Money and Money Supply are the lifeline of an economy and central to our daily transactions. Understanding the mechanics of money and money supply is essential for grasping the broader economic forces at play, enabling informed decisions in both personal finance and policy-making arenas. This article of NEXT IAS aims to explain in detail the concept of Money and its types, along with the mechanism involved in the supply of money, Money Supply Measures, and other related concepts.

What is Money?

Money is defined as something that is generally accepted by society as a medium of exchange and which can act as a unit of account, a store of value, and be used for repayment of debt.

Money developed as a better alternative to the barter system of trade that had existed across the world since ancient times.

Barter System and Evolution of Money

The Barter System refers to the act of trading goods and services between two or more parties directly, without the use of an intermediary monetary medium, such as money or credit card. In other words, the barter system involves an exchange of one kind of goods and services for another kind of goods and services.

The barter system has been in use since the beginning of recorded history. However, as the economy grew in terms of its size and number of economic players, this system of trade started facing several difficulties as explained below:

- Issue of Double Coincidence of Wants: “Double Coincidence of Wants” means that if one wants to exchange some goods with another person then the latter must also be willing to exchange his goods with the first person.

- For example, a person, who wants clothes and has rice with him to offer in return, can exchange rice for cloth with only that another person who has cloth and who also wants rice. In practical life, finding such a person might be difficult.

- Issue of Large and Long Storage: In a barter system, a person must store a large volume of his own goods in order to exchange for his/her desired goods with others on a day-to-day basis. However, the good loses its original quality and value if it is stored for a long period.

These problems of the Barter System meant that as human civilization progressed, people felt the need for some common medium of exchange that could be easily carried, stored, and used to express the value of a good. It is this need that brought the money into being.

Major Functions of Money

The main functions of money in a modern economy can be seen as follows:

- Medium of Exchange: The primary and unique function of money is to serve as a medium of exchange. It resolves the issue of double coincidence of wants and facilitates economic exchanges with ease.

- Unit of Account: Money is the common standard for measuring the relative worth of goods and services. This makes it easier to compare values and setting prices.

- Store of Value: Money also serves as a store of value. People can hold their wealth in the form of money. Money provides a liquid store of value because it is easy to spend and store.

- Standard of Deferred Payments: Money facilitates transactions that are not settled immediately but require a future payment.

- Means of Payment: Money is used to settle debts and pay for obligations, including taxes, fees, and fines.

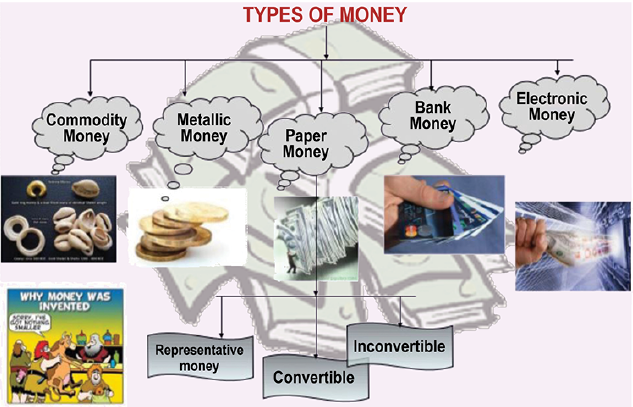

Types of Money

Economies across the world make use of various forms of money as can be seen below:

Commodity Money

Commodity money is that type of money that possesses intrinsic value of its own, independent of any governing body. This means the money itself contains a worth.

Numerous commodities such as gold, silver, copper, chocolate beans, etc, have been used as Commodity Money.

Metallic Money

Metallic Money refers to money that is made up of pure and superior metals like gold and silver. Convenience, storability, high-value density, and easy portability led metallic money to take the place of commodity money.

Paper Money

Paper money consists of currency notes issued by the government or the central bank of a country.

Fiat Money

- Fiat Money refers to Government-issued money, not backed by any physical commodity like gold and silver, but by the Government that issued it.

- This type of money does not have any intrinsic value as such. Rather, they derive their value from the guarantee provided by the issuing authority.

- Currency notes and coins in India are examples of fiat money.

- In India, every currency note and coin bears on its face, a promise from the Governor of RBI that if someone produces them to RBI or any other commercial bank, RBI will be responsible for giving the person purchasing power equal to the value printed on them.

- Fiat Money is also called legal tenders as they cannot be refused by any citizen of the country for settlement of any kind of transaction.

- Cheques drawn on savings or current accounts and Demand Deposits (DD) are not legal tenders as they can be refused by anyone as a mode of payment.

Bank Money or Credit Money

- Bank Money or Credit Money refers to money held in the form of demand deposits with commercial banks.

- Demand deposits of banks are withdrawable through cheques. However, a cheque by itself is not money, it is only a credit instrument that is used and accepted as a medium of exchange.

- Therefore, credit money is regarded as ‘near money’.

