In News

- Recently, the government has approved extending a guarantee of Rs 30,600 crore to the National Asset Reconstruction Company Ltd (NARCL) to help clear the banking sector’s stressed assets of around Rs 2 lakh crore in a time-bound manner.

Key Points

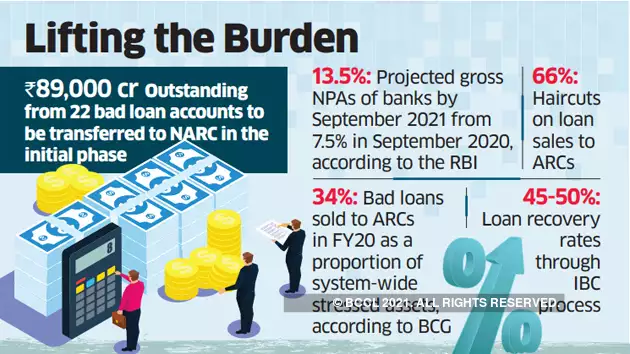

- A total of Rs 90,000 crore of stressed assets, against which banks have made 100 percent provisions in their books of accounts, will be transferred to NARCL in the first phase.

- The India Debt Resolution Company Ltd has already been set up and will function as the asset management company.

- Ownerships: Public sector banks will have a 51% ownership in the NARCL, while their shareholding along with that of public sector financial institutions will be capped at 49% for the IDRC, with private lenders bringing in the rest of the equity capital.

- Government’s Guarantee:

- The GoI Guarantee of up to Rs 30,600 crore will back Security Receipts (SRs) issued by NARCL. The guarantee will be valid for 5 years.

- If the bad bank is unable to sell the bad loan, or has to sell it at a loss, then the government guarantee will be invoked.

- The guarantee shall cover the shortfall between the face value of the SR and the actual realisation.

- A 15% cash payment would be made to the banks based on some valuation and the rest (85%) will be given as security receipts.

- Need for Guarantee:

- Resolution mechanisms of this nature which deal with a backlog of NPAs typically require a backstop from the Government.

- This imparts credibility and provides for contingency buffers.

- It will support the regulatory provisioning requirement of the RBI.

- The Finance Minister stated that the meticulous execution of the 4 Rs — Recognition, Resolution, Recapitalisation and Reforms — strategy since 2015 had served the banking system well.

- In the last six fiscal years, banks had made recoveries of ?5.01-lakh crore with as much as ?3.1-lakh crore since March 2018. In 2018-19, banks recovered a record ?1.2-lakh crore.

Significance of Move

- Growth Capital: Most of the big-ticket NPAs (Non Performing Assets) will be transferred to NARCL, thereby cleaning up banks’ balance sheets and freeing up growth capital for them to support economic activity.

- Clean & Transparent: This will result in banks’ balance sheets and books being cleaner, transparent, they will now be able to stand on their own and do business.

- Positive step: The government guarantee for the proposed security receipts is a positive stepping stone for unlocking stressed assets’ value. A guarantee helps in improving the value of security receipts, their liquidity and tradability.

- Inbuilt Incentives: There is an inbuilt incentive structure within the overall framework that will drive both banks and NARCL to ensure resolution of the bad loans within a period of 5 years.

- Quicker Resolution: The recent moves include elements that have been missing in the functioning of the existing ARCs and hence, the large assets that have hitherto been left unaddressed will see resolution going ahead.

- Completing Cycle: Since 2015, resolution, recovery of NPAs, healthy capital infusion has been done alongside a series of reforms to resurrect the public sector banks. NARCL is completing the entire cycle of cleaning up India’s banking system that began with the recognition of the extent of bad loans in 2015.

|

National Asset Reconstruction Company Ltd (NARCL)

India Debt Resolution Company Ltd. (IDRCL)

Benefits of NARCL-IRDCL Setup

|

Issues with NPA

- Needs Provisioning: The bad loans lead to banks’ having to save a part of their operating revenue to account for bad loans. This is called Provisioning. The technical term used for provisioning is Capital Adequacy Ratio (CAR) or Capital to Risk (weighted) Assets Ratio (CRAR).

