Syllabus:GS3/Economy

In News

- The RBI released draft amendment directions to revise the methodology for identifying Non-Banking Financial Companies aiming to enhance transparency, simplicity, and regulatory parity.

About

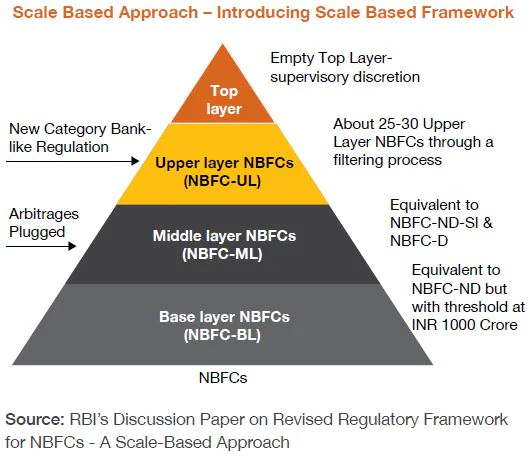

- The current Scale Based Regulatory (SBR) Framework for NBFCs prescribes a two-pronged methodology for identification of NBFC-UL viz.,

- Top ten eligible NBFCs by asset size and parametric scoring methodology.

- This dual approach has been criticised for being complex and less transparent.

- NBFC-UL are the entities posing significant systemic risks due to their size, complexity, and interconnectedness.

- Top 10 NBFCs by asset size + parametric scoring methodology like Bajaj Finance, Shriram Finance, Tata Capital, Aditya Birla Finance, LIC Housing Finance.

Proposed Amendments by RBI

- Asset Size Threshold: Single objective criterion, NBFCs with asset size ≥ ₹1,00,000 crore qualify as NBFC-UL, replacing the dual methodology. Reviewed every 5 years. Enhances predictability and ease of compliance.

- Inclusion of Government NBFCs: Currently placed in Base Layer (BL) or Middle Layer (ML), state-owned entities like NABARD, Exim Bank, and SIDBI will now be classified under Upper Layer based on size.

- State Government Guarantees: NBFC-UL entities may use state government guarantees as a credit risk transfer instrument without any cap (subject to conditions), providing greater flexibility in risk management.

Non-Banking Financial Company (NBFC)

- Definition of NBFC: A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act (1956 or 2013) that primarily conducts financial activities like loans, advances, leasing, hire-purchase, and investment in securities.

- NBFCs are prohibited by the Reserve Bank from associating with any unincorporated bodies

- Excluded activities: It does not include companies whose main business is agriculture, industry, trading goods (other than securities), services, or real estate activities.

- Residuary NBFCs: Companies that mainly collect money through deposits or instalment schemes also fall under NBFCs (called residuary non-banking companies).

- Eligibility : To register with the Reserve Bank of India (RBI) as a Non-Banking Financial Company (NBFC), a company must be incorporated under the Companies Act, 1956 or 2013 and have a minimum Net Owned Fund (NOF) of ₹10 crore.

- However, higher capital requirements apply for specialised NBFCs, such as ₹300 crore for NBFC-IFCs and IDF-NBFCs, ₹100 crore for Mortgage Guarantee Companies, ₹20 crore for Housing Finance Companies, ₹150–250 crore for Standalone Primary Dealers depending on activities, and ₹2 crore for NBFC-AA and NBFC-P2P categories.

How NBFCs are Different from Banks?

- NBFCs cannot accept demand deposits.

- They cannot issue cheques or operate payment systems.

- Their deposits are not insured by DICGC.

Key Challenges

- Regulatory Burden: More entities under UL means higher compliance costs and stricter capital/governance norms.

- Threshold Rigidity: Sole reliance on asset size may ignore risk heterogeneity and qualitative factors like interconnectedness.

- Government NBFC Impact: Inclusion may limit operational flexibility of public sector entities.

- Corporate Governance Conflicts: Cases like Tata Sons highlight how regulatory changes can trigger ownership disputes and restructuring pressures.

Way Forward

- Combine asset size with risk-based indicators to avoid oversimplification.

- Phased implementation for newly included entities, especially government NBFCs.

- Strengthen RBI’s supervisory capacity for a larger NBFC-UL pool.

- Issue clear listing guidelines to prevent regulatory arbitrage.

Source :TH

Previous article

India’s Payment Revolution