Syllabus: GS3/Economy; Financial Inclusion

Context

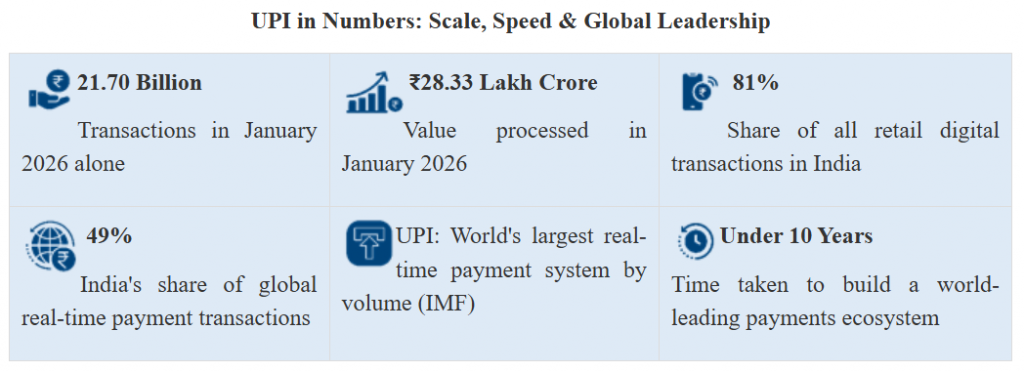

- Recently, India’s Unified Payments Interface (UPI) has completed 10 years of its operations as it has revolutionized financial inclusion and real-time payments. However, the rapid expansion has been accompanied by rising fraud risks, necessitating regulatory intervention.

About India’s Digital Payment Ecosystem

- Evolution and Growth of Digital Payments in India: India has become one of the largest digital payments markets globally. UPI dominates with billions of monthly transactions and widespread adoption.

- Growth driven by Digital India Programme, JAM Trinity (Jan Dhan–Aadhaar–Mobile); and expansion of smartphones and affordable internet.

- India’s digital payment ecosystem is built on interoperability, innovation, and inclusion, making it a global model.

- India accounts for a significant share of global real-time payments. Rapid increase in transaction volume, merchant adoption, and digital penetration in Tier-2 and Tier-3 cities.

Key Components of the Ecosystem

- Unified Payments Interface (UPI): It is developed by National Payments Corporation of India (NPCI) that enables instant, interoperable bank transfers.

- It supports peer-to-peer (P2P) and merchant (P2M) transactions, and has become the dominant retail payment system globally.

- UPI’s scalability and low-cost architecture have made it a model for other countries.

- Supporting Payment Systems: Immediate Payment Service (IMPS), National Electronic Funds Transfer (NEFT), Real-Time Gross Settlement (RTGS); Aadhaar Enabled Payment System (AePS); and Bharat Bill Payment System (BBPS) etc.

- This multi-layered structure ensures flexibility and resilience.

Impacts of India’s Digital Payment Ecosystem

- Financial Inclusion and Accessibility: Expansion of bank accounts under PMJDY; integration with Aadhaar and mobile connectivity and enabling access to digital payments even in rural areas.

- It facilitates Direct Benefit Transfers (DBT) directly into bank accounts.

- India’s ecosystem is unique in combining inclusion, technology and scale.

- Convenience and Efficiency: Instant, 24×7 transactions; reduced dependency on cash and physical banking; and lower transaction costs

- Digital payments improve transaction efficiency and reduce time and operational costs, benefiting both consumers and businesses.

- Boost to Economic Growth: Promotes formalization of the economy; increases tax compliance and transparency; and enhances ease of doing business.

- Digital payments contribute to economic development by improving financial flows and reducing leakages.

- Empowerment of Small Businesses and MSMEs: Easy onboarding via QR codes and mobile apps; access to digital transaction history for credit eligibility; and increased participation in the formal economy.

- Transparency and Reduction in Corruption: Minimizes cash handling and informal transactions; creates digital audit trails; and reduces leakages in welfare schemes.

- Digital Economy and Innovation Boost: Growth of FinTech ecosystem; integration with e-commerce, gig economy, and services; and encourages innovation in payment solutions, credit delivery, and financial products.

- Inclusion of Rural and Marginalized Sections: UPI and Aadhaar-based payments enable access in remote areas; and bridges the urban-rural divide.

- Digital payments have significantly improved rural financial participation and service delivery.

- Global Leadership and Soft Power: India leads in real-time digital transactions globally; and UPI is being exported internationally (cross-border payments).

- Positions India as a global model for digital public infrastructure.

