Syllabus: GS3/Economy; GS3/ Environment

Context

- India’s bioeconomy needs capital-market innovation, regulatory modernisation and strategic blend of innovation to achieve $1.2 trillion by 2047.

About Bioeconomy

- As per Food and Agriculture Organization (FAO), the bioeconomy is the production, utilization and conservation of biological resources, including related knowledge, science, technology, and innovation, to provide information, products, processes and services across all economic sectors aiming toward a sustainable economy.

Status of India’s Bioeconomy

- India’s bioeconomy has witnessed exponential growth, expanding 16-fold in a decade, from $10 billion in 2014 to over $165 billion in 2024, and it aims to contribute about $1.2 trillion by 2047.

- As per the India BioEconomy Report 2024, the sector contributes 4.25% to India’s GDP, signalling its rising centrality in national development.

- It has been fueled by advances in biotechnology, pharmaceuticals, agriculture, and bioenergy, supported by a growing startup ecosystem and government support.

- In Ethanol, India is now the third-largest producer of blended ethanol, with production almost tripling in five years, supporting both energy security and decarbonization efforts.

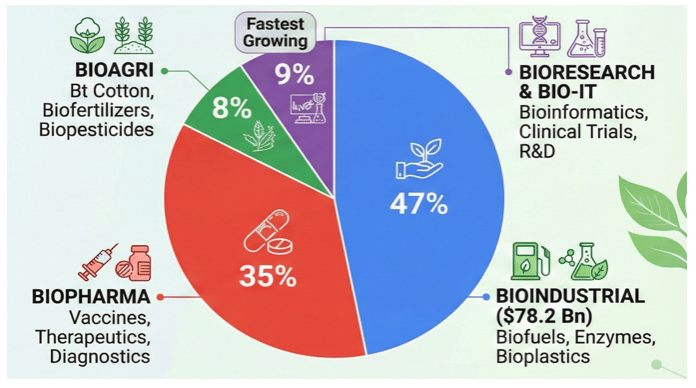

Key Sectors Driving the India’s Bioeconomy

- Biopharma: India is already a global leader in generics and vaccines, and it is focusing on biologics, biosimilars, and personalized medicine.

- Agricultural Biotechnology: Innovations in crop genetics, biofertilizers, and precision farming can enhance food security and sustainability.

- Bioenergy & Biofuels: Bioethanol and biogas offer scalable alternatives to fossil fuels, with a push for clean energy

- Industrial biotechnology: Enzymes, bioplastics, and green chemicals are gaining traction as eco-friendly industrial inputs.

- India can build thousands of deep-tech start-ups, lead globally in mRNA, RNAi, gene therapy, biosimilars, and biologics, emerge as a preferred global hub for clinical research and bio-manufacturing, generate millions of high-value jobs under the BioE³ framework, and realise a $1.2 trillion bioeconomy by 2047.

India’s Push For Expanding Bioeconomic Architecture

- BioE3 Policy: The BioE3 policy (Biotechnology for Economy, Environment, Employment) acts as a unifying strategy to propel biomanufacturing, focusing on six domains—ranging from bio-based chemicals to functional foods, carbon capture, precision biotherapeutics, climate-smart agriculture, and even marine/space bio-research.

- Other Key Measures: National Mission on Bioeconomy (2016), National Biopharma Mission, Bio-RIDE, BioNEST incubators, Global Biofuels Alliance & National Biological Data Centre (NBDC).

Hindrances to Reach $1.2 Trillion by 2047

- India’s Structural Bottleneck: India does not permit pre-revenue or research-stage biotech companies to list publicly. Consequently:

- Innovators rely heavily on private, risk-averse capital.

- Valuations remain suppressed.

- High-potential start-ups relocate abroad, seeking more supportive ecosystems.

- Regulatory Inefficiencies: Cumbersome approval processes for biotech products delay innovation and commercialization.

- Lack of a single-window clearance system for biotech startups and research trials creates uncertainty.

- First-in-Human (FIH) trial approvals take months. Each trial phase requires fresh Subject Expert Committee (SEC) review.

