Syllabus:GS3/Economy

In Context

- India’s rural credit ecosystem has grown substantially over the years.

Evolution of Rural Credit System

- In the post-Independence period, the Government and the Reserve Bank of India (RBI) undertook key initiatives to strengthen institutional credit.

- 1955: The National Agricultural Credit (Long-term Operations) Fund was created and the State Bank of India was established. These initiatives marked a major step towards expanding rural banking and strengthening agricultural finance.

- 1969: 14 major commercial banks were nationalised. It reoriented banking policies towards priority sectors, particularly small farmers, which enhanced the flow of institutional credit to rural areas.

- 1982: NABARD was established, strengthening the rural credit architecture.

- It integrated financing, developmental, and supervisory functions for agriculture and rural development.

- It also promotes financial inclusion, prepares district credit plans and supports Government initiatives aimed at expanding access to formal finance.

- 1992: The Self-Help Group (SHG)-Bank Linkage Programme was introduced which expanded access to formal credit for rural households.

- 1998: The Kisan Credit Card (KCC) Scheme improved the availability of timely and affordable credit for farmers.

- 2014: Pradhan Mantri Jan Dhan Yojana (PMJDY) was launched to expand financial inclusion through universal banking access, supporting credit, insurance and Direct Benefit Transfers.

- It forms a key pillar of the JAM (Jan Dhan–Aadhaar–Mobile) Trinity. This has transformed the delivery of welfare benefits through digitally enabled, transparent and targeted service delivery.

- 2015: The MUDRA Scheme (PMMY) was launched to provide collateral-free institutional credit to non-corporate, non-farm small and micro enterprises. This promotes rural entrepreneurship and self-employment.

- 2022 onwards: Digital initiatives such as the Jan Samarth Portal, e-KCC and others have transformed rural credit delivery through technology-enabled, accessible and inclusive financial services.

Institutional Architecture of Rural Credit

- Scheduled Commercial Banks (SCB): A SCB is a bank included in the Second Schedule of the RBI Act, 1934. These banks are eligible for loans at the bank rate from the RBI and are members of the clearing house.

- They deliver banking services through branches, Business Correspondents, digital platforms, and Government initiatives such as PMJDY and Direct Benefit Transfer (DBT).

- SCBs include public sector banks, private sector banks, foreign banks, payment banks, regional rural banks and small finance banks.

- Progress: At present, around 120 SCBs are providing banking services across the country.

- In rural areas, there were 41,464 SCB branches in 2014. This increased by over 35% to 56,193 rural branches by July 2025, playing a vital role in rural credit delivery.

- They deliver banking services through branches, Business Correspondents, digital platforms, and Government initiatives such as PMJDY and Direct Benefit Transfer (DBT).

- Regional Rural Banks (RRBs) : RRBs were established under the RRB Act, 1976, with the objective of strengthening institutional credit in rural areas.

- They focus particularly on small and marginal farmers, agricultural labourers, artisans, and small entrepreneurs.

- They have played a critical role in promoting rural development and financial inclusion.

- Currently, 28 RRBs operate across States and Union Territories, having a branch network of over 22,000 in 700 districts.

- Co-operative Banks: The co-operative banking system forms an integral part of India’s financial system, with separate urban and rural segments.

- Small Finance Banks (SFB): SFBs were introduced following the Union Budget 2014–15. Licensed by RBI, SFBs aim to promote financial inclusion by providing accessible and secure savings facilities.

- They particularly focus on the unserved and underserved sections of the population.

- SFBs extend credit to small businesses, small and marginal farmers, micro industries, and other entities in the unorganised sector.

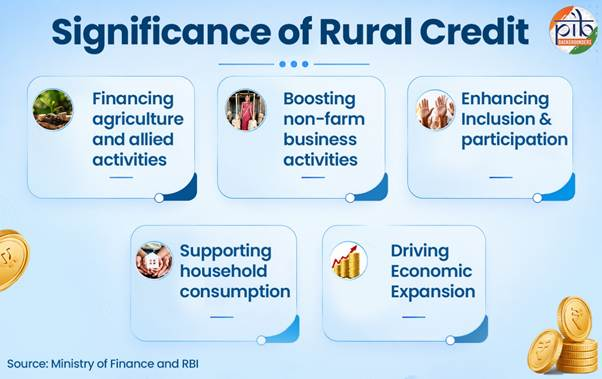

Importance of India’s Rural Credit Ecosystem

- Supports agricultural production and food security: Crop loans, investment credit for irrigation, farm mechanisation, dairy, fisheries and horticulture enable farmers to purchase inputs and boost productivity.

