Syllabus: GS3/Economy

Context

- Kunal Shah, India’s prominent fintech entrepreneur has been appointed as global CEO of WhatsApp.

About

- The Meta is also investing $900 million in CRED, raising concerns over US technology companies gaining increasing control over India’s fintech sector and data generated by Indian consumers.

- The Meta-CRED transaction comes at a time when India’s digital-payments ecosystem is increasingly dominated by platforms linked to US firms.

- Walmart controls about 72% of PhonePe, Google owns Google Pay and Meta owns WhatsApp Pay.

- The proposed CRED investment would further strengthen the control of foreign technology giants in a sector built largely on Indian public digital infrastructure.

- Many Indian fintech startups appear more interested in building companies for eventual sale to foreign buyers than in creating long-term Indian-owned digital champions.

What is Fintech?

- The fintech sector in India refers to the use of technology to enhance, innovate, and streamline financial services.

- This sector encompasses a wide range of financial products and services, including digital payments, lending, insurance, wealth management, and personal finance, all powered by technology.

Fintech Sector in India

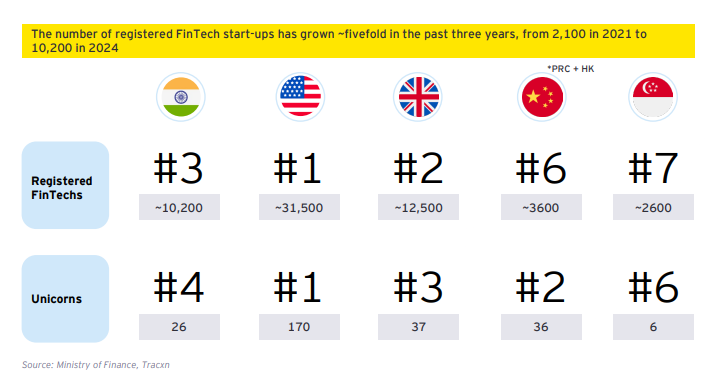

- The Indian fintech industry is estimated to be around USD 110 billion in 2024 and is projected to reach about USD 420 billion by 2029.

- India ranks 3rd globally, in number of FinTechs and is the Global Leader in digital payment volumes.

- From just 1 Mn transactions in 2016, UPI has since crossed the landmark 10 Bn transactions.

Growth Drivers

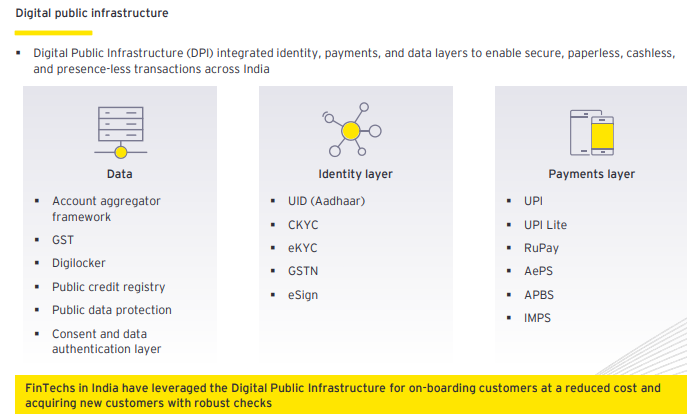

- Digital Infrastructure: Open Application Programming Interface (API) Platforms i.e. Aadhar, UPI, Bharat Bill Payments, GSTN.

- Technological Innovation: Implementation of new business models driven by technologies such as Artificial Intelligence and Machine Learning

- Favourable Demographics: 62% of urban and 37% of rural adults use the internet. Smartphone penetration surpassed 50% in 2024, with a 2.5x growth in the last seven years.

- Financial Inclusion Initiatives: Financial inclusion programmes such as PMJDY, DAY-NRLM, Direct Benefit Transfer, Atal Pension Yojana among others have accelerated the digital revolution and brought more citizens, especially in rural areas, within the ambit of digital financial services.

Challenges

- Cybersecurity Risks: The increasing use of digital platforms raises concerns about data breaches and cyberattacks.

- Ensuring robust security measures to protect sensitive financial data is crucial.

- Lack of Digital Literacy: A significant portion of the population still lacks digital literacy and access to technology, which limit the reach and effectiveness of fintech solutions.

- Customer Trust: Building trust in digital financial services, especially among older demographics and those new to technology is challenging.

- Policy Changes: Changes in economic or financial policies, including taxation and interest rates majorly affect the fintech ecosystem.

- Innovation and Scalability: Keeping pace with rapid technological advancements and ensuring that systems can scale effectively as user demand grows is a tough challenge.

Government Initiatives for Fintech Sector in India

- Pradhan Mantri Jan Dhan Yojana (PMJDY): Aims to increase financial inclusion by facilitating the enrollment of new bank accounts for direct benefit transfers and access to financial services.

- India Stack: A societal initiative to build public digital infrastructure that supports both public and private digital initiatives, particularly in the finance sector.

- Aadhaar Enabled Payment System (AePS): Allows individuals to conduct financial transactions using their Aadhaar number and biometric verification (fingerprint or iris scan) on Micro-ATMs.

- Central KYC (Know Your Customer): A central repository designed to reduce the need for multiple KYCs across different financial institutions.

- Unified Payments Interface (UPI): A scalable platform that supports digital payments across India.

- Bharat Bill Payment System (BBPS): Enhances consumer convenience by enabling bill payments across various utilities and sectors, covering all recurring billers except prepaid recharges.

- Self-Regulatory Organisation (SRO) for Fintech: RBI has recognized Fintech Association for Consumer Empowerment as an SRO for the fintech sector.

- It strengthens industry standards, compliance, and consumer protection.

- National Digital Health Mission (NDHM) and Related Initiatives: Government-led efforts, including NDHM and DISHA, aim to transform the insurance and healthcare sectors through digital infrastructure.

- Regulatory Sandbox: Introduced by the Reserve Bank of India and later by International Financial Services Centres Authority.

- Allows fintech firms to test innovative products in a controlled regulatory environment before full-scale deployment.

- Fintech Hub at IFSC, GIFT City: A world-class fintech hub developed in Gandhinagar, Gujarat, to promote India as a global fintech leader.

Conclusion

- The fintech sector in India is vibrant and rapidly evolving, playing a significant role in the country’s financial ecosystem by enhancing accessibility, efficiency, and inclusion.

Source: IE

Previous article

Union Government Tightens FCRA Rules for NGOs