Syllabus: GS3/ Economy

Context

- On 1 July 2026, the Goods and Services Tax (GST) completed nine years since its rollout under the 101st Constitutional Amendment.

Nine Years of GST: Key Outcomes

- Formalisation of the Economy: GST has expanded India’s formal economic base. The number of registered taxpayers has increased from around 66.5 lakh in 2017 to nearly 1.65 crore by May 2026.

- Strong Revenue Performance: Tax collections have grown steadily over the years. Gross GST revenue increased from approximately ₹7.4 lakh crore in 2017–18 to ₹22.27 lakh crore in 2025–26.

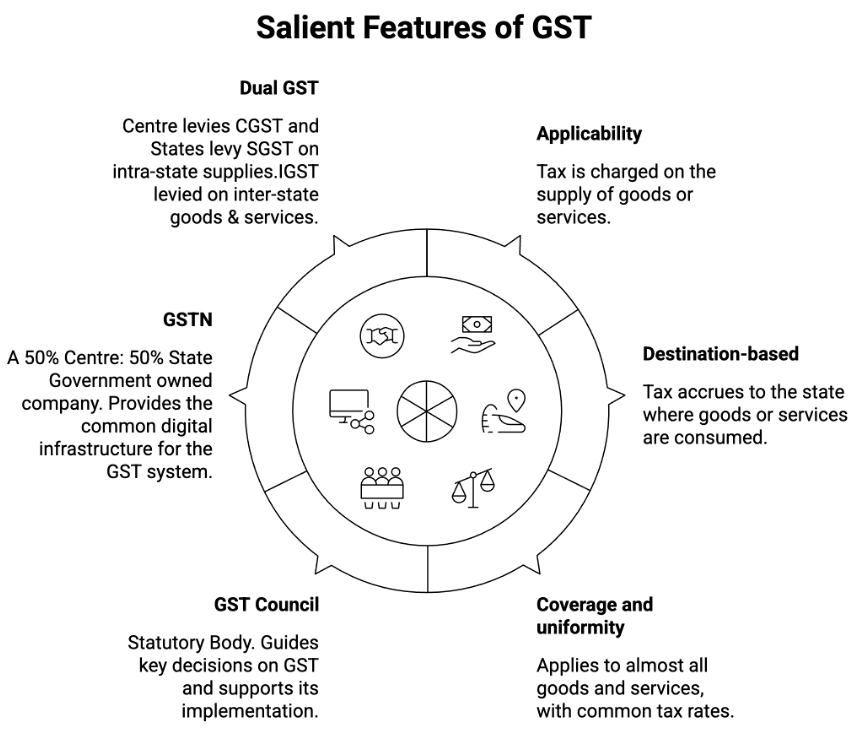

- Towards a Unified National Market: By replacing 17 different Central and State indirect taxes, GST created a common national market and substantially reduced the cascading effect of taxation which strengthen the idea of “One Nation, One Tax”.

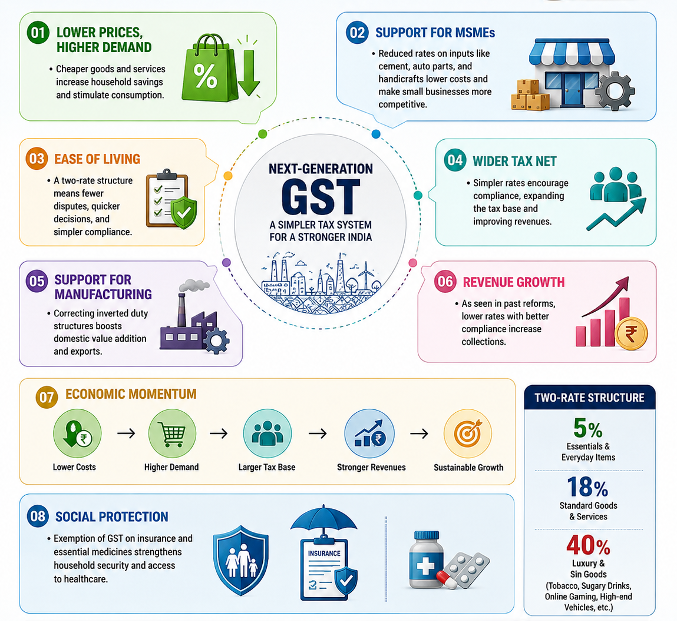

GST 2.0: Major Reforms

- Rationalisation of Tax Rates: Under this, the earlier four-rate system of 5%, 12%, 18% and 28% has largely been consolidated into two principal slabs of 5% and 18%.

- Also, a new 40% rate has been introduced for luxury and demerit goods.

- Household Relief:Essentials like UHT milk (tetra pack), paneer, roti, and erasers have been moved to Nil (0%) GST. Common household items like soap, toothpaste, kitchenware are placed in the 5% bracket.

- Healthcare and Insurance: Life and health insurance products are GST-exempt, and rates on essential drugs and medical devices have been reduced.

- Sectoral Support: GST 2.0 reforms specifically address the Inverted Duty Structure affecting key sectors.

- Institutional Strengthening: The Goods and Services Tax Appellate Tribunal (GSTAT) become operational to enable faster dispute resolution.

Next-Gen GST: Benefits

Challenges

- Revenue Foregone: Rate reductions could lead to a revenue loss of approximately ₹48,000 crore on FY 2023-24 consumption base (Finance Ministry), requiring compensatory base broadening.

- ITC Removal Concerns: Removal of ITC on healthcare products and insurance could increase costs for businesses providing these services, partially offsetting consumer relief.

- Petroleum Exclusion: Keeping petroleum outside GST perpetuates cascading tax effects on logistics and manufacturing, undermining GST’s core efficiency objective.

- Transitional Compliance Burden: Despite rationalisation, businesses face pricing structure adjustments and billing system upgrades during transition, creating short-term operational complexity.

- Concerns of States: Several states continue to express concerns over possible revenue losses following the end of the GST compensation mechanism and the latest rate rationalisation.

- Moderating Revenue Growth: Although GST collections continue to reach record levels in absolute terms, the pace of year-on-year growth has moderated. This has raised questions about the long-term sustainability of revenue buoyancy and the need to further widen the tax base.

Way Forward

- AI Integration: Develop AI-driven invoice matching and real-time ITC verification to combat fake invoice fraud, protecting revenue without burdening compliant taxpayers.

- Strengthen Cooperative Federalism: Sustained engagement through the GST Council remains essential for addressing state-level revenue concerns and ensuring that future reforms enjoy broad consensus.

- Broaden the GST Base: Expanding the tax base would improve revenue buoyancy, simplify the indirect tax structure and move India closer to a truly comprehensive GST regime.

- Faster Dispute Resolution: Fast-track GSTAT operationalisation across all 45 locations to resolve pending disputes and restore taxpayer confidence in the GST dispute resolution architecture.

Source: PIB

Previous article

Fiscal Tightrope for State Governments

Next article

News In Short 01-07-2026