- Promotes financial inclusion: SHG–Bank Linkage pioneered by NABARD and supported by RBI, links low income rural households particularly women to the formal banking system.

- Reduced reliance on informal lenders: Institutional credit is offered at regulated interest rates and offers formal protection to borrowers than traditional moneylenders.

- Funds rural infrastructure and non-farm growth: Rural Credit directs resources to roads, irrigation, bridges and other infrastructure

Current Issues

- Unequal access to formal credit: Small and marginal farmers face difficulties in getting institutional loans in time resulting in regional disparities in credit flow.

- High transaction costs and documentation burden: The lending in rural areas is expensive and time consuming due to the dispersed borrowers, land-record issues and procedural requirements.

- Credit concentration in crop loans: Short term crop finance is more developed than long term investment credit for irrigation, mechanisation, storage and allied sectors.

- Regional Imbalance: Some of the eastern and central states receive less institutional agricultural credit than the southern and western states.

- Lack of Awareness: Some rural borrowers have low financial literacy and digital capability, which can limit the effective use of formal credit channels.

- Monsoon Dependency: Agriculture remains highly vulnerable to weather shocks, increasing the riskiness of farm lending and generating repayment stress and periodic loan restructuring.

Policy Framework for Rural Credit

- Priority Sector Lending (PSL): Priority Sector Lending (PSL) is a mandatory framework set by the RBI.

- It requires banks to allocate a specific percentage of their total loans to critical or underserved sectors of the economy that struggle to access formal credit.

- At least 18% of their Adjusted Net Bank Credit or Credit Equivalent of Off-Balance Sheet Exposures, whichever is higher, must be earmarked for this purpose.

- Ground Level Credit (GLC): The Government sets annual GLC targets for agriculture and allied sectors, which banks must achieve each financial year.

- These targets are set region-wise, agency-wise, and by loan category, including crop and term loans.

- Self Help Group (SHG): The Self-Help Group–Bank Linkage Programme (SHG-BLP), was initiated by NABARD. It was launched to connect rural Self-Help Groups (SHGs) with the formal banking system & enabling access to affordable institutional credit.

- Primary Agricultural Credit Societies (PACS): PACS are the grassroots-level institutions of the short-term cooperative credit structure. They directly interact with rural borrowers, providing loans and facilitating repayment.

- PACS also undertakes distribution and marketing functions for agricultural inputs and produce.

- Modified Interest Subvention Scheme (MISS): MISS is a central sector scheme ensuring the availability of short-term credit to farmers at affordable interest rates through KCC.

- Under the scheme, farmers receive short-term loans at a subsidised interest of 7%, with 1.5% subvention provided to lending institutions. Farmers repaying loans promptly are eligible for an additional incentive of up to 3%, reducing the interest rate to 4%.

- The Union Budget 2025–26 introduced several measures to strengthen MISS.

- Enhanced the loan limit under the MISS from ₹3 lakh to ₹5 lakh for loans availed through KCC.

- The lending limit for fisheries and allied activities increased from ₹2 lakh to ₹5 lakh.

- From January 2025, the limit for collateral-free short-term agricultural loans increased from ₹1.6 lakh to ₹2 lakh per borrower.

- PM Dhan Dhanya Krishi Yojana (PM-DDKY): PM-DDKY approved in July 2025, aims to catalyse growth in 100 low performing agri-districts.

- It adopts a saturation-based convergence of 36 Central schemes across 11 Ministries. A key objective of the scheme is to enhance access to short-term and long-term agricultural credit for farmers

- Kisan Credit Card: It offers features such as an ATM-enabled debit card and one-time documentation.

- Pradhan Mantri Jan Dhan Yojana (PMJDY): It provides universal banking access through at least one basic account per household of marginalized communities.

- Jan Samarth Portal: Launched in June 2022, it is a one-stop digital platform to link Government-sponsored loan and subsidy schemes, including KCC.

- Jan Dhan Darshak App: It enables citizens to locate banking service points, including bank branches, ATMs, Bank Mitras and Common Service Centres (CSCs), across the country.

Conclusion

- India’s rural credit system has transitioned from an informal structure to a diversified, institution-led and policy-driven framework. The system has reinforced rural prosperity to timely and affordable credit across agriculture and allied sectors.

- RRBs, cooperatives and NABARD have expanded institutional credit but the problems of unequal access, poor governance of cooperatives and inadequate financing for long-term investments persist.

- Strengthening institutions, digitisation and targeted investment in rural areas are key to sustainable rural growth.

Source :PIB

Previous article

Digitisation in Criminal Justice System in India

Next article

News In Short 16-07-2026