Syllabus: GS2/Governance; GS3/Infrastructure

Context

- Recent disruptions in India’s aviation sector like the Ahmedabad plane crash in June 2025 and large-scale IndiGo flight cancellations and delays in December 2025, exposed deeper structural risks that the problem is no longer temporary or airline-specific.

About India’s Civil Aviation

- It has emerged as one of the fastest-growing aviation markets in the world, currently ranked as the third-largest domestic aviation market globally.

- It operates over 840 aircraft and carries more than 350 million passengers annually.

- Air travel has transformed from a luxury into an essential mode of transport with rising incomes, expanding middle-class aspirations, and improved regional connectivity.

Rapid Expansion of Domestic Air Travel

- Over the past decade, India’s aviation market has expanded at a remarkable pace. Key drivers include:

- Rising disposable incomes and increased urban mobility;

- Low-cost carrier (LCC) dominance, making flying affordable;

- Infrastructure development, including new airports and terminal expansions;

- Government initiatives like the UDAN scheme, aimed at regional connectivity;

- The Ude Desh ka Aam Nagrik (UDAN) scheme has operationalised hundreds of routes, bringing air travel to Tier-2 and Tier-3 cities and enhancing economic integration across regions.

- Projections suggest that domestic passenger traffic could reach 715 million annually by 2030, reflecting continued strong demand.

- Parliamentary estimates suggest the need for 7,000 new pilots between 2024 and 2026, rising to 25,000–30,000 over the next decade.

Concerns & Issues in India’s Aviation Industry

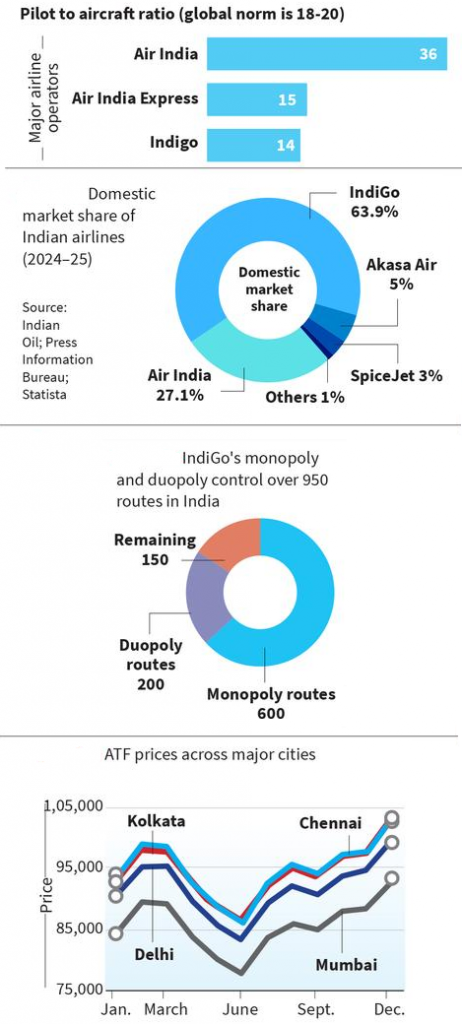

- Inadequate Pilot-to-Aircraft Ratio: Global benchmarks suggest 18–20 pilots per narrow-body aircraft for fatigue-mitigated operations, while Indian carriers often operate closer to 14–16.

- Stricter Flight Duty Time Limitation (FDTL) Norms: Recent enforcement of tighter duty-time rules, reducing night operations and increasing mandatory rest has exposed scheduling vulnerabilities.

- Airlines operating at high utilisation levels struggle to adapt without cancellations and delays.

- Training Bottlenecks: Pilot training infrastructure remains insufficient as limited simulator capacity, high training costs, regulatory delays, and shortage of instructors.

- It creates a structural supply constraint that cannot be resolved quickly.

- High Market Concentration (Duopoly Risk): India’s domestic aviation market is dominated by two groups i.e. IndiGo and Air India, controlling nearly 90% of passenger traffic.

- It affects national connectivity rather than merely shifting passengers to competitors when a dominant airline faces operational disruption.

- Disruptions result in complete connectivity loss, particularly affecting Tier-2 and Tier-3 cities.

- Financial Fragility: Despite strong passenger growth, Indian airlines operate on low margins due to intense fare competition, high operating costs, and currency fluctuations.

- Aviation Turbine Fuel (ATF) prices are linked to global crude oil markets and the US dollar. Sudden spikes significantly impact airline profitability.

- India has witnessed multiple airline collapses and several regional carriers. It reflects structural financial instability within the industry.

