In News

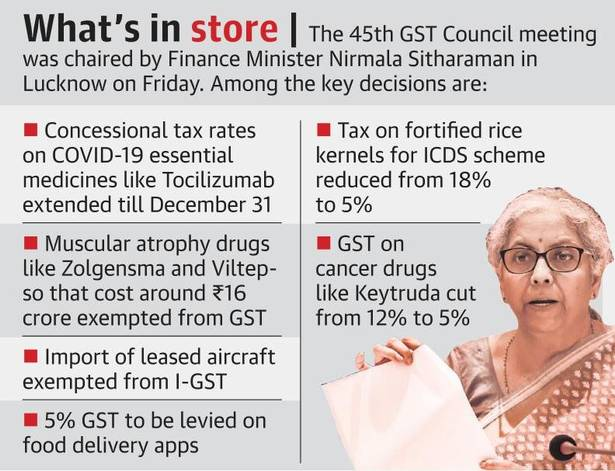

Recently, the GST Council’s 45th meeting was held in Lucknow under the chairmanship of the Union Finance Minister.

Key Decisions

- Drugs:

- Life-saving drugs Zolgensma and Viltepso used in treatment of Spinal-Muscular Atrophy are exempted from GST when imported for personal use.

- Extension of existing concessional GST rates on certain COVID-19 treatment drugs upto 31st December 2021

- GST rates on 7 other medicines recommended by Department of Pharmaceuticals reduced from 12% to 5% till 31st December 2021

- GST rate on Keytruda medicine for treatment of cancer reduced from 12% to 5%

- Special abilities people’s requirements:

- GST rates on Retro fitment kits for vehicles used by persons with special abilities reduced to 5%

- Petroleum products:

- Petroleum products will be out of the GST regime.

- Import:

- Import of leased aircraft exempted from IGST. This will help the aviation industry avoid double taxation.

- Goods supplied at Indo-Bangladesh border haats have also been exempted from GST.

- The Council also decided to remove GST on the import of muscular atrophy drugs like Zolgensma and Viltepso, which cost crores of rupees.

- Rice kernels:

- GST rates on Fortified Rice kernels for schemes like ICDS reduced from 18% to 5%

- Footwear:

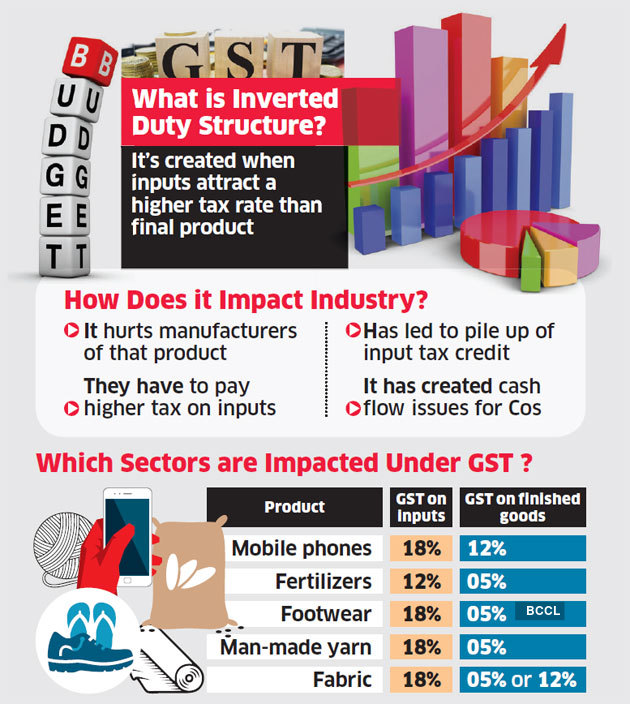

- GST on footwear costing less than Rs.1000 and ready-made garments and fabrics have increased to 12% from 5%.

- It will come into effect from January 1st and will be done to correct inverted duty structure in footwear and textiles sector, as was discussed in earlier GST Council Meeting and was deferred for an appropriate time.

- Bricks:

- Bricks would attract GST at the rate of 6% without input tax credits under the scheme, or 12% with input credits.

- Automobiles:

- Consumers will have to keep paying the Compensation Cess levied on products like automobiles till March 2026 instead of July 2022 as originally envisaged at the time of rolling out the indirect tax regime.

