Syllabus: GS3/ Economy

Context

- India’s financial inclusion journey is undergoing a paradigm shift, driven by the convergence of a strong Digital Public Infrastructure (DPI) and Artificial Intelligence (AI).

What is financial inclusion?

- As per the World Bank, financial inclusion means that individuals and businesses have access to useful and affordable financial products and services that meet their needs — transactions, payments, savings, credit and insurance — delivered in a responsible and sustainable way.

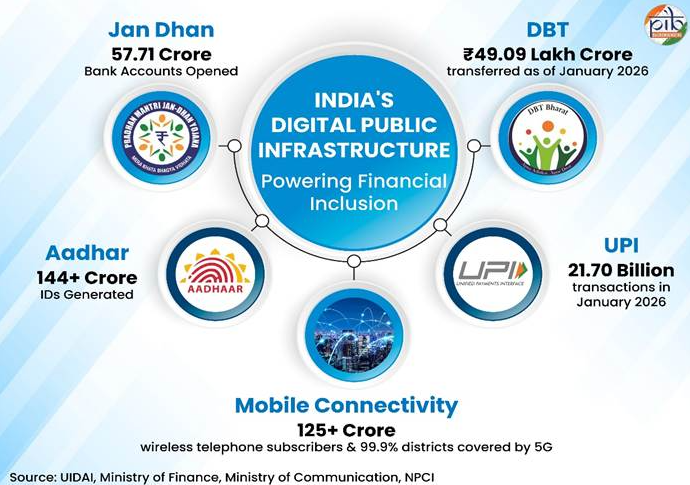

India’s Digital Foundation for Financial Inclusion

- In 2021, the Reserve Bank of India (RBI) launched a Financial Inclusion Index (FI-Index) to track the process of ensuring access to financial services, timely and adequate credit for vulnerable groups such as weaker sections and low-income groups at an affordable cost.

- JAM Trinity (Jan Dhan-Aadhaar-Mobile): JAM is a foundational convergence of universal bank accounts, biometric identity, and mobile connectivity.

- Direct Benefit Transfer (DBT): Under the DBT system, government subsidies and welfare benefits are directly transferred into the bank accounts of beneficiaries, to enhance transparency by removing intermediaries.

- Unified Payments Interface (UPI): UPI is a real-time payment system that allows for instant money transfers between any two bank accounts via a mobile platform.

- Atal Pension Yojana (APY): It was launched in 2015 and provides social security to unorganised sector workers.

- APY is regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It functions under the National Pension System (NPS) framework.

Integration of AI in financial services

- MuleHunter.AI: Launched in 2024 by the Reserve Bank Innovation Hub (RBIH), MuleHunter.AI is an advanced AI-powered tool designed to identify and mitigate “mule” bank accounts used in cybercrimes.

- Digital India BHASHINI Division and Reserve Bank of India signed a Memorandum of Understanding in 2026 to integrate AI-based language technologies into banking and financial services.

- Digital ShramSetu: It is a proposed initiative designed to empower India’s 490 million informal workers by leveraging Artificial Intelligence (AI), blockchain, and immersive learning.

- It aims to bridge digital divides, enhance productivity, and provide social protection to workers in the informal economy through a dedicated national ecosystem.

- AI-Based Credit Scoring: For individuals without a CIBIL score, AI-based lending systems use digital transaction patterns and behavioural data to evaluate financial reliability.

- Unified Lending Interface (ULI): Reserve Bank of India developed the ULI as a Digital Public Infrastructure (DPI) for frictionless and inclusive credit delivery.

Key Terms

- Digital Public Infrastructure (DPI) refers to interoperable digital systems- such as digital identity, payment platforms, and data exchange frameworks that enable secure and efficient service delivery.

- Application Programming Interface (API) is a set of rules and protocols that allows different software applications to communicate and exchange data with each other.

- CIBIL Score, issued by Credit Information Bureau (India) Limited (CIBIL), is a three-digit numeric summary of a user’s credit profile and loan-worthiness, based on past repayment behaviour and credit records.

Challenges to Financial Inclusion

- Digital Divide: Many rural populations lack access to smartphones or the internet, restricting access to digital financial services.

- Low Financial Literacy: Lack of awareness about formal financial products and schemes hampers their adoption.

- Overall national financial literacy stands at only 62.6%. (According to 2023 data).

- Trust Deficit: Fear of fraud, complex procedures, and prior bad experiences discourage first-time users from participating in formal finance.

- Cybercrime reports increased 24.4% between 2021–22 (NCRB data), indicating rising digital fraud.

- Infrastructure Deficit: Inadequate banking infrastructure (ATMs, branches) in remote areas reduces outreach.

- Gender Disparity: Although bank account ownership among women has improved, actual usage remains low due to social and cultural constraints.

Way Ahead

- Strengthening Digital Literacy: Expand awareness and digital training programmes for rural and vulnerable populations.

- Ensuring Data Protection: Implement robust safeguards for consent-based and secure data sharing.

- Inclusive AI Models: Develop transparent and unbiased AI algorithms for equitable financial access.

- Expanding DPI Infrastructure: Improve digital connectivity and last-mile financial infrastructure.

- Strengthening Regulatory Oversight: Enhance cybersecurity frameworks and AI governance standards.

Source: PIB

Previous article

NEET Paper Leak Controversy