Syllabus :GS3/Economy

In News

- Indian companies are increasingly channeling their outward foreign direct investment (FDI) through low-tax jurisdictions—commonly referred to as tax havens—to expand their global footprint.

Present Scenario

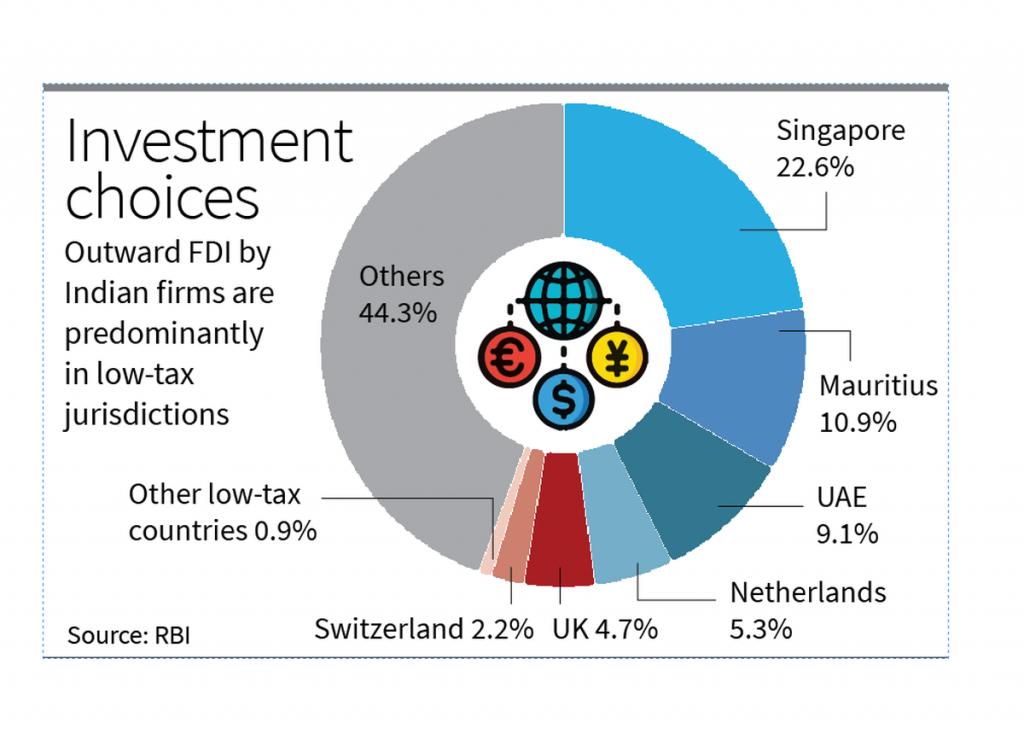

- The companies are routing their foreign investments through low-tax jurisdictions (tax havens) such as Singapore, Mauritius, UAE, the Netherlands, UK, and Switzerland.

- According to data ,56% of India’s outward FDI in 2023-24 (₹1,946 crore of ₹3,488.5 crore) went to these jurisdictions.

- In Q1 of 2024-25, this increased to 63%.

Reasons behind the Tax Haven Preference

- Indian companies prefer tax havens due to favorable legal frameworks, bilateral treaties (like the India-Mauritius DTAA) and low corporate tax rates.

- FDI regulations and taxation in India are often restrictive.

- Experts also warn that high U.S. tariffs on Indian imports might encourage companies to set up subsidiaries abroad to avoid these tariffs in the future.

- Strategic locations such as Singapore and the UAE also serve as gateways to broader markets.

- Flexible financial regulations in tax havens allow smoother capital movement and investment structuring.

- Special Purpose Vehicles (SPVs) in tax havens help attract international investors and facilitate stake dilution.

Impacts on India’s Economy

- Routing profits through tax havens can reduce India’s taxable income base.

- Tax havens are often associated with money laundering and base erosion.

- Increases the risk of round-tripping, where Indian money is sent abroad and reinvested in India under the guise of FDI.

- Overreliance on foreign structuring may reduce direct investment in Indian operations, impacting job creation and local growth.

- Difficult for Indian authorities to track ultimate investment destinations and enforce compliance.

Steps Taken

- India has initiated several reforms to address the challenges posed by tax haven-linked FDI and these includes:

- Renegotiation of treaties with Mauritius and Singapore to include anti-abuse clauses.

- India is part of the OECD’s Base Erosion and Profit Shifting (BEPS) initiative to curb profit shifting.

- The government has streamlined FDI norms, enhanced sectoral caps, and introduced Jan Vishwas reforms to improve ease of doing business.

Conclusion and The Way Ahead

- Indian companies use tax havens not only for tax benefits but also for strategic and operational reasons.

- While this supports global expansion, it challenges India’s tax system, regulations, and domestic investments.

- To balance this, India should improve ease of doing business, simplify regulations, and strengthen international tax cooperation to ensure outward FDI benefits the economy.

- Additionally, international cooperation is key to enforcing tax standards and curbing illicit flows.

- A balanced, reform-driven approach is essential to support global ambitions without compromising fiscal integrity.

Source :TH

Previous article

The SC issued Guidelines for Cases where DNA Evidence is Involved

Next article

News In Short – 15 September, 2025