- No relaxation:

- There was also indication that the Union government is not inclined to consider some States’ demand to extend the five-year period for which they have been assured a 14% revenue growth for giving up several taxation powers to pave the way for implementing the GST regime.

- Two Group of Ministers (GoM):

- To shore up GST revenues, the Council has decided to form two groups of ministers (GoMs) that have to recommend measures within two months.

- They will be setup to examine issue of correction of inverted duty structure for major sectors and for using technology to further improve compliance, including monitoring

- The first one has been tasked with reviewing tax rate rationalisation issues to correct anomalies in the rate structure

- The other will look to tap technology to improve compliance and monitoring. It will look at e-way bills, Fastags, compliance and composition schemes to plug loopholes.

- They will be setup to examine issue of correction of inverted duty structure for major sectors and for using technology to further improve compliance, including monitoring

- To shore up GST revenues, the Council has decided to form two groups of ministers (GoMs) that have to recommend measures within two months.

- Food delivery apps:

- It also decided to make food delivery apps like Swiggy and Zomato liable to collect and remit the taxes on food orders, as opposed to the current system where restaurants providing the food remit the tax.

- This will essentially shift the responsibility of paying the 5 per cent GST to the aggregators from the restaurants.

Image Courtesy: TH

Inverted duty structure

- Definition:

- An inverted duty structure comes up in a situation where import duties on input goods are higher than on finished goods.

- In other words, the GST rate paid on purchases is more than the GST rate payable on sales.

- What is Inverted Duty Structure under GST?

- Under GST, inverted duty structure means inputs (inward supplies) used are having a higher GST rate compared to the GST rate of finished goods (outward supplies).

- In simple terms, it means the GST rate for raw materials has a higher tax rate whereas the GST rate on finished goods is lower.

- Problems with the current inverted duty structure under GST:

- Taxpayers will have accumulated credits in the form of refund claims with the tax Department.

- The inverted duty structure is a revenue loss for the government as it has to refund the tax already paid (in inputs).

- Under GST, the inverted duty structure is identified for goods and not for services. Or in other words, there is recognition for ‘input good’ and not for ‘input services’.

(Image Courtesy: ET )

- Impact on business:

- Businesses paying taxes under this structure continue to have Input Tax Credit in their ledger even after paying off the output tax liability, leading to crucial working capital remaining stuck in the form of credit.

- There is confusion about central laws not providing for any refund of credit accumulation on account of differential tax rates, particularly when the rate of tax on inputs is more than rate of tax on output.

- Services sectors such as hotels and hospitality have pointed out to Section 54(3) of the CGST Act, which states that unutilized ITC can be claimed, but the tax department does not consider the unutilized ITC on services while calculating “Net ITC” as per Rule 89(5) of CGST Rules.

- Hence, there is confusion on whether a taxpayer is eligible to claim a refund of unutilised ITC on input services or not. Thus, the businessmen want it to be abolished.

Recent Concerns with GST

- Less Revenue: While the GST regime had originally been premised on a revenue-neutral tax rate of 15.5%, the actual GST revenues had been going down with the effective tax rate slipping to 11.6% due to changes made in the tax rates on various goods and services over the last few years.

- Increased Borrowings: In 2020-21, the Centre had borrowed ?1.1 lakh crore on behalf of States to bridge the shortfall in the GST Compensation Cess collections that arose due to the COVID-19 pandemic, but some arrears are still pending. Similar borrowings have also been made this year of about ?75,000 crore, with another ?83,000 crore more estimated over the remaining part of the year.

- Exclusion of Petroleum Products: The consensus in the Council to keep petroleum products and natural gas outside the GST regime, was contrary to the expectations of the general public. The Council discussed that it is not the right time to include petroleum products under GST.

- Impact on Consumers: The GST Compensation Cess would have to be extended beyond July 2022 till March 2026 in order to repay the principal and interest on the back-to-back borrowings raised to meet the GST compensation shortfall for States. It is expected to impact consumers as the same will be recovered from them.

Way Ahead

- The GST Council should work towards an enabling, conducive, predictable, and transparent environment which promotes inclusiveness.

- To promote investment and growth, changes in taxation policy should be transparent and predictable. There should be no vacuum of uncertainty.

- The tax rates have to be harmonious and sustainable to ensure the success of cooperative fiscal federalism in India.

|

GST Council

|

Sources: TH

Previous article

‘Reforms in Urban Planning Capacity in India’ : NITI Aayog

Next article

Inspiration4 Mission