Plastic Money

Plastic money is a term that is used predominantly in reference to the hard plastic cards in place of actual bank notes. They can come in many different forms such as cash cards, credit cards, debit cards, etc.

Helicopter Money or Helicopter Drop

- Helicopter Money or Helicopter Drop refers to increasing the supply of money in an economy through measures such as more spending, tax cuts, etc.

- It is, basically, an expansionary fiscal or monetary policy that involves printing large sums of money and distributing it to the public in order to stimulate the economy.

- The term ‘Helicopter Drop’ was coined by the American economist Milton Friedman in 1969.

Digital Money or Electronic Money

- Digital Money or Electronic Money refers to any means of payment that exists in a purely electronic form.

- Unlike other forms of money, Digital Money is not physically tangible.

- At present, this form of money is increasingly becoming prevalent with the rise of online banking and digital wallets.

Money Supply

- The total stock of money in circulation among the public at a particular point in time is called money supply or supply of money.

- It is to be noted the term ‘public’ refers to households, firms, local authorities, companies, etc, and does not include the government and banks.

- Thus, public money does not include money held by

- the government

- the RBI (in the form of CRR), and

- the commercial banks (in the form of SLR).

- Thus, public money does not include money held by

- Money, forming part of the Supply of Money, can be in the following forms:

- Currency Notes and Coins (CU)

- Demand Deposits such as Saving Bank Deposits (DD) – These are those deposits that can be withdrawn on demand from banks.

- Other Deposits such as Time Deposits/Term Deposits/Fixed Deposits – These are those deposits that can be withdrawn only after a specific time.

- Money held in Post Office Saving Accounts.

- Deposits of Banks in other Banks/RBI (except CRR).

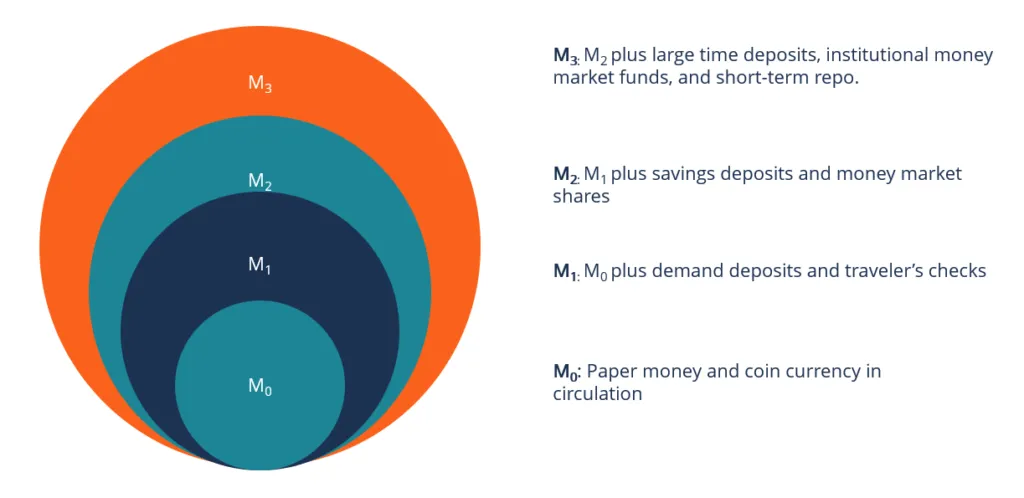

Money Supply Measures

Money Supply Measures refer to the tools used to measure the supply of money in an economy. In India, the RBI has been using the following tools as money supply measures:

- M0 (or Reserve Money)

- M1 (or Narrow Money)

- M2

- M3 (or Broad Money)

- M4

The following points are to be noted w.r.t. these Money Supply Measures:

- These measures of the supply of money vary in terms of the liquidity they possess.

- The decreasing order of liquidity of these monetary aggregates is: M0 > M1 > M2 > M3 > M4.

- This decline in liquidity indicates the shifting of its nature from a ‘medium of exchange’ to a ‘store of value’.

- In India, mostly M0, M1, and M3 are used, while M2 and M4 are rarely used.

M0 (Reserve Money)

M0 is the sum of

- Currency in Circulation

- Bankers’ Deposits with RBI, and

- ‘Other’ Deposits with RBI

Here, ‘Other’ Deposits with RBI comprise mainly:

- Deposits of quasi-government and other financial institutions including primary dealers,

- Balances in the accounts of foreign Central banks and Governments,

- Accounts of international agencies such as the International Monetary Fund, etc.

