Government budgeting is a fundamental aspect of public administration and governance, serving as a critical tool for economic management, policy implementation, and social development. It reflects the government’s priorities, commitments, and plans for the nation’s future. This article of NEXT IAS aims to explain in detail the meaning of government budgeting, key components of a government budget and other related concepts.

What is Government Budgeting?

Government budgeting is the process by which governments plan, allocate, and monitor the spending of public funds. It involves estimating government revenues (from taxes, fees, and other sources) and deciding on the expenditures necessary to achieve the government’s policy objectives within a specified fiscal period, usually a year.

Government Budgeting in India

Government budgeting in India is a comprehensive process involving the preparation, enactment, and execution of budgets by the Center and/or the states. For the purpose of this article, we will focus on the budget of the central government, called as the Union Buget of India.

Union Budget of India

As per Article 112 of the Constitution of India, the Union Budget of a fiscal year refers to the annual financial statement of the Union Government for that particular fiscal year. It contains a detailed account of the estimated receipts and expenditures of the government for a particular fiscal year that runs from 1st April to 31st March.

The data contained in the Union Budget of India can be categorized into the following three categories:

- Budget Estimates of receipts and expenditures for the upcoming fiscal year (also known as the Budget Year)

- Revised Estimates of receipts and expenditures for the current fiscal year.

- Provisional Actuals of receipts and expenditures for the previous fiscal year.

For example, the Union Budget 2023-24 was presented towards the end of the fiscal year 2022-23 in February 2023. Thus, for the Union Budget 2023-24, the 2022-23 became the current fiscal year, 2021-22 became the previous fiscal year and 2023-24 became the upcoming fiscal year. Thus, the Union Budget 2023-24 contained these three categories of data:

- Budget Estimates of receipts and expenditures for the fiscal year 2023-24

- Revised Estimates of receipts and expenditures for the fiscal year 2022-23

- Provisional Actuals of receipts and expenditures for the fiscal year 2021-22

Key Facts about the Union Budget of India

- From the budget year 2017-18 and onwards, the Union Budget is presented by the Union Finance Minister on February 1 of every year.

- Prior to the budget year 2017-18, the Budget was presented in the last week of February as per the colonial practice.

- The Railway Budget was merged with the General Budget from the fiscal year 2017-18 based on the recommendation of the Bibek Debroy Committee.

- The Railway Budget was separated from the General Budget by the British in 1924 on the recommendations of the Acworth Committee.

- The nodal agency for the preparation of the Union Budget is the Budget Division of the Department of Economic Affairs (Ministry of Finance).

Process of Government Budgeting in India

The process of government budgeting in India comprises four distinct phases:

- Budget Formulation: It involves preparation of estimates of expenditure and receipts for the ensuing financial year.

- Budget Enactment: It involves approval of the proposed Budget by the Legislature through the enactment of Finance Bill and Appropriation Bill

- Budget Execution: It involves enforcement of the provisions in the Finance Act and Appropriation Act by the government. Roughly, it comprises of collection of receipts and making disbursements for various services as approved by the legislature.

- Legislative Review: It refers to audits of government’s financial operations on behalf of the legislature

Procedure for Budget Enactment

The enactment of the Union Budget forms the most crucial part of the government budgeting process. The whole process of enactment of the Union Budget is described in chronological order as follows:

- President’s Recommendation: As per Rule 204 (1) of the Rules of Procedure and Conduct of Business in the Lok Sabha, the Budget is presented to the Parliament on such date as is fixed by the President. Thus, the recommendation of the President of India is taken for introduction and consideration of the budget in the Lok Sabha.

- Presentation of the Budget: The Union Finance Minister presents the Union Budget in the Lok Sabha with a speech known as Budget Speech.

- In the Budget Speech, the Union Finance Minister summarizes the key points of the budget and explains the thinking behind the proposals.

- At the end of the Budget Speech, the budget is laid before the Rajya Sabha as well.

- General Discussion on the Budget: A few days after the presentation, the general discussion on the budget begins in both houses of the Parliament.

- During the general discussions, the House is at liberty to discuss the budget as a whole or any question of principle involved therein, but no motion can be moved nor can the budget be submitted to the vote of the House.

- Scrutiny by Departmental Committees: After the general discussion on the budget is over, the Houses are adjourned for some perio, during which the demands for grants are scrutinized thoroughly by the Departmental Standing Committees. The committees, then, submit their reports to the Parliament.

- Voting on Demands for Grants: In the light of the reports submitted by the departmental standing committees, the Lok Sabha debates and votes on the demands for grants. Once duly voted upon and passed by the Lok Sabha, a demand becomes a grant.

- The Rajya Sabha can discuss the budget but has no power to vote on the demands for grants. This is the exclusive privilege of the LS.

- Cut Motion: During the stage of Voting on Demands for Grants, the MPs can move cut motions to reduce any demand for grant.