- Loss of Profit: The banks are required to provision for bad loans out of their operating income. The concerned bank becomes less profitable because it has to use some of its profits from other loans to make up for the loss on the bad loans.

- Becomes Risk-averse: The officials of such banks hesitate from extending loans to business ventures that may remotely appear risky for the fear of aggravating an already high level of non-performing assets (or NPAs).

- Affects Valuation: Any reduction in the perceived valuation of the banks might lead to loss of share value of the banks, leading to general downfall in the share markets. This could result in wiping out shareholders’ wealth from the financial markets.

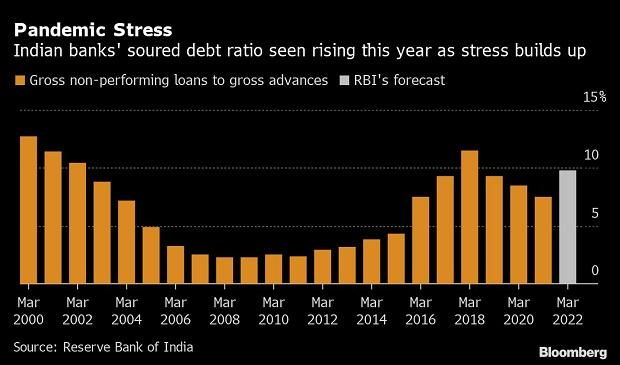

- Rising Bad Loans: In spite of various efforts, a substantial amount of NPAs continue on balance sheets of banks primarily because the stock of bad loans as revealed by the Asset Quality Review is not only large but fragmented across various lenders.

(Image Courtesy: BS )

Various Steps Taken for NPA

- Insolvency and Bankruptcy Code (IBC);

- Strengthening of Securitization and Reconstruction of Financial Assets and Enforcement of Securities Interest (SARFAESI Act) and Debt Recovery Tribunals;

- Setting up of dedicated Stressed Asset Management Verticals (SAMVs) in banks for large-value NPA accounts etc.

