Syllabus: GS3/Economy

Context

- The proposed Insolvency and Bankruptcy Code (IBC) Amendment, 2026 introduced the Creditor-Initiated Insolvency Resolution Process (CIIRP) aimed at faster resolution of stressed assets while preserving enterprise value.

- However, its restriction of initiation rights to select ‘notified financial institutions’ has triggered debates on fairness, constitutionality, and efficiency.

Evolution of India’s Insolvency Framework

- Pre-IBC Era:

- Sick Industrial Companies Act (SICA), 1985 adopted a debtor-in-possession model through the Board for Industrial and Financial Reconstruction (BIFR).

- The framework suffered from excessive delays, litigation, and misuse by promoters seeking to avoid repayment obligations.

- Subsequent mechanisms such as the SARFAESI Act, 2002 and the Debt Recovery Tribunals (DRTs) improved recovery but lacked a comprehensive resolution framework.

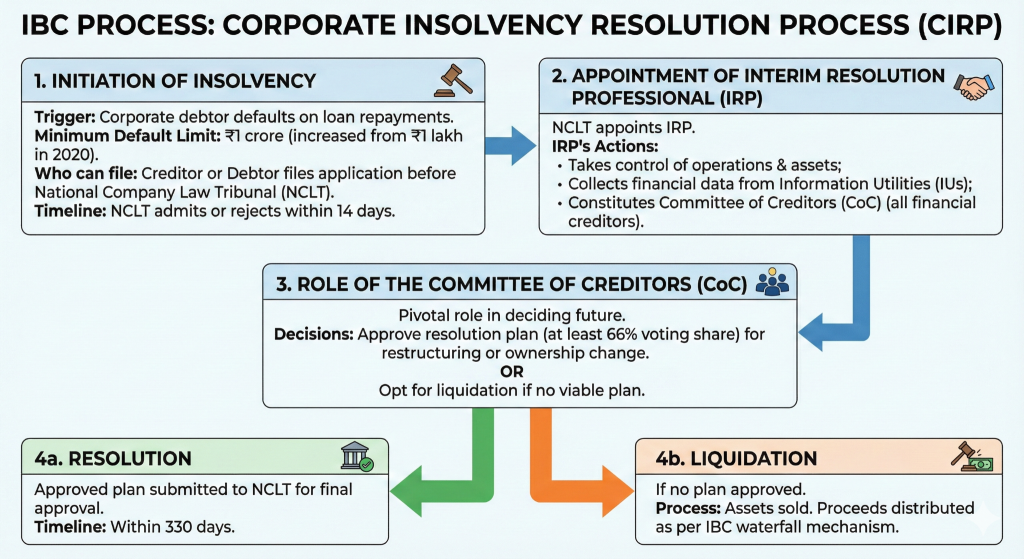

- IBC, 2016: It introduced a creditor-in-control model, established a time-bound insolvency process under the supervision of the National Company Law Tribunal (NCLT).

- It prioritised value maximisation, creditor recovery, and ease of doing business, and recognised globally as a major structural reform.

Need for the IBC 2026 Amendment

- Major Drivers: Prolonged resolution timelines beyond statutory limits, value erosion of stressed firms during insolvency proceedings, excessive judicial intervention, and need for a restructuring mechanism that preserves business continuity.

- The amendment seeks to provide a faster and less disruptive alternative for companies facing temporary financial stress.

Key Features of the IBC 2026 Amendment

- Introduction of CIIRP: It establishes a Creditor-Initiated Insolvency Resolution Process (CIIRP) through new provisions (Sections 54C–54P). It designed as a hybrid framework combining elements of both:

- Debtor-in-possession, where existing management continues operations.

- Creditor oversight, through supervision by a resolution professional.

- Preservation of Enterprise Value: Avoids abrupt displacement of management, enables continuity of business operations during restructuring, and reduces the risk of value destruction often associated with traditional insolvency proceedings.

- Reduced Procedural Delays: Encourages restructuring before financial distress escalates into liquidation, and limits unnecessary judicial intervention.

- Clarification of Admission Standards: Replaces the discretionary term ‘may’ with ‘shall’ in the relevant admission provision.

- Makes admission mandatory once debt and default are established through Information Utility records, and enhances predictability and certainty for creditors.

- Restricted Eligibility: Only ‘notified financial institutions’ can initiate the CIIRP. It is the most debated aspect of the amendment.

Key Concerns in 2026 Amendment and the Overall IBC Framework

- Constitutional Concerns under Article 14: The amendment creates a distinction within the class of financial creditors.

- The Supreme Court, in 2019, upheld differentiation between financial and operational creditors based on ‘intelligible differentia’.

- However, differentiating between notified and non-notified financial creditors may be difficult to justify.

- Concentration of Power: Bargaining power becomes concentrated in the hands of a few notified institutions.

- Smaller lenders and non-notified creditors may lose meaningful participation in restructuring negotiations.

- Disadvantage to Operational Creditors: Operational creditors already occupy a weaker position in the repayment waterfall.

- CIIRP may further marginalise their interests.

- Risk of Strategic Behaviour: Creditors excluded from CIIRP may resort directly to the more aggressive CIRP mechanism.

- It could increase disputes and undermine the objective of consensual restructuring.

- Continuing Challenges within IBC: Beyond the amendment, broader concerns i.e. judicial delays, capacity constraints in NCLTs, shortage of insolvency professionals, low recovery in certain sectors, and frequent litigation affecting resolution timelines remain.

Global Practices: Lessons for India

- United States: Strong debtor-in-possession framework; existing management generally retains control; access is based on financial distress rather than the identity of creditors; and encourages broad stakeholder participation.

- United Kingdom: Focuses on restructuring viable businesses, permits participation of different creditor classes, and uses objective financial criteria instead of regulatory status.

- India’s Divergence: India’s proposed framework restricts initiation rights to a select group of institutions unlike these systems. Such an approach may:

- Reduce investor confidence;

- Create perceptions of regulatory favoritism;

- Discourage participation by non-traditional lenders and foreign investors.

Way Forward: Strengthening Measures

- Adopt a Universal CIIRP Framework: Allow any financial creditor to initiate CIIRP.

- Require support from creditors representing at least 51% of total financial debt.

- Ensures broad legitimacy while preventing frivolous filings.

- Use a Default-Neutral Initiation Rule: Base eligibility on objective financial exposure rather than institutional identity.

- Enhances constitutional robustness.

- Strengthen NCLT Capacity: Increase benches and judicial resources, and improve disposal rates and reduce pendency.

- Protect Minority and Operational Creditors: Ensure transparency in negotiations, and introduce safeguards against exclusion from restructuring decisions.

- Promote Pre-Packaged and Early Restructuring Mechanisms: Encourage resolution before financial distress becomes irreversible, and preserve employment, assets, and enterprise value.

- Improve Information Infrastructure: Strengthen Information Utilities and digital insolvency processes, and reduce disputes regarding debt and default.

| Daily Mains Practice Question [Q] Examine the significance of the proposed Insolvency and Bankruptcy Code (IBC), 2016 Amendment introducing the Creditor-Initiated Insolvency Resolution Process (CIIRP). Discuss its potential benefits, constitutional concerns, and the need for a more inclusive insolvency framework. |

Previous article

Equality of Treatment for Persons With Disabilities

Next article

India–France Partnership 2.0