- Cut Motions are of 3 types:

- Policy Cut Motion: it states that “the amount of the Demand be reduced to `1”. It represents disapproval of the policy underlying the demand.

- Economy Cut Motion: It states that “the amount of the demand be reduced by a specified amount”. Thus, it represents the economy that can be affected in the proposed expenditure.

- Token Cut Motion: It states that “the amount of the demand be reduced by `100”. Its purpose is to vnetilate a specific grievance.

- Passing of Appropriation Bill: After the demands for grants are approved, the Appropriation Bill is introduced, debated, and voted upon.

- After Presidential assent, the Appropriation Bill becomes the Appropriation Act and authorizes withdrawals from the Consolidated Fund of India to meet the government’s expenditure.

- Passing of Finance Bill: The Finance Bill, containing the government’s tax proposals, is introduced immediately after the presentation of the Budget.

- The passing of the Finance Bill is mandatory to legalize the income side of the budget.

- With passing of the Finance Bills, the process of the enactment of the budget gets completed.

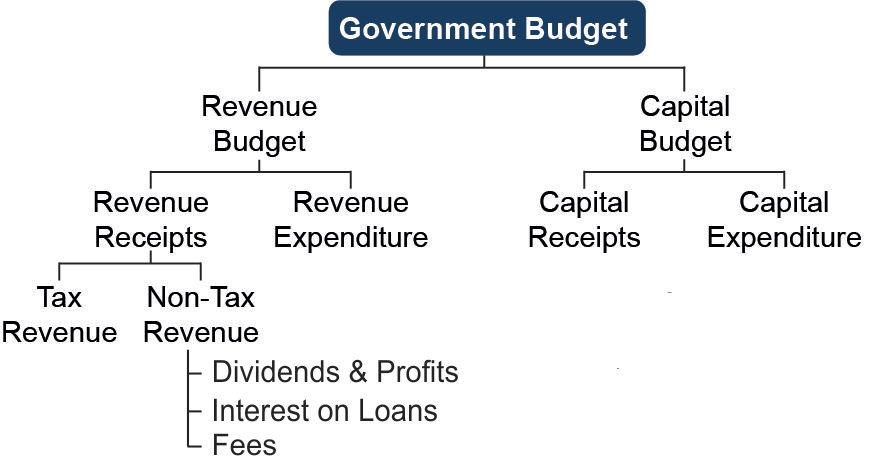

Components of Government Budget

There are, broadly, two main components of the Government Budget – Revenue Budget and Capital Budget

Revenue Budget

This component comprises the details of revenue receipts and expenditures for the upcoming fiscal year. Thus, this, in turn, has 2 sub-components:

Revenue Receipts

This includes the income the government expects to receive within the fiscal year that is not to be paid back by the government.Revenue Receipts are not reclaimed from the government, and hence they don’t impact the liabilities and assets of the government.

Revenue Receipts are of 2 types:

Tax Revenue

It consist of the proceeds of taxes and other duties levied by the Central Government.

Tax revenues comprise of proceeds coming from the following types of taxes:

- Direct Taxes – It includes taxes which are imposed directly on individuals (personal income tax) and firms (corporation tax).

- Indirect Taxes – It includes taxes like Excise Taxes (duties levied on goods produced within the country), Customs Duties (taxes imposed on goods imported into and exported out of India) and Service Tax.

- Other Direct Taxes – It includes taxes like Wealth Tax, Gift Tax etc.

Non-Tax Revenue

It comprises earnings from sources other than taxes, and mainly consists of:

- Interest receipts on account of loans by the Central Government

- Dividends and profits on investments made by the government

- Fees and other receipts for services rendered by the government.

- Revenue from Spectrum Auctions

- Loans and Grants-in-aids from foreign countries and international organisations

Revenue Expenditure

Revenue Expenditure is expenditure incurred for purposes other than the creation of physical or financial assets. Thus, these expenses do not yield any revenue in the future.

Some major components of the Revenue Expenditure include expenses incurred for the purpose of

- Day-to-day functioning of the government departments

- Salaries, pensions, subsidies, interest payments

- Offering various services to citizens.

- Interest payments on debt incurred by the government

- Grants given to State Governments and other parties (even though some of the grants may be meant for creation of assets).

Capital Budget

The Capital Budget is an account of the assets as well as liabilities of the Central Government. This shows the capital requirements (for creating long term durable infrastructure) of the government and the pattern of their financing.

The Capital Budget, in turn, has 2 sub-components:

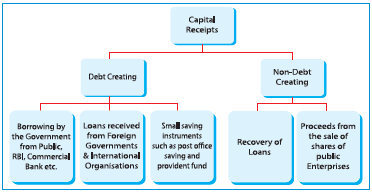

Capital Receipts

They comprise the funds received by the government that are not part of the regular income sources. All those receipts of the government which create liability or reduce financial assets are termed as capital receipts.

