In News

- Recently, Banks have invoked the Sarfaesi Act against telecom infrastructure provider GTL to recover their pending dues.

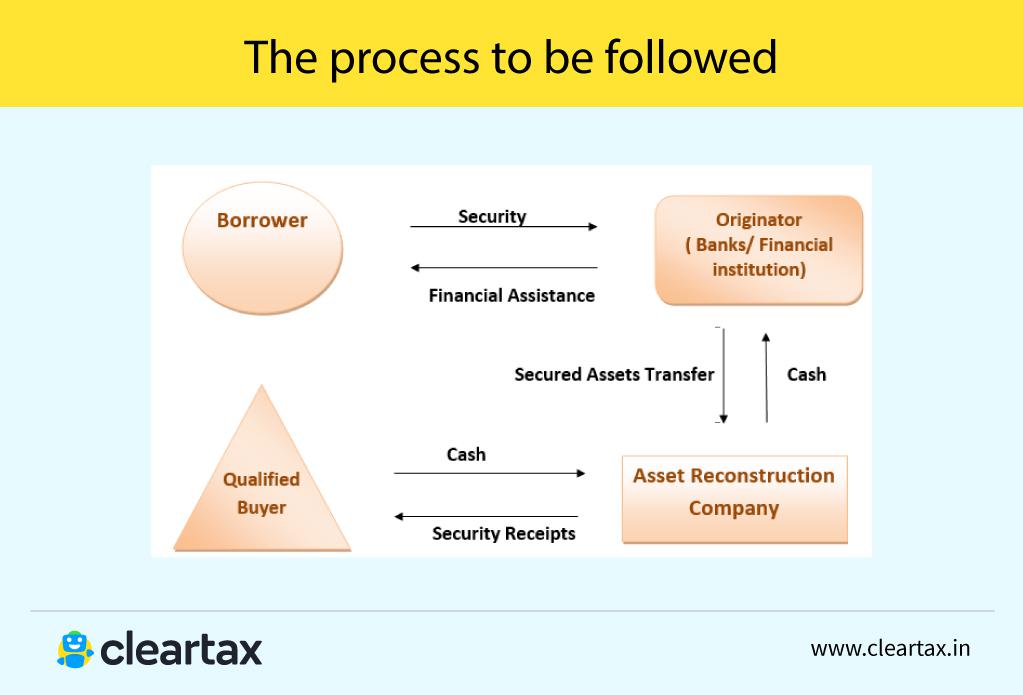

About Sarfaesi Act

- Term:

- It is termed as Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (Sarfaesi) Act.

- Aim:

- It was brought in to guard financial institutions against loan defaulters.

- Taking control of the secured assets

- Take over management of the secured assets, as well as the right to transfer the secured assets via lease, assignment, or sale

- Designate someone to administer the secured assets

- To recover their bad debts, the banks under this law can take control of securities pledged against the loan, manage or sell them to recover dues without court intervention.

- Coverage:

- Co-operative banks can also invoke Sarfaesi Act.

- The non-banking financial companies (NBFCs) can initiate recovery in Rs 20 lakh loan default cases.

- Application:

- The law is applicable throughout the country and covers all assets, movable or immovable, promised as security to the lender.

- Powers:

- The Act comes into play if a borrower defaults on his or her payments for more than six months.

- The lender then can send a notice to the borrower to clear the dues within 60 days.

- In case that doesn’t happen, the financial institution has the right to take possession of the secured assets and sell, transfer or manage them.

- The defaulter, meanwhile, has recourse to move an appellate authority set up under the law within 30 days of receiving a notice from the lender.

- Modes of recovery under the SARFAESI Act

- Securitisation

- Asset reconstruction

- Enforcement of security without the interruption of the court

Image Courtesy: Cleartax

|

Related committees

|

Issues/ Shortcomings

- Unsecured creditors: One of the Act’s significant flaws is that it does not apply to unsecured creditors.

- The bank has no influence over what happens to the asset after it is placed up for auction: If there are no buyers for the asset at the auction, the bank cannot proceed, pursuant to the previous conditions.

- Not useful: the Government of India added a new clause in 2011 declaring that the bank might acquire the asset if there was no better bidder. However, if it was in an extremely remote place, it was useless to the bank.

- No remedy: The Act’s provision permitted the bank to keep a specific asset for a maximum of seven years. However, if the bank does not get a reasonable bid within the specified time frame, the remedy for such a situation is not specified in the Act.

What is the need? / Significance

- Lengthy route: Before the law was enacted in December 2002, banks and other financial institutions were forced to take a lengthy route to recover their bad debts.

- Slow recovery: The lenders would appeal in civil courts or designated tribunals to get hold of security interests to recovery of defaulting loans, which in turn made the recovery slow and added to the growing list of lender’s non-performing assets.

- Co-operative banks: Considering their size, for the smooth functioning of these co-operative banks, speedy recovery of defaulting loans is critical.

- Allowing co-op banks recourse to the SARFAESI Act can expedite the process of liquidation or resolution.

- Promotion of seamless transferability of financial assets by the ARC to acquire financial assets of banks and financial institutions through the issuance of debentures or bonds or any other security as a debenture.

- Entrusting the Asset Reconstruction Companies to raise funds by issue of security receipts to qualified buyers.

Way Forward

- Improve the fundamentals: Experts have consistently pointed to the need for improving the examination process during the initial stages of the lending process. Usually the cause of bad loans has been traced to reckless lending undertaken by the banks to meet their lending targets.

- Asset Quality Review: While the spike in NPAs was a result of RBI-mandated Asset Quality Review, it is to be understood that the process was a mere recognition of the extent of the problem facing the financial sector of India. It is important to gauge the extent of the issue if corrective actions are expected to yield results.

- Firm steps required to address the crisis: Government has emphasised on the ‘4R strategy’ to yield result in the resolution of the NPA crisis. It constitutes Recognition of NPAs, Resolution of bad loans and recovery of value from the assets, Recapitalisation of the banks by the government and Reforms in the banking sector.

- Government has also come up with various other schemes like Indradhanush plan and Gyan sangam (meeting between government officials and the bank officials to understand and resolve the issues plaguing banking sector.

|

Insolvency and Bankruptcy Code:

Bad bank

|

Source: IE

Previous article

Labour Codes

Next article

World Population Prospects Report 2022