M1 (Narrow Money)

M1 is the sum of

- Currency with the Public, and

- Net Demand Deposits held by Commercial Banks

M2

M2 is the sum of

- M1, and

- Savings Deposits with Post Office Savings Banks

M3 (Broad Money)

M3 is the sum of

- M1, and

- Net Time Deposits with the Banking System

M4

M4 is the sum of

- M3, and

- Total Deposits with Post Office Savings Organizations (excluding National Savings Certificate)

New Monetary Aggregates

The Working Group on Money Supply: Analytics and Methodology of Compilation (Chairman: Dr. Y.V. Reddy), in 1998, recommended the compilation of 4 monetary aggregates on the basis of the balance sheet of the banking sector in conformity with the norms of progressive liquidity. The RBI has started publishing these new monetary aggregates as a measure of supply of money:

- NM0 (Monetary Base)

- NM1 (Narrow Money)

- NM2

- NM3 (Broad Money)

NM0 (Monetary Base or Reserve Money)

NM0 is the sum of

- Currency in Circulation

- Bankers’ Deposits with RBI, and

- ‘Other’ Deposits with RBI

Here, ‘Other’ deposits with RBI comprise mainly:

- Deposits of quasi-government and other financial institutions including primary dealers,

- Balances in the accounts of foreign Central banks and Governments,

- Accounts of international agencies such as the International Monetary Fund, etc.

NM1 (Narrow Money)

NM1 is the sum of:

- Currency with the Public

- Current Deposits with the Banking System

- Demand Liabilities Portion of Savings Deposits with the Banking System, and

- ‘Other’ Deposits with RBI

Thus, NM1 includes currency with the public and non-interest-bearing deposits with the banking sector including that of RBI.

NM2

NM2 is the sum of:

- NM1, and

- Short-term Time Deposits of Residents (including and up to the contractual maturity of 1 year)

NM3 (Broad Money)

NM3 is the sum of:

- NM2,

- Long-term Time Deposits of Residents, and

- Call/Term Funding from Financial Institutions.

Thus, NM3 captures the complete balance sheet of the banking sector.

Liquidity Aggregates

In addition to the New Monetary Aggregates, the Working Group had also recommended the compilation of three Liquidity Aggregates – L1, L2, and L3.

L1

L1 is the sum of:

- NM3, and

- All Deposits with the Post Office Savings Banks (excluding National Savings Certificates).

L2

L2 is the sum of:

- L1,

- Term Deposits with Term-Lending Institutions and Refinancing Institutions (FIs),

- Term Borrowing by FIs, and

- Certificates of deposit issued by FIs.

L3

L3 is the sum of:

- L2, and

- Public Deposits of Non-Banking Financial Companies (NBFCs)

Velocity of Money

The velocity of money is a measurement of the rate at which money is exchanged in an economy. In simple terms, it refers to:

- the number of times that money moves from one entity to another, OR

- the number of times a unit of currency is used in a given period of time, OR

- the rate at which consumers and businesses in an economy collectively spend money.

The velocity of money is usually measured as a ratio of GDP to a country’s Total Money Supply. Thus,

Velocity of Money = GDP/Total Money Supply

Significance of Velocity of Money

- Indicator of Robustness of Economy: Velocity is important for measuring the rate at which money in circulation is used for purchasing goods and services. This helps investors gauge how robust the economy is.

- Indicator of Inflation: It is also a key input in the determination of an economy’s inflation calculation. Economies that exhibit a higher velocity of money have a higher rate of inflation, and vice versa.

- Important for GDP Growth: A higher Velocity of Money is also important for ensuring higher GDP growth. This is illustrated as follows:

- Velocity of Money = GDP/Total Money Supply

Hence, GDP = Money Supply × Velocity of Money

- Velocity of Money = GDP/Total Money Supply

Thus, GDP cannot be controlled through the supply of money alone.

- If there is an increase in money supply, but the velocity of money decreases, the GDP may stay the same or even decline.

- If the supply of money is decreased, but the velocity of money increases, GDP could increase.

Therefore, an increase in the supply of money does not necessarily lead to an increase in GDP or inflation without taking the velocity of money into consideration.

The concepts of Money and Money Supply are foundational to understanding economic dynamics. As economies continue to evolve, with digital currencies and new forms of transactions emerging, the definitions and implications of Money and Money Supply will likely adapt.

FAQs on Money and Money Supply

What Constitutes Money?

Anything that can serve as a medium of exchange, a unit of account, a store of value, and be used for repayment of debt can be called Money. There are various types of money such as Commodity Money, Metallic Money, Paper Money, etc.

What is meant by ‘Currency in Circulation’?

“Currency in Circulation” refers to banknotes and coins that are not held by the Central Bank or banking institutions, but are instead in the cash reserves of banks or in the hands of the public and are actively being used in an economy for transactions.

How does the Central Bank control the Money Supply?

The Central Bank makes use of various monetary policy instruments to control the supply of money in an economy.

What role does the Supply of Money play in Inflation?

Inflation is more or less directly related to the money supply in an economy. The higher the supply of money, the higher the inflation, and vice versa.

How does the Money Supply impact interest rates?

The supply of money and interest rates have an inverse relationship. This means that generally, as the supply of money in an economy increases, interest rates tend to decrease, and vice versa.