Capital Receipts are of two types:

Debt Creating

These include fresh loans and other liabilities raised by the government.

Non-Debt Creating

These include amounts received by the government from the disposal of its assets and recovery of loans.

Capital Expenditure

It comprises expenses incurred by the government to create long-term assets and investments that give profits or dividends in the future.

Some of the major components of Capital Expenditure include:

- Expenditure on developing infrastructure like roads, schools, hospitals, etc.

- Investments in shares of the government companies and corporations.

- Loans and advances made by the Central government to States and Union Territories or foreign agencies.

- Repayments of loans and other liabilities (only repayment of the principle amount of the loan forms capital expenditure. Interest payments on loans is a part of the revenue expenditure.)

Types of Budget

The government budget (central budget or state budget) can be of three types – Balanced Budget, Surplus Budget, and Deficit Budget.

Balanced Budget

A balanced budget is the one wherein the expected or actual receipts are equal to proposed expenditures. This means that the income equals the total spending.

A Balanced Budget increases the level of aggregate demand in the economy moderately. Hence, it is recommended in a situation when the economy is close to achieving full employment.

Surplus Budget

A surplus budget is the one wherein receipts exceed expenditures. In other words, more money is coming in than going out.

A Surplus Budget reduces the aggregate demand. Hence, it is recommended in an economic situation when there is a large inflationary gap

Deficit Budget

A deficit budget is the one wherein expenditures exceed receipts. This means the government is spending more money than it is earning or receiving.

A Deficit Budget increases the aggregate demand. Hence, it is recommended in an economic situation of depression.

Deficit and its Types

In the context of Government Budget, the gap between the receipts and expenditure is called Deficit.

There are various types of Deficit in the context of government budgeting:

Budget Deficit

Budget Deficit refers to the difference between all receipts and expenses in both revenue and capital account of the government.

Budget Deficit = Total Expenditure – Total Receipts

Since it, usually, equals to zero (0), it does not have much significance.

Revenue Deficit

Revenue Deficit is the excess of government’s revenue expenditure over its revenue receipts.

Revenue Deficit = Revenue Expenditure – Revenue Receipts

A high revenue deficit, usually, results in borrowing by the government to finance recurring and non-asset creating expenditure. Since it may lead to unsustainable levels of debt, it is a warning to the government either to curtail its expenditure or increase its tax and non-tax receipts.

Effective Revenue Deficit (ERD)

Effective Revenue Deficit is the difference between revenue deficit and grants for creation of capital assets. Thus, it indicates the actual revenue deficit after grants given for capital expenditure.

Effective Revenue Deficit = Revenue Deficit – Grants for Creation of Capital Assets

Effective Revenue deficit was introduced in the Union Budget 2012-13, on the suggestion of Rangarajan Committee

Fiscal Deficit

Fiscal Deficit is defined as excess of total budget expenditure (revenue and capital) over total budget receipts (revenue and capital) excluding borrowings during a fiscal year.

Fiscal Deficit = Total Expenditure – (Revenue Receipts + Non-Debt Creating Capital Receipts)

Fiscal deficit is a measure of how much the government needs to borrow from the market to meet its expenditure when its resources are inadequate.

Primary Deficit

Primary Deficit is defined as fiscal deficit of current year minus interest payments on accumulated debt.

Primary Deficit = Fiscal Deficit – Net Interest Liabilities

It is a measure of current year’s fiscal operation after excluding the liability of interest payment created due to borrowings undertaken in the past.

Monetized Deficit

Monetized Deficit refers to that part of the fiscal deficit which is financed by the government either by borrowing money or drawing-down its cash from the RBI.

Monetized Deficit = Borrowing from RBI + Draw-down by the government of its cash balance from the RBI.

It involves infusion of new money and hence expansion in money supply in the economy.

Types of Government Budgeting

Based on the underlying philosophy and the process followed, there are various types of government budgeting:

Line-Item Budgeting

- In a line-item system, expenditures for the budgeted period are listed according to objects of expenditure, called “line items”.

- It major ddvantage is that it facilitates centralized control and fixing of authority and responsibility of the spending units. However, it does not provide enough information to the top levels about the activities and achievements of individual units.

Performance Budgeting

- It uses performance information for the allocation of funds and management of a program and is aimed to increase the efficiency and effectiveness of public expenditures.

- It involves the precise definition of the work to be done or services to be rendered and a correct estimate of what that work or service would cost. Thus, under this type of budgeting, the emphasis gets shifted from the means of accomplishment to the accomplishments themselves.

Zero-Based Budgeting (ZBB)

- It is based on the concept that all programs of the Department were to be reviewed afresh from the base zero and not merely in terms of incremental changes proposed for the budget year. The basic tenet of Zero-Based Budgeting (ZBB) is that program activities and services must be justified annually during the budget development process.

