Syllabus: GS3/Economy

Context

- Recently, the Union Minister for Finance and Corporate Affairs tabled the Economic Survey 2025-26 in Parliament.

What is an Economic Survey?

- It is an official annual document that reviews the state of the Indian economy over the past year and outlines key economic trends, challenges, and policy directions.

- It is prepared by the Economic Division, Department of Economic Affairs (DEA), Ministry of Finance, under the supervision and guidance of the Chief Economic Adviser (CEA).

- It is tabled in Parliament just before the Union Budget every year.

- It typically covers:

- Overview of the Economy: GDP growth, Inflation, Employment trends, Fiscal deficit, External sector (exports, imports, forex reserves).

- Sector-wise Analysis: Agriculture, Industry, Services

- Public Finance: Government revenue and expenditure, Tax performance, Subsidies and welfare spending

- Social Sector: Education, Health, Poverty and inequality, Human development indicators

- Special Themes: Each year, the Survey focuses on one or two major themes, such as climate change & green growth, digital economy, inclusive growth, productivity and reforms.

Highlights of Economic Survey 2025-26

- Global Context and India’s Growth Advantage: The global economy remains fragile, marked by geopolitical tensions, trade fragmentation, and financial vulnerabilities.

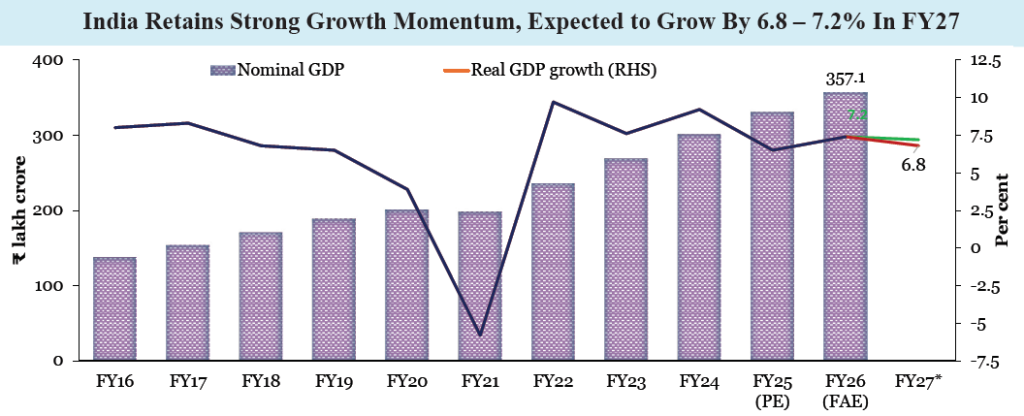

- India stands out as the fastest-growing major economy for the fourth consecutive year.

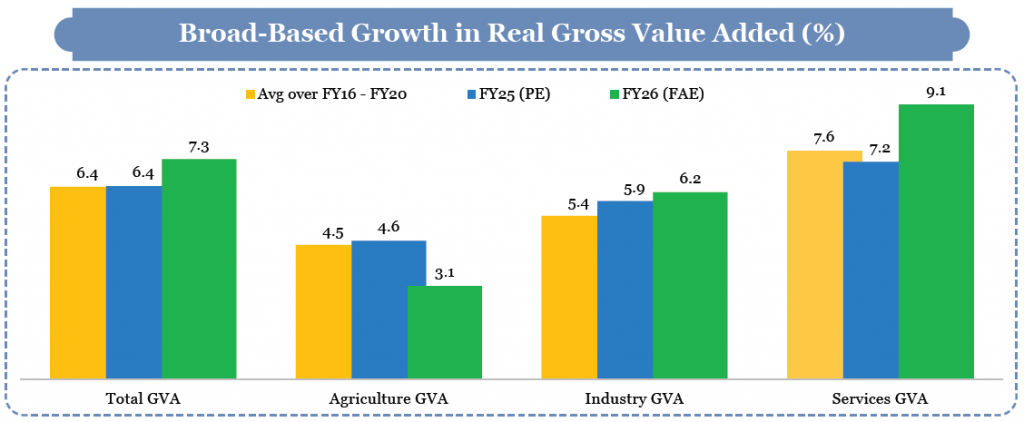

- As per the First Advance Estimates, real GDP growth in FY26 is pegged at 7.4%, with Gross Value Added (GVA) growth at 7.3%, underlining strong domestic fundamentals.

- Demand-Led Growth: Consumption and Investment

- Consumption Momentum: Private Final Consumption Expenditure (PFCE) grew 7.0% in FY26, reaching 61.5% of GDP, the highest level since 2012.

- It reflects low and stable inflation, steady employment conditions, and rising real incomes.

- Strong agricultural output boosted rural consumption, while tax rationalisation and income growth supported urban demand, indicating broad-based consumption recovery.

- Investment Revival: Gross Fixed Capital Formation expanded by 7.8%, maintaining a 30% share of GDP. Investment growth was supported by sustained public capital expenditure, and renewed private sector investment, reflected in corporate announcements.

- Consumption Momentum: Private Final Consumption Expenditure (PFCE) grew 7.0% in FY26, reaching 61.5% of GDP, the highest level since 2012.

- Sectoral Performance: Services Lead, Industry Accelerates

- Services as the Growth Engine: Services remain the primary driver of growth:

- GVA growth of 9.3% in H1 FY26

- Estimated 9.1% growth for the full year: Services now account for 56.4% of total GVA, driven by modern, tradable, and digitally delivered services.

