Way Ahead

- There is a need to adopt technology wherever possible to streamline the operational and clinical processes for healthcare facilities in order to manage efficient patient flow.

- In addition, there is the challenge to think beyond the obvious and promote virtual care protocols, and telehealth services, which can be leveraged to reduce the patient-load burden to a large extent.

- To sum it up, there is an urgency to make healthcare service and service providers more transparent operationally.

- This will help ensure people and processes can be made easily accountable to provide better healthcare services.

Source: BL

Previous article

Distressing Agriculture Sector

Next article

Changing Role of Civil Society