Grasping the Fundamentals of Economics is essential, not only for developing a strong hold over the syllabus of economics, but also for a comprehensive understanding of how economic policies impact governance, society, and the world at large. This article of NEXT IAS aims to explain the fundamental concepts in economics, including the definition of economics, factors of production, types of goods, and more.

What is Economics?

Economics is a social science analyzing the production, distribution, and consumption of goods and services. In other words, it is a discipline that deals with what choices people make, and how and why they make them while making purchases.

Central Problems of the Economy

The amount of resources in an economy is limited. But, we as humans have unlimited wants. This gives rise to the problem of scarcity, requiring us to make choices or trade-offs between goods and services. This is where the role of Economics comes in.

Economics deals with the problem of scarcity by studying how societies can allocate scarce resources to produce valuable commodities and distribute them among different people. This, then, means that the central problems of an economy revolve around the following three issues:

- What to produce?

- How to produce?

- For whom to produce?

Factors of Production

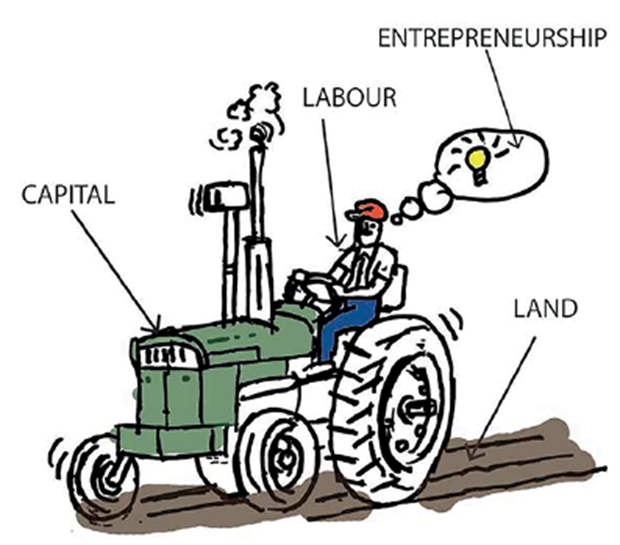

Factors of Production refer to the inputs that are used in the production of goods or services in an attempt to make an economic profit. The factors of production include – Land, Labor, Capital, and Entrepreneurship.

- Land: Land is an economic resource encompassing natural resources found within a nation’s economy. This resource includes timber, land, fisheries, farms, and other similar natural resources.

- Labor: Labor represents the human capital available to transform raw materials or natural resources into consumer goods. This roughly translates to able-bodied individuals capable of working in the nation’s economy and willing to provide various services to other individuals or businesses.

- Capital: Capital represents the investment in durable physical assets made by individuals and companies that are used to produce goods or services. These assets include buildings, production facilities, equipment, vehicles, etc.

- Entrepreneurship: Entrepreneurship is the process of designing, launching, and running a new business, which offers a product or service for sale or hire. An entrepreneur is a person who combines the other factors of production – land, labor, and capital – to start a business or an enterprise.

Types of Goods

Any good or service purchased by the consumer (Individual or Enterprise) can be for final use or use in further production. Based on their use in production and consumption processes, goods and services can be categorized into the following categories:

- Final Goods: An item that is meant for final use and will not pass through any more stages of production or transformations is called a final good.

- For Example, tea leaves are purchased by a household consumer to make tea for consumption at home.

- Intermediate Goods: Of the total production taking place in the economy, a large number of products do not end up in final consumption and are not capital goods either. Such goods may be used by other producers as material inputs, and are called Intermediate Goods.

- For Example, tea leaves purchased by a restaurant to make tea for selling to its consumers.

Branches of Economics

The study of fundamentals of economics can be subcategorized into two branches – Microeconomics and Macroeconomics.

Microeconomics

- Microeconomics is the study of the economics of the individual or business decision regarding the allocation of resources given the scarcity and government intervention.

- It includes concepts such as the relationship between supply and demand, the price of goods and services, etc.

Macroeconomics

- Macroeconomics is the study of the performance and structure of the whole economy rather than specific individual markets.

- It includes concepts such as national consumption and production, general price levels, inflation, international trade, unemployment, etc.

Schools of Economic Thought

Over a period of time, various Schools of Economic Thought have emerged to explain how economies work and to offer policy recommendations. The two most common Schools of Economic Thought are Classical and Keynesian.

- Classical View: It believes that free markets are the best way to allocate resources and the government’s role should be limited to that of a fair and strict referee.

- Keynesian View: It believes that markets do not work well at allocating resources on their own and that governments must step in from time to time and actively reallocate resources efficiently.

Thus, the Classical School of Economic Thought and the Keynesian School of Economic Thought are in contrast to each other.