- Infrastructure Constraints: Major airports such as Delhi and Mumbai operate near capacity, causing slot shortages, taxi-time delays, and airspace congestion.

- Many regional airports lack adequate passenger facilities, night landing capabilities, and advanced navigation systems.

- Regulatory and Oversight Challenges: The Directorate General of Civil Aviation (DGCA) faces vacancies in technical and safety oversight positions.

- Operational disruptions are often managed through temporary exemptions rather than strict systemic correction.

- It raises concerns about oversight capacity in a rapidly expanding sector.

- Overutilisation of Assets: Indian airlines operate with minimal buffer capacity like high aircraft utilisation rates, limited spare crew availability and tight turnaround schedules.

- Globally, airlines maintain 20–25% spare crew capacity to absorb shocks.

- Regional Airline Sustainability: New regional carriers aim to improve connectivity, but past failures show persistent challenges like weak demand on certain routes, high fixed costs, competitive pressure from dominant airlines, and fuel and currency volatility.

- Rising Demand vs. System Readiness: India accounts for over 4% of global air traffic, and passenger numbers are projected to more than double by 2030.

- However, training capacity is limited, regulatory resources are stretched, infrastructure upgrades are ongoing but uneven, safety buffers remain thin.

Efforts and Initiatives to Overcome Issues in India’s Aviation Industry

- Strengthening Pilot Availability and Training: The government has encouraged the establishment of new Flying Training Organisations, including at underutilised airports. It aims to:

- Increase Commercial Pilot Licence (CPL) output;

- Reduce dependence on foreign training academies;

- Lower training costs over time;

- Implementation of Revised FDTL Norms: The phased rollout of stricter FDTL norms is designed to reduce pilot fatigue, improve safety standards and align India with global best practices.

- Development of Greenfield Airports: New airports such as Noida International Airport (Jewar) and Navi Mumbai International Airport are expected to reduce congestion at major hubs, increase slot availability, and support regional growth.

- Modernisation of Existing Airports: Public-private partnerships (PPP) have accelerated terminal expansion, runway upgrades, and passenger facility improvements at major airports.

- Promoting Regional Connectivity (UDAN Scheme): The UDAN (Ude Desh ka Aam Nagrik) initiative remains a cornerstone policy. Key features include:

- Viability Gap Funding (VGF) for airlines operating on regional routes;

- Reduced airport charges for smaller cities;

- Revival of unserved and underserved airports;

- Encouraging Market Competition and New Entrants: The issuance of No Objection Certificates (NOCs) to new regional airlines reflects policy intent to:

- Reduce overdependence on dominant carriers;

- Improve service frequency in Tier-2 and Tier-3 cities;

- Diversify capacity across regions;

- Enhancing Regulatory Oversight: Efforts are underway to fill technical vacancies within the DGCA to strengthen safety audits and oversight mechanisms.

- The DGCA has intensified inspections, audits, and compliance monitoring, particularly concerning FDTL adherence, aircraft maintenance standards, and operational safety procedures.

- Financial and Structural Reforms: The consolidation of weaker carriers into stronger groups (e.g., Vistara’s merger into Air India) is aimed at creating financially robust entities capable of absorbing shocks.

- New-generation aircraft orders promise better fuel efficiency, lower operating costs, and improved environmental performance.

- Improving Operational Resilience: Airlines are gradually reassessing crew-to-aircraft ratios to better absorb disruptions under stricter FDTL norms. India is promoting domestic Maintenance, Repair and Overhaul (MRO) facilities to reduce aircraft downtime, lower foreign exchange outflows, and improve maintenance turnaround times

- Air Traffic Management Modernisation: The government is investing in advanced air navigation systems, satellite-based navigation (GAGAN), and airspace redesign initiatives.

- These measures aim to reduce congestion, improve fuel efficiency, and enhance safety in crowded corridors.

- Liberalised Foreign Pilot Hiring (Temporary Measure): To ease immediate shortages, temporary approvals have been granted for foreign pilots.

Conclusion

- India’s aviation sector stands at an inflection point. With market concentration high, pilot supply constrained, regulatory capacity stretched, and safety notices rising, the industry needs to shift from aggressive expansion to resilience-building.

- If corrective action is delayed, the cost will not just be financial losses for airlines, it will be borne by millions of passengers and by the credibility of one of India’s fastest-growing sectors.

| Daily Mains Practice Question [Q] Examine the structural, regulatory, and market-related challenges confronting India’s aviation industry. Substantiate your answer with relevant arguments and examples. |

Next article

Moving Up the Global Value Chain