Syllabus: GS3/Agriculture; Economy

Context

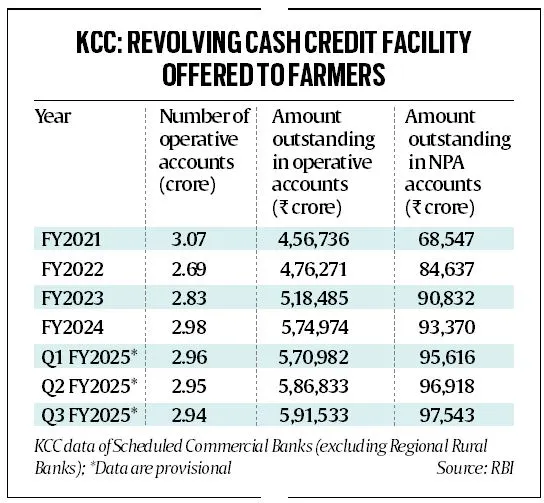

- Recent data reveals that bad loans under the Kisan Credit Card (KCC) scheme have surged by 42% over the past four years, highlighting the financial stress in the agricultural sector.

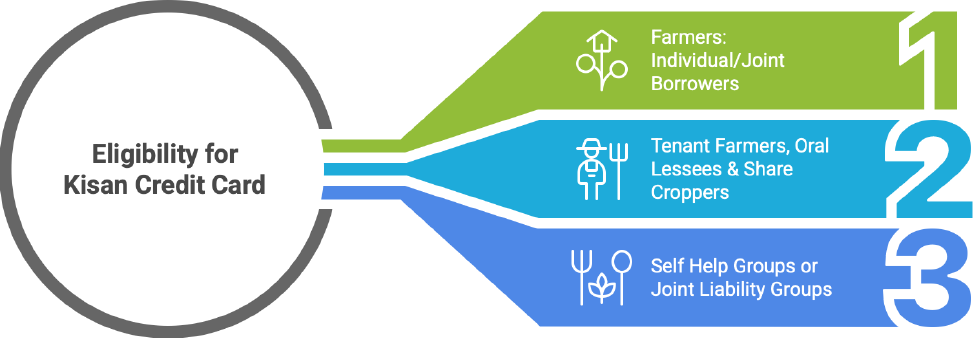

Understanding Kisan Credit Card (KCC) Scheme (1998)

- About: It is designed to provide short-term credit to farmers for agricultural and allied activities, based on the recommendations of the R.V. Gupta Committee.

- Features:

- Issued by commercial banks, cooperative banks, and regional rural banks.

- Covers crop production needs (seeds, fertilizers, pesticides, etc.).

- Includes working capital for allied activities like dairy, poultry, and fisheries.

- Can be used for farm machinery, irrigation, and post-harvest expenses.

- A KCC loan is classified as NPA if unpaid within three years of disbursal.

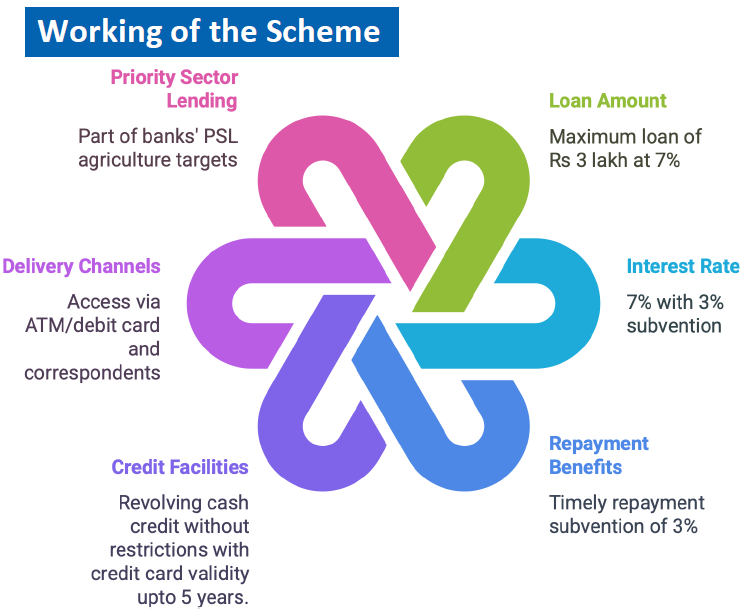

- Working of KCC Scheme:

