Syllabus: GS3/ Economy

Context

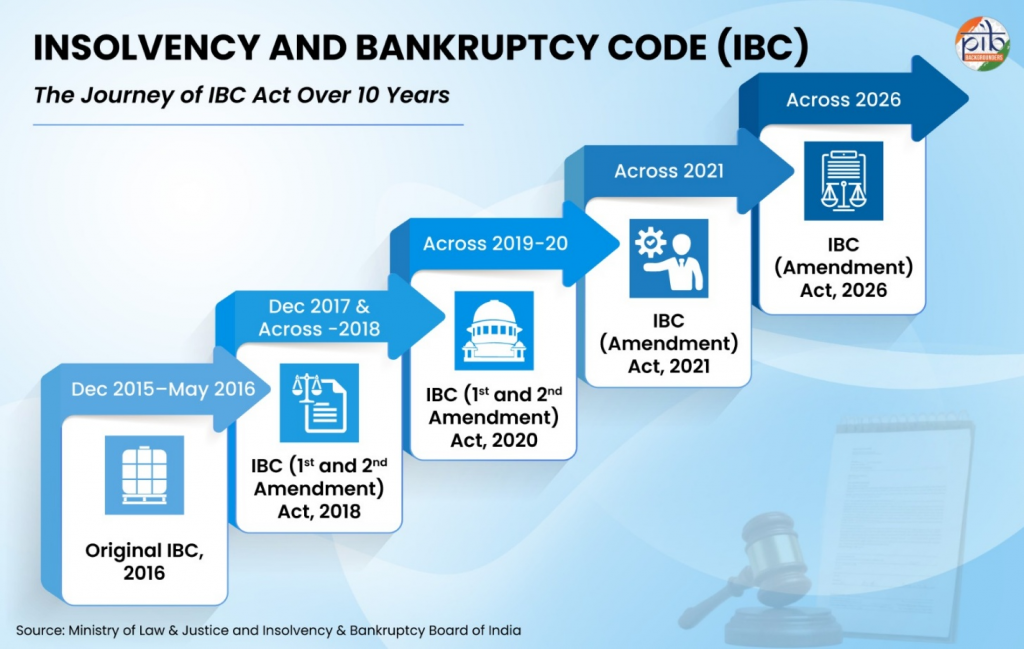

- The Insolvency and Bankruptcy Code (IBC), introduced in 2016 to create a time-bound insolvency resolution mechanism, has completed a decade.

Insolvency and Bankruptcy Code (IBC) 2016

- IBC was introduced in 2016 to address rising Non Performing Assets and ineffective debt recovery mechanisms in India.

- Objectives of the IBC resolution are;

- Business Revival: To save businesses through restructuring, changes in ownership, or mergers,

- Maximization of Asset Value: To preserve and maximize the value of the debtor’s assets,

- Promoting Entrepreneurship and Credit: To encourage entrepreneurship, improve credit availability, and balance the interests of stakeholders, including creditors and debtors.

- Currently a maximum 330 days is allowed to find a resolution for a company admitted into the insolvency resolution process.

- Otherwise, the company goes into liquidation.

Institutional Framework under IBC

- Insolvency and Bankruptcy Board of India (IBBI): The apex regulatory body established to oversee the functioning of insolvency professionals, insolvency professional agencies, and information utilities.

- National Company Law Tribunal (NCLT): The adjudicating authority responsible for admitting insolvency petitions, declaring moratoria, and approving resolution plans for companies and LLPs.

- Insolvency Professionals (IPs): IPs administer the affairs of distressed entities, safeguard assets and facilitate meetings of creditors. They oversee the resolution process in compliance with the Code and applicable regulations.

- Committee of Creditors (CoC): The supreme decision-making body comprising the distressed entity’s financial creditors. They evaluate, vote on, and approve the resolution plan.

Need for Insolvency Reforms in India

- Rising NPA Crisis: India’s banking sector suffered from massive Non-Performing Assets (NPAs), especially after the infrastructure and corporate lending boom of the 2000s.

- Ineffective Earlier Mechanisms: Earlier recovery mechanisms such as the SARFAESI Act, Debt Recovery Tribunals (DRTs) and Lok Adalats were slow and inefficient.

- Recovery proceedings continued for several years without effective resolution.

- Weak Credit Discipline: Defaulting promoters used to retain control over companies despite persistent loan defaults. The absence of strict consequences encouraged wilful defaults and poor repayment culture.

- Improving Ease of Doing Business: India’s insolvency resolution system ranked poorly in global ease of doing business indicators before the IBC.

- A predictable exit mechanism was necessary to attract domestic and foreign investment.

Success of the Insolvency and Bankruptcy Code

- Debt recovery framework: Till March 2026, a total of 8,987 Corporate Insolvency Resolution Processes (CIRPs) had been admitted under the IBC framework.

- Out of these cases, 1,419 corporate debtors were successfully resolved through approved resolution plans.

- Several additional cases were closed through settlements, appeals, reviews and withdrawals under Section 12A of the Code, reflecting the behavioural impact of the IBC on borrowers.

- Improved recovery outcomes: As of March 2026, creditors realised nearly ₹4.32 lakh crore through approved resolution plans under the IBC.

- Recoveries also amounted to more than 94.56% of the fair value of stressed assets, indicating better value maximisation under the resolution process.

- Strengthened financial discipline: The fear of losing management control has improved repayment discipline among corporate borrowers.

- Many firms have opted for early settlements before formal insolvency admission, thereby reducing prolonged litigation.

- The Reserve Bank of India’s “Report on Trends and Progress of Banking in India 2024-25”, highlighted that IBC accounted for nearly 52.4% of the total recoveries made by banks.

- Recoveries through the IBC were significantly higher than recoveries made through SARFAESI, Debt Recovery Tribunals (DRTs) and Lok Adalats.

What are the Concerns?

- Rising Delays in Resolution: The average resolution timeline increased to nearly 744 days by FY2026 against the statutory limit of 330 days.

- Nearly 78% of insolvency cases exceeded the prescribed timeline.

- Delays lead to erosion of asset value and reduce investor interest in stressed assets.

- High Haircuts for Creditors: On average, creditors face haircuts of around 67%, recovering only about one-third of their admitted claims.

- The IBC lacks clear provisions for handling issues unique to modern firms, such as intellectual property valuation, employee claims, and technology continuity.

- This limits effective resolution of non-traditional enterprises.

- Capacity Constraints: The NCLT and NCLAT continue to suffer from manpower shortages and limited infrastructure.

- Cross-Border Insolvency Challenges: Insolvency cases involving multinational assets and creditors face legal and procedural uncertainty.

Way Ahead

- Strengthen NCLTs: The government must increase the number of NCLT benches, judges and technical members to reduce pendency and delays.

- Reduce Delays: Strict timelines for appeals and insolvency proceedings must be enforced to preserve asset value.

- Prioritise Resolution: The insolvency framework must focus more on revival and restructuring of viable firms rather than liquidation.

- Limit Haircuts: Greater transparency and better valuation mechanisms are needed to reduce excessive creditor haircuts.

- Protect MSMEs: Operational creditors and MSMEs should receive fairer treatment under resolution plans.

Source: BS