- CDSCO lacks scientific capacity to assess emerging modalities like mRNA, CRISPR, CAR-T, and gene therapies.

- Limited Capital Market Access: Biotech startups struggle to raise early-stage and scale-up funding due to high R&D risks and long gestation periods.

- India lacks a robust biotech IPO pipeline, unlike the US and China, where public markets actively support biotech innovation.

- Fragmented Innovation Ecosystem: Weak industry-academia linkages hinder translational research and product development.

- Many innovations remain trapped in labs due to poor commercialization pathways and limited tech transfer infrastructure.

- Inadequate Infrastructure: Shortage of biomanufacturing facilities, especially for biologics, diagnostics, and advanced therapeutics.

- Policy and Coordination Gaps: Multiple ministries (Science & Tech, Health, Agriculture, Environment) operate in silos, leading to policy fragmentation.

- Absence of a centralized bioeconomy mission or roadmap with measurable milestones hampers strategic alignment.

Key Suggestions For Achieving Bioeconomy $1.2 Trillion by 2047

- Regulatory Reform: India’s current drug-regulation system — led by CDSCO — remains slow, fragmented, and bureaucratic.

- Even with capital access, innovation will stagnate without regulatory speed and scientific clarity.

- Need of Innovation & Biotech Board: India urgently needs a dedicated listing board on the NSE and BSE, modelled on NASDAQ, STAR, and Hong Kong’s Biotech Chapter.

- It could unlock domestic capital, draw global institutional investors, and become the financial engine of India’s bioeconomy.

- Such a platform should:

- Allow pre-revenue and research-stage biotech listings.

- Enable IP-led companies to access patient capital.

- Attract global investors to India’s science story.

- Encourage domestic scaling instead of foreign migration.

- Focus on Innovation: Both capital-market reform and regulatory reform together can drive innovation that powers global biotech leadership. It needs:

- A dedicated Innovation & Biotech Board;

- A science-led dual-agency regulatory system; and

- Strong institutional support.

Two-Pillar Model for India

- Empower ICMR for Scientific Review: ICMR’s research depth and ethical infrastructure make it ideal for evaluating early-stage drugs, vaccines, diagnostics, and advanced biologics.

- Position CDSCO as Licensing Authority: CDSCO should focus on final approvals, GMP compliance, site inspections, and pharmacovigilance.

- Separation of scientific assessment (ICMR) and administrative licensing (CDSCO) could reduce approval timelines, improve scientific rigour, and reinforce investor confidence.

| Case Study of China – Capital Innovation Fuels Scientific Innovation: 1. STAR Market (Shanghai, 2019): Enabled pre-revenue deep-tech firms to list without profitability requirements, mobilising $130+ billion. 2. Hong Kong Biotech Chapter (2018): Allowed non-revenue biotech IPOs; over 70 companies listed, raising $25 billion. 3. Venture Capital Inflows (2018–2022): $45 billion in life sciences — nearly 10 times India’s inflows. 4. Pharma R&D Investment: Surpassed $20 billion, compared to India’s $3 billion. – China faced regulatory hurdles, similar to India, a decade ago but acted decisively: 1. Reformed NMPA into a science-led regulator. 2. Introduced time-bound review pathways, cutting trial approval times by 40–60%. 3. Allowed parallel review of trial phases. 4. Aligned with ICH global standards. 5. Fast-tracked advanced modalities, approving multiple CAR-T and gene therapies before Western counterparts. – This regulatory agility created predictability, which built investor confidence, fueling China’s biotech surge. |

Conclusion

- India stands at a decisive juncture. We have the science, the talent, and the market. What remains is the courage to reform.

- Capital-market innovation and regulatory modernisation must be treated as national priorities.

- India can evolve from the pharmacy of the world to the lab of the world — leading global biotech innovation, not just supplying it with bold action.

| Daily Mains Practice Question [Q] Discuss the opportunities and challenges India faces in realizing its bioeconomic potential by 2047. What strategic initiatives and sectoral transformations are necessary to achieve this goal? |

Previous article

A Dismantling of the Base of Environmental Regulation

Next article

Need To Recalibrate India’s Export Strategy