Syllabus: GS3/Economy

Context

- The Government of India has introduced tax exemptions and investment-related reforms for Foreign Institutional Investors (FIIs) and Foreign Portfolio Investors (FPIs) investing in Government Securities (G-Secs).

About FIIs and FPIs

- Foreign Institutional Investment (FII) is a category of FPI that refers specifically to investments made by foreign institutional investors such as mutual funds, pension funds, insurance companies, and hedge funds. These institutions invest pooled funds in financial markets and typically play a more active role in investment research and decision-making.

- Foreign Portfolio Investment (FPI) refers to investments made by foreign individuals, institutional investors, or funds in financial instruments such as stocks, bonds, mutual funds, and government securities. FPIs do not participate in the management or decision-making of the companies in which they invest and are generally considered passive investors.

What are Government Securities (G-Secs)?

- Government Securities (G-Secs) are tradable debt instruments issued by the Central or State Governments to borrow funds and meet their expenditure requirements.

- They represent the government’s debt obligation and are generally considered risk-free as they carry a sovereign guarantee.

- G-Secs are broadly classified into:

- Treasury Bills (T-Bills): Short-term securities with a maturity of less than one year.

- Government Bonds/Dated Securities: Long-term securities with a maturity of one year or more.

- In India, the Central Government issues both Treasury Bills and Government Bonds, while State Governments issue long-term securities known as State Development Loans (SDLs).

What changes have been introduced?

- Prior to the latest reform, Foreign Institutional Investors (FIIs), including SEBI-registered Foreign Portfolio Investors (FPIs), were taxed under Section 210 of the Income-tax Act, 2025.

- Any income earned from investments in Government Securities (G-Secs) was subject to tax. Specifically:

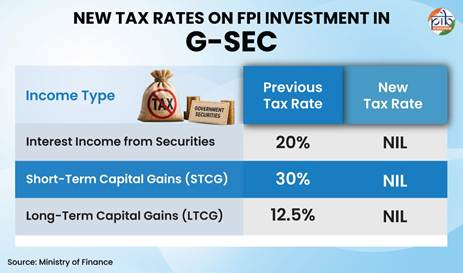

- Interest income earned on G-Secs was taxed at 20% for FIIs/FPIs.

- Short-term capital gains arising from the sale of G-Secs were taxed at 30%, depending on the nature of the transaction.

- Long-term capital gains were taxed at 12.5%.

- As a result, a portion of the returns earned by foreign investors from holding or trading G-Secs was payable as tax in India.

- Under the new regime, FPIs/FIIs will be exempt from:

- Interest income earned from G-Secs; and

- Capital gains arising from the sale, transfer, exchange or redemption of G-Secs.

- The exemption will apply to income arising on or after 1 April 2026 under the Income-tax (Amendment) Ordinance, 2026.

Significance of the Reforms

- Attracting Long-Term Foreign Capital: Experts estimate that the measures could bring $45–50 billion in additional foreign inflows over the next two years.

- Deepening the Bond Market: As of May 2026, FPIs held Government Securities worth about ₹3.75 lakh crore, accounting for 3.34% of the total outstanding G-Sec stock. Greater participation can improve market liquidity, price discovery, and trading activity.

- Lowering Government Borrowing Costs: Increased demand for Government Securities can reduce yields and lower borrowing costs for the government.

- Supporting Infrastructure and Development Financing: Additional capital can support infrastructure, manufacturing, renewable energy, and urban development projects.

- Strengthening External Sector Stability: Higher foreign inflows can support the Balance of Payments (BoP), strengthen foreign exchange reserves, and reduce pressure on the rupee.

Potential Challenges

- Volatility of Portfolio Flows: Unlike Foreign Direct Investment (FDI), FPI investments are highly sensitive to global interest rates, geopolitical tensions, and risk sentiment. A rise in US interest rates or global financial uncertainty can trigger sudden withdrawals from emerging markets, including India.

- Risk of Capital Flight: While increased foreign participation can deepen the bond market, sudden outflows may lead to sharp movements in bond yields and exchange rates. This could increase borrowing costs and put pressure on the rupee.

- Limited Impact on Structural Issues: Tax exemptions may improve the attractiveness of Indian Government Securities, but they may not fully address concerns related to currency volatility, fiscal deficits, or broader investor confidence.

Conclusion

- The reforms mark a significant step towards deepening India’s debt market and enhancing its attractiveness to global investors.

- By simplifying market access, expanding investment opportunities, and improving tax competitiveness, the Government aims to attract stable long-term capital while strengthening the resilience and efficiency of India’s financial system.

- This could support economic growth, improve market development, and further integrate India with global capital markets.

Source: PIB

Previous article

8th India-Indonesia Joint Commission Meeting

Next article

India’s Cotton Mission and Challenges