| About Non-Performing Assets (NPAs) – These refer to loans or advances for which the principal or interest payment remains overdue for more than 90 days. Types – Substandard Assets: NPA for less than or equal to 12 months. – Doubtful Assets: NPA for more than 12 months. – Loss Assets: Unrecoverable loans, identified by the bank or RBI. RBI Guidelines For Agricultural Loans (as NPAs) – Short-term crop loans are considered NPAs if payment is overdue for two crop seasons. – Long-term agricultural loans become NPAs if overdue for one crop season. |

Current Trends in Agricultural NPAs

- According to data from the RBI, the outstanding NPAs in KCC accounts of scheduled commercial banks (excluding regional rural banks) increased from ₹68,547 crore at the end of March 2021 to ₹97,543 crore by December 2024.

- It underscores the growing challenges faced by farmers in repaying their loans.

Major Causes of Rising NPAs in Agriculture

- Unpredictable Weather and Climate Change: Erratic rainfall, frequent droughts, floods, and changing weather patterns directly impact crop yields, making it difficult for farmers to repay loans.

- With limited insurance coverage, crop failures lead to defaults on agricultural credit.

- Low Farm Income and Market Volatility: Despite government support, farmers often struggle with low productivity and unremunerative prices.

- Market price fluctuations, lack of assured MSP for all crops, and inadequate procurement mechanisms contribute to financial distress.

- Loan Waiver Schemes and Moral Hazard: State and central governments frequently announce loan waivers as a relief measure, encouraging willful defaults.

- Farmers often anticipate future waivers, leading to poor repayment discipline.

- Inadequate Risk Management by Banks: Banks are sanctioning loans without sound risk assessment.

- Structural Weakness in Agricultural Finance: Small and marginal farmers, who form 86% of India’s farming community, have limited access to institutional credit.

- Dependence on informal moneylenders results in debt traps and an inability to repay formal loans.

- Delay in Crop Insurance Settlements: Pradhan Mantri Fasal Bima Yojana (PMFBY) has faced delays in claim settlements, leaving farmers unable to repay loans.

Implications of Rising Agricultural NPAs

- Stress on Banking System: High NPAs reduce the ability of banks to extend fresh loans, impacting overall agricultural credit growth.

- RRBs and Cooperative Banks, which primarily cater to farmers, suffer from financial instability.

- Increased Fiscal Burden: The government often compensates banks for loan waivers, straining fiscal resources and diverting funds from productive rural investments.

- Economic and Social Distress: Indebtedness is a key reason behind farmer suicides, particularly in states like Maharashtra, Karnataka, and Punjab.

- Rising NPAs lead to rural distress, impacting employment and food security.

- Credit Crunch for Genuine Farmers: Due to higher default rates, banks tighten credit norms, making it difficult for genuine, creditworthy farmers to access loans.

Measures to Address Rising Agricultural NPAs

- Strengthening Crop Insurance and Risk Mitigation: Faster claim settlements under PMFBY and expansion of insurance coverage can reduce financial distress.

- Promoting climate-resilient farming and crop diversification can mitigate weather-related risks.

- Improving Credit Discipline: Restricting loan waivers to genuinely distressed farmers and ensuring targeted relief can prevent willful defaults.

- Encouraging timely repayment incentives, such as interest rate discounts, can improve repayment behavior.

- Enhancing Institutional Credit Access:Expanding Kisan Credit Card (KCC) coverage to all small and marginal farmers.

- Strengthening Farmer Producer Organizations (FPOs) to ensure collective bargaining for better credit access.

- Online application through banks’ websites & Common Service Centers (CSCs).

- Integration with PM-KISAN and Aadhar for easier verification.

- Strengthening Bank Supervision and Credit Monitoring: Implementing technology-driven loan tracking to identify early signs of distress.

- Increasing financial literacy programs to educate farmers on loan management and risk mitigation.

- Encouraging Diversification and Value-Addition: Promoting agribusiness, food processing, and non-farm activitie

- Strengthening supply chains and storage infrastructure to minimize post-harvest losses.

Previous article

The Rise of Quick Commerce in India

Next article

Gene-Edited Bananas