Syllabus: GS3/Economy

Context

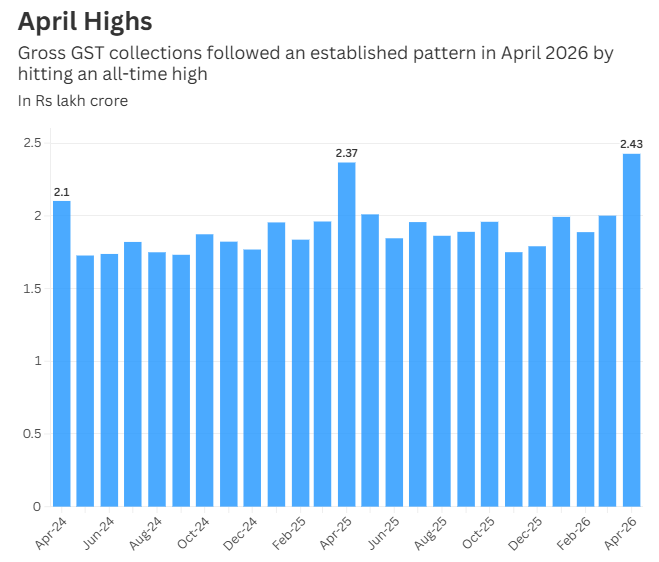

- The government’s Goods and Services Tax (GST) revenue in April 2026 surged to an all-time high of Rs 2.43 lakh crore, up 8.7% over April last year.

About

- The growth was once again driven by collections on imports, with revenue from domestic sales growing slower.

- Collections in April typically come in higher as both industry and the tax administration make a final push to achieve the financial year-end targets.

Goods and Services Tax

- The GST was introduced in 2017 by the 101st Constitutional Amendment Act, 2016 as a comprehensive indirect tax for the entire country.

- It is a destination based tax on consumption of goods and services.

- It is levied at all stages right from manufacture up to final consumption.

- Only value addition will be taxed and the burden of tax is to be borne by the final consumer.

- It accrues to the State or the Union Territory where the consumption takes place. It is of 3 types:

- Central GST (CGST): Levied by the Center.

- State/Union Territory GST (SGST/UTGST): Levied by States or UTs.

- Integrated GST (IGST): Tax levied and collected by the Center on all inter-state supplies of goods and/or services.

- The Center settles accounts with the States/UTs by transferring the SGST/UTGST portion of IGST to the destination state where goods/services were consumed.

- Three slabs for taxes for both goods and services: 5%, 18% and 40%.

- Different tax slabs were introduced because daily necessities could not be subject to the same rate as luxury items.

- The GST Council is a constitutional body under Article 279A.

- It is a federal body comprising the Union Finance Minister as its Chairman and Finance Ministers of all States as members.

- The GST Council members take almost all decisions on GST with consensus.

- Exempted Items: The GST applies to all goods other than alcoholic liquor for human consumption and five petroleum products (common for the Center and the States): petroleum crude, motor spirit (petrol), high speed diesel, natural gas, aviation turbine fuel.

GST 2.0 Reforms

- Simpler Tax Structure: The move to a three-slab GST regime (5%, 18% and 40%) reduces complexity, classification disputes, and compliance costs.

- MSME and Startup Enablement: Faster refunds, simplified registration and returns, and lower input costs aim is to boost the present businesses and startups and incentivise the youth to enter into businesses and initiate startups.

- Wider Tax Base and Revenue Stability: Simpler rates and improved compliance have expanded the GST taxpayer base to over 1.5 crore, while gross collections also increased, reinforcing fiscal sustainability.

Conclusion

- The 2025 GST reforms mark a transformative chapter in India’s journey toward inclusive economic growth and youth empowerment.

- By rationalising rates across diverse industries, the government has not only eased the cost of living but also fostered new opportunities for startups, MSMEs, and job seekers.

- Collectively, the reforms reaffirm India’s commitment to making taxation simpler, fairer, and more growth-oriented – ensuring that young citizens are at the heart of the nation’s economic future.

Source: TH

Previous article

News In Short 01-05-2026

Next article

Fiscal Position of States