- Industry and Manufacturing Upswing: Industrial activity strengthened despite global headwinds:

- Industry GVA grew 7.0% in H1 FY26

- Manufacturing GVA accelerated to 7.72% in Q1 and 9.13% in Q2

- Production Linked Incentive (PLI) schemes have attracted over ₹2 lakh crore in investments, generated ₹18.7 lakh crore in incremental output, and created over 12.6 lakh jobs.

- Services as the Growth Engine: Services remain the primary driver of growth:

- Fiscal Developments: Credibility Through Consolidation

- Prudent fiscal management strengthened macroeconomic stability and led to three sovereign credit rating upgrades in 2025.

- Key fiscal trends include:

- Centre’s revenue receipts rising to 9.2% of GDP in FY25

- Non-corporate tax collections increasing from 2.4% (pre-pandemic) to 3.3% of GDP

- Income tax filers increasing from 6.9 crore (FY22) to 9.2 crore (FY25)

- Public capital expenditure rose sharply:

- Effective capital expenditure reached 4% of GDP in FY25

- States were incentivised through targeted assistance to sustain capex

- India reduced its general government debt-to-GDP ratio by 7.1 percentage points since 2020, while maintaining high investment levels.

- Monetary Management and Financial Intermediation

- Banking Sector Strength: Asset quality of scheduled commercial banks improved significantly, with GNPA at 2.2% and net NPA at 0.5% (September 2025).

- Credit growth accelerated to 14.5% YoY by December 2025.

- Financial Inclusion: Flagship schemes expanded access to finance:

- PMJDY: 55.02 crore accounts;

- PMMY: ₹36.18 lakh crore disbursed across 55.45 crore loans;

- Stand-Up India and PM SVANidhi strengthened entrepreneurship;

- Capital Markets and Regulation: Demat accounts crossed 21.6 crore, with women comprising nearly a fourth of investors.

- Mutual fund participation expanded beyond metros.

- The IMF-World Bank FSAP (2025) validated India’s resilient, well-capitalised financial system.

- Banking Sector Strength: Asset quality of scheduled commercial banks improved significantly, with GNPA at 2.2% and net NPA at 0.5% (September 2025).

- External Sector: Resilience in a Volatile World

- India’s share in global merchandise exports rose to 1.8%, and services exports to 4.3%.

- Total exports hit a record USD 825.3 billion in FY25, led by services.

- Current Account Deficit remained moderate at 1.3% of GDP (Q2 FY26).

- Remittances reached USD 135.4 billion, the highest globally.

- Forex reserves stood at USD 701.4 billion, covering ~11 months of imports.

- India ranked 4th globally in Greenfield investments and emerged as the largest destination for digital Greenfield projects (2020-24).

- Inflation

- India recorded its lowest-ever CPI inflation, with average headline inflation at 1.7% (April–December 2025).

- It was driven by declining food and fuel prices, and effective supply-side management.

- India saw one of the largest declines in inflation during 2025 among emerging economies.

- India recorded its lowest-ever CPI inflation, with average headline inflation at 1.7% (April–December 2025).

- Agriculture and Food Management

- Foodgrain production reached 357.7 million tonnes in AY 2024-25.

- Horticulture output surpassed foodgrains at 362.08 MT, accounting for 33% of agricultural GVA.

- Digital and market reforms expanded the reach of e-NAM, covering 1.79 crore farmers.

- Income support continued through MSP, PM-KISAN (₹4.09 lakh crore disbursed) and PMKMY pensions.

- Industry and Manufacturing

- Industry GVA grew 7.0% in H1 FY26, with manufacturing accelerating to 9.13% in Q2.

- PLI schemes attracted ₹2 lakh crore investment and generated 12.6 lakh jobs.

- India’s Global Innovation Index rank improved to 38th (2025).

- Semiconductor Mission approved projects worth ₹1.6 lakh crore.

- Human Capital: Education, Health and Skills

- Education: 24.69 crore students enrolled across 14.71 lakh schools; Higher education institutions increased to 70,018; NEP reforms enabled flexible learning, credit portability and skills integration;

- Health: MMR declined by 86% since 1990; IMR reduced to 25 (2023); Under-five mortality declined by 78%;

- Employment, Skills and Social Progress: 56.2 crore employed in Q2 FY26;

- Organised manufacturing added 10 lakh jobs in FY24;

- e-Shram registered 31 crore workers, over 54% women;

- Social services expenditure rose to 7.9% of GDP (FY26 BE);

- Rural Development and Social Progress

- Poverty levels declined significantly under revised global benchmarks. Social services expenditure rose to 7.9% of GDP, while rural asset ownership, digital mapping, and women-led initiatives strengthened grassroots economic participation.

- Emerging Frontiers: AI, Urbanisation, and Strategic Resilience

- India’s AI ecosystem is evolving around practical, low-cost, and local solutions, enabling adoption across sectors such as agriculture, healthcare, and governance.

- Urban connectivity projects are reshaping labour markets and easing metropolitan pressures.

- Strategically, India is transitioning from narrow import substitution toward strategic resilience and global indispensability, embedding itself deeply into global value chains.

Looking Ahead: Strategic Resilience and Indispensability

- India’s development strategy is evolving from import substitution to strategic resilience and global indispensability.

- A disciplined indigenisation framework, lower input costs, AI diffusion tailored to real-world needs, and integrated urbanisation models are positioning India to move from ‘buying Indian’ to ‘buying Indian without thinking’.

Previous article

News In Short 29-01-2026

Next article

Economic Survey First Time Cites Power Gap Index