- The Ministry of Finance formally introduced Zero-Base Budgeting in 1986 asking all the Ministries and Departments of the Government to adopt Zero-Base Budgeting approach with effect from the budget for 1987-88. However, it has not yet been fully implemented in India.

Outcome Budgeting

- Under Outcome Budgeting symbolizes a shift from traditional budgeting in the sense that it goes beyond budgeting by inputs (how much can we spend) towards budgeting by measurable outcomes (what can we achieve with what we spend). The first step in developing an outcome budgeting system involves the process of defining the desired outcomes. This is followed by the process of identifying the interventions required for achieving target outcomes. Finally, the expenditure required for implementing the identified interventions is estimated.

- The first outcome budget in India was passed by the Parliament on August 25, 2005. However, a consolidated Outcome budget covering all Ministries and Departments was laid down for the first time in Budget 2017-18.

Gender Budgeting

- Gender Budgeting is a method of planning, programming and budgeting that helps advance gender equality and women’s rights. It dissection of the Government budgets to establish its gender differential impacts and to ensure that benefits of development reach women as much as men.

- A Gender Budget Statement (GBS) was first introduced in the Indian Budget in 2005-06.

Related Concepts

Crowding Out Effect

The crowding out effect is an economic theory suggesting that increased government spending leads to a reduction in private sector spending. The government increases taxation or borrowing in order to fund the increased spending. This leads to lesser money supply in the market as well as an increase in interest rates. This leads to reduction in private investment spending, which dampens the initial impact of the increase of total investment spending.

Fiscal Consolidation

Fiscal consolidation is a process where government’s fiscal health is improved by reducing fiscal deficit to levels which is manageable and bearable for the economy. Improved tax revenue realization and better aligned expenditure are important components of fiscal consolidation.

Off Budget Financing

- The Off-Budget Financing refers to the expenditure undertaken by the PSUs through the market borrowings based upon guarantee of repayment of loans given by Government.

- For example, if the government needs to invest in the Railways, it may ask the Indian Railway Finance Corporation (IRFC) to borrow money from the market and finance railway projects. However, the Government guarantees the repayment of principal and interest for the money borrowed by Indian Railway Finance Corporation in case it fails to repay the borrowed money.

Monetization of Deficit

- Monetization of deficit refers to the practice where a government finances its budget deficit by creating new money. This is typically done through the central bank, which buys government bonds or securities directly using new money that it has created, effectively increasing the money supply. The government then uses this money to cover its expenditures that exceed its revenue, such as public services, social programs, or infrastructure projects.

- Prior to April 1, 1997, the fiscal deficit of the government was mainly financed through monetization of the government deficits. However, this practice has been now discontinued and replaced by the Ways and Means Advance (WMA) system.

Ways and Means Advances (WMA)

- WMAs are short-term loan facility or an overdraft facility provided by the central bank to the government to bridge the gap between its payments and receipts. This tool allows the government to meet its immediate expenditure requirements without having to resort to last-minute or expensive borrowing from the market.

- The WMA facility is available for 90 days and its interest rate is linked to the Repo Rate.

- The WMA system replaced the practice of monetization of government deficit which had been in practice prior to April 1, 1997.

Fiscal Drag

Fiscal drag is an economic term whereby an increase in income or inflation or income moves taxpayers into higher tax brackets. The increase in taxes reduces aggregate demand and consumer spending from taxpayers as a larger share of their income now goes to taxes, which leads to deflationary policies, or drag, on the economy. Thus, it acts as an automatic fiscal stabilizer by controlling a rapidly expanding economy from overheating.

Fiscal Neutrality

- Fiscal neutrality is when a government taxing, spending, or borrowing decision has or is intended to have no net effect on the economy. Any new spending introduced by a policy change that is fiscally neutral is expected to be entirely offset by additional revenues generated; the net effect of the policy change is neutral with respect to the balance of the government’s budget. Thus, fiscal neutrality creates a condition where demand is neither stimulated nor diminished by taxation and government spending.

- A balanced budget is an example of fiscal neutrality, where government spending is covered almost exactly by tax revenue.

Pump Priming

Pump priming is the action taken to stimulate an economy usually during a recessionary period, through government spending, and interest rate and tax reductions. It, usually, involves measures to prompte higher demand for goods and services. The increase in demand experienced through pump priming can lead to increased profitability within the private sector, which assists with overall economic recovery.

Economic Stimulus

An economic stimulus is the use of monetary or fiscal policy changes to kick start growth during an economic recession. It involves measures such as lowering interest rates, increasing government spending and quantitative easing etc.

For example, during the COVID-19 Pandemic, the Government announced 3 tranches of economic stimulus under the Atma Nirbhar Bharat Programme.