Types of Economy

Based on how the central problems of an economy are addressed and the role of the state therein, the fundamentals of economic systems are classified into 3 categories:

Capitalist Economy

- The capitalistic form of economy is based on the concept of ‘laissez faire’ state i.e. non-interference by the government, which was given by Adam Smith.

- In such an economy, the decisions of what to produce, how much to produce, and at what price to sell are taken by private enterprises in the market, with the state having no economic role.

- One of the most prominent features of a capitalist economy is that the market determines prices through the laws of supply and demand. For example, when demand for coffee increases, a profit-seeking business will boost prices in order to increase its profit. If, at the same time, society’s appetite for tea diminishes, growers will face lower prices and aggregate production will decline.

Socialist Economy

- Under a true socialist system, it is the government’s role to determine output and pricing levels.

- As opposed to a Capitalist Economy, distribution in a Socialist Economy is supposed to be based on what people need and not on what they can afford to purchase. Unlike capitalism, for example, a socialist nation provides free healthcare to the citizens who need it.

Mixed Economy

- It is an economic system that features characteristics of both capitalism and socialism. A mixed economic system allows a level of private economic freedom in the use of capital but also allows for governments to interfere in economic activities in order to achieve social aims whenever required.

- For example, in a Mixed Economy, the Government seeks to redistribute wealth by taxing the private sector and using funds from taxes to promote social objectives.

Type of Economy Adopted by India

Post independence, most of the prominent leaders were in favor of adopting a Socialist Economy as it would help promote the welfare of all rather than a few. However, it was not possible in a democracy like India for the government to abolish private ownership of land and other properties of its citizens. Moreover, doing so would have created upheaval among the industrial classes and stunted India’s growth story.

So, after Independence, India opted for the Mixed Economy. Under it, some basic and important infrastructural economic responsibilities were taken up by the Government, and the rest of the economic activities were left to private enterprise i.e. the market.

The Economic Reforms carried out in the early 1990s redefined the prevailing state-market mix of the Indian Economy to usher in a new form of mixed economy. The redefined mixed economy for India has a tilt towards the market economy, with many economic roles, which were earlier under complete government monopolies, now opened for participation by the private sector.

Structural Composition of an Economy

The structural composition of an economy refers to different sectors that make contributions to the GDP of that economy. Usually, various sectors of an economy are categorized into the following categories:

Primary Sector

- The primary sector involves the extraction of raw materials from natural resources. Therefore, this is also known as the Extraction Sector.

- It includes activities such as:

- Agriculture (farming, fishing, and forestry)

- Mining

- Oil and gas extraction

- This sector provides basic foods for humans and raw materials for industries.

- People engaged in primary activity are called Red-Collar Workers due to the outdoor nature of their work.

Secondary Sector

- The secondary sector involves the transformation of raw materials into finished or manufactured goods. Thus, this sector is rightly called the Manufacturing Sector.

- Key activities included in this sector are:

- Manufacturing (automobiles, electronics, textiles, etc.)

- Construction

- Utilities (electricity, water, and gas)

- People engaged in secondary activity are called Blue-Collar Workers.

Tertiary Sector

- The sector is concerned with the intangible aspect of offering services to consumers and businesses. Thus, this sector is also called the Service Sector.

- It includes a wide range of activities such as:

- Retail and wholesale sales

- Transportation and logistics

- Information technology services etc

- People engaged in tertiary activities are called White-Collar Workers.

Quaternary Sector

- The quaternary sector is said to be the intellectual aspect of the economy. It is also called the knowledge sector.

- It includes activities such as education, training, the development of technology, and research & development.

Quinary Sector

- The Quinary Sector includes the highest levels of decision-making in an economy.

- This sector includes top executives or officials in such fields as government, science, universities, nonprofits, healthcare, culture, and the media.

- People engaged in quinary activities are called Gold-Collar Workers.

Understanding the Fundamentals of Economics, as explained above, is essential for developing a deeper understanding of the economy as a subject. Along with this, it can also provide valuable insights into the complexities of economic systems working in India and the world.

Frequently Asked Questions (FAQs)

What are the Fundamentals of Economics?

The Fundamentals of Economics encompass the foundational concepts and principles that underlie the study of how societies allocate scarce resources to satisfy unlimited wants and needs such as supply and demand, opportunity cost, etc.

What are the Factors of Production?

The Factors of Production are the resources used in the production process to create goods and services. They are classified into four main categories:

1. Land,

2. Labour,

3. Capital and

4. Entrepreneurship

What are the central problems of an economy?

The central problems of an economy arise due to the fundamental economic condition of scarcity, where resources are limited relative to the desires of individuals and society as a whole. The central problems of an economy can be

1. What to produce?

2. How to produce?

3. For whom to produce?