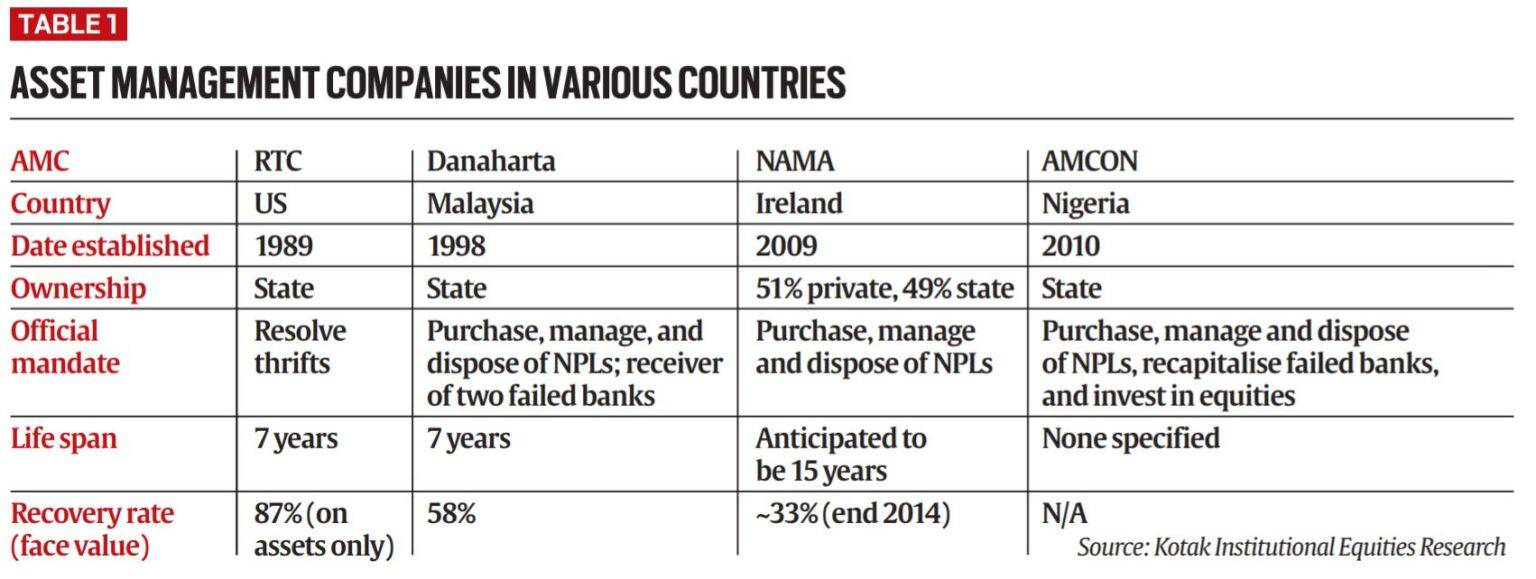

- Existing ARCs have been helpful in resolution of stressed assets especially for smaller value loans.

- However, considering the large stock of legacy NPAs, additional options/alternatives are needed and the NARCL-IRDCL structure announced in the Union Budget is this initiative.

Bad Bank

- An Asset Reconstruction Company (ARC) or Bad Bank is a specialized financial institution which buys stressed assets from banks and financial institutions.

- Asset reconstruction is the purchase of title or rights of the banks or financial institutions in loans, bonds, debentures, etc., for the sole purpose of its recovery or realization.

- Banks can sell their stressed or bad assets to the ARC at a mutually agreeable price, thereby helping banks to clean up their balance sheets and concentrate on delivering normal banking services.

- Thereafter, it is the responsibility of the ARC to recover the bad debts or associated securities in a market-led process.

Need for Bad Bank

- Enhanced Lending: A bad bank can take over the bad loans of the bank, thereby freeing up the bank from the provisioning requirements. This means since the banks are not required to provision for the bad loans, the same money can be utilised for lending purposes.

- Revival of Credit: The more money banks have, the more they can advance to the needy. This is useful for the revival of the credit cycle and boosting investments in the economy.

- More Recovery: A bad bank would be specialised in maximising the recovery out of a bad loan, as this would be its primary task.

- Impetus to Industry : A bad bank can provide an impetus to the industry by freeing up the books of banks.

- Decreases Recapitalisation Needs: Recapitalisation of banks is required to fulfill the capital adequacy ratio of the banks. With the formation of a bad bank, it is expected that this amount can be utilised elsewhere, including towards public welfare and infrastructure creation.

- Mitigating Slowdown: Reports have pointed to a potential increase in stressed assets due to economic slowdown in India. To resolve such a situation, it is necessary to work out a solution which can be optimised to reverse the effects of slowdown in the country.

Image Courtesy: ET

Concerns With the Bad Bank

- Incomplete Solution: A bad bank is expected to take over the debts of commercial banks under itself. Therefore, the bad bank can only be expected to aggregate, but not resolve the problem.

- Huge Expenditure: A huge amount is needed for setting up a bad bank. In the times of global recession as well as COVID-induced lockdown, this might prove to be tricky for the government as it is already pressed to provide for increased healthcare costs and is constrained by decreasing revenues.

- Banks Management: The haircuts taken by the banks would reflect on its profit and loss account and affect its profitability. This might raise questions on both the management of the bank as well as its decision making regarding both earlier and future haircuts.

- Rise in Unethical Practices: The employees might turn towards unethical practices to boost recovery out of a bad loan. This has been a continuing problem earlier as there have been reports of harassment of the banks’ clients, who were unable to pay their dues.

Conclusion

- The sovereign guarantee would allow the banks to free up the capital without the burden of additional provisioning, effectively allowing more participation from the banks to resolve their NPAs through the bad bank.

- However, the success of the bad bank will depend on the implementation and management of the transferred NPAs.

|

Non Performing Asset (NPA)

Types of NPA

Image Courtesy: IE Background of Bad Bank

Difference Between ARCs and ?IBC

|

Previous article

15th East Asia Summit of Energy Ministers

Next article

Sea Cucumber