Concerns and Issues in India’s Digital Payment Ecosystem

- Rising Cyber Fraud and Security Risks: Sharp increase in digital payment frauds, especially UPI-related scams;

- Growth of Authorised Push Payment (APP) frauds (social engineering)

- Phishing, fake apps, identity theft;

- Fraud cases increased from 0.26 million (2021) to 2.8 million (2025).

- Annual fraud value exceeds ₹22,000 crore.

- Transactions above ₹10,000 contribute about 98.5% of total fraud value.

- Data Privacy and Protection Concerns: Risks of data breaches and misuse of personal financial data; inadequate awareness about data-sharing practices; and concerns around Aadhaar linkage and surveillance.

- Digital Divide and Exclusion: Limited access to smartphones, internet connectivity, and digital literacy; Rural and elderly populations face barriers.

- Despite growth, digital inequality continues to restrict inclusive adoption.

- Lack of Digital Literacy and Awareness: Users often unaware of fraud risks, and safe digital practices leading to vulnerability to scams.

- Low financial and digital literacy directly increases fraud susceptibility.

- Infrastructure and Technical Issues: Network failures and transaction delays; system outages due to high volume; and dependence on stable internet connectivity.

- These issues affect reliability and user experience, especially in rural areas.

- Regulatory and Institutional Challenges: Coordination challenges between RBI; Banks; and FinTech companies.

- Regulatory frameworks often lag behind innovation, creating gaps.

- Overdependence on Technology: System vulnerabilities to cyberattacks, technical failures, and risk of systemic disruption.

- A highly digitized system increases systemic risk if safeguards are weak.

Safeguarding India’s Digital Payment Ecosystem

- RBI’s Payment Security Framework: Mandatory cybersecurity guidelines for banks and payment operators; regular audits, compliance checks, and risk assessments; and strengthening of data protection and fraud monitoring systems.

- RBI Discussion Paper on Fraud Prevention (2024–25): Key proposals include:

- Cooling-off period for high-value transactions;

- Additional authentication (trusted person mechanism);

- Transaction caps for risky accounts;

- Whitelisting of beneficiaries;

- Payments Vision 2025: Focus on security and resilience, user protection, and technological innovation; to promote safe, secure, and inclusive payment systems.

- AI-Based Fraud Detection: Use of machine learning and real-time analytics; and behavioral monitoring to detect anomalies.

- Tokenization and Encryption: Card tokenization reduces exposure of sensitive data; and end-to-end encryption ensures secure transactions.

- Real-Time Monitoring Systems: Continuous transaction surveillance; and instant alerts for suspicious activities.

- Regulatory Sandbox: Allows testing of fintech innovations in a controlled environment; and balances innovation with consumer protection.

- Strengthening Banking Infrastructure: Investments in cybersecurity tools, fraud analytics, and incident response systems.

- Consumer Protection Initiatives:

- Zero Liability Protection: Customers protected against unauthorized transactions (subject to conditions)

- Compensation Mechanisms: RBI mandates timely compensation for failed transactions and fraud cases

- Grievance Redress Systems: Ombudsman scheme, and faster dispute resolution frameworks.

- Awareness and Digital Literacy Campaigns:

- ‘RBI Kehta Hai’ Campaign: Educates users about safe digital practices.

- Cyber Awareness Initiatives: Grassroots campaigns; and cyber volunteers and awareness drives.

- Other Initiatives:

- Central Bank Digital Currency (CBDC): RBI’s Digital Rupee aims to provide a secure alternative to private digital payments

- Strengthening Data Protection: Emphasis on privacy laws and data governance frameworks

- Cross-Border Payment Security: Secure integration of UPI with global systems

Conclusion & Way Forward

- India has adopted a multi-layered strategy to safeguard its digital payment ecosystem, combining regulation, technology, consumer protection, and awareness.

- As fraud risks evolve, the focus must remain on proactive, technology-driven, and user-centric safeguards to ensure sustainable growth.

- A balanced approach combining technology, regulation, and awareness is essential to sustain UPI’s growth while mitigating risk. These include:

- Targeted safeguards instead of blanket restrictions

- Opt-out provisions to preserve user autonomy

- Strengthened digital literacy programs

- Enhanced institutional coordination among banks, RBI, and law enforcement.

| Daily Mains Practice Question [Q] India’s digital payment ecosystem has achieved scale but faces rising security challenges. Discuss the growth of digital payments in India and evaluate the effectiveness of safety mechanisms. |

Previous article

India’s Opportunity In a Shifting World Order

Next article

India’s Heat Crisis & Mapping Legislative Vacuum