In News

- Recently, the Finance Ministry said that the National Asset Reconstruction Company Ltd. (NARCL), set up to take over large bad loans of more than 500 crore from banks, will pick up the first set of such non-performing assets (NPAs) in July.

Background

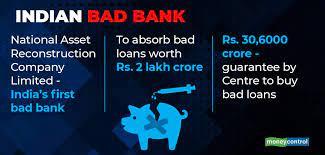

- NARCL is a special purpose asset reconstruction company for taking over the large value NPA accounts (above 500 crore) from banks.

- Its formation was announced in the Union Budget for 2021-22, is intended to resolve stressed loans amounting to about 2 lakh crore, of which fully provisioned assets of about 90,000 crore are expected to be transferred to it from lenders in the first phase.

- NARCL has shareholding from 15 Indian lenders and Canara Bank is the sponsor of this Asset Reconstruction Company (ARC).

- While public sector banks have taken a majority stake in NARCL, India Debt Resolution Company Ltd (IDRCL) will be majorly owned by private sector banks.

- Approvals granted: The NARCL, which will acquire the bad loans from banks, and the India Debt Resolution Company Ltd. which will then manage these assets and seek to enhance their value have secured necessary approvals and permissions.

What is a Bad Bank?

- A bad bank is simply an entity which specialises in handling bad loans or NPAs.

- It is basically an entity which buys the NPAs of commercial banks and tries to recover at least a part of the value of such NPAs.

- Usually, banks discount the book value of NPAs when they are transferred to a bad bank. After that, whatever recovery is possible from the bad loan becomes the earnings of the bad bank.

- Unlike commercial banks, bad banks do not undertake deposits, lending or other usual banking operations.

- Another name for a bad bank is Asset Reconstruction Company (ARC). It is a company which buys the bad loans of banks or any other financial institution, to let them clear their books and resume lending.

Rationale for a bad bank

- Free up resources: Banks have to set aside a part of their operating revenue to cover up for the potential doubtful advances.

- A bad bank can take over the bad loans of the bank, thereby freeing up the bank from the provisioning requirements.

- This means since the banks are not required to provision for the bad loans, the same money can be utilised for lending purposes.

- Incremental lending: Banks take advantage of the fact that a major portion of the deposits lies dormant in the bank accounts.

- This deposit can be used towards lending.

- Similarly, not all advances banks make are withdrawn immediately from the accounts. Therefore, a fraction of such loans can be used to advance further credit. Therefore, the more money banks have, the more they can advance to the needy.

- Specialisation: A bad bank would be specialised in maximising the recovery out of a bad loan, as this would be its primary task.

- In contrast, banks are not in the business of recovery; therefore, their capability to resolve the loans is minimal.

- Economic slowdown: Reports have pointed to a potential increase in stressed assets due to economic slowdown in India. Combined with the COVID-induced lockdown, this may create a situation in which the NPAs might increase to an unsustainable limit.

- Improved sentiment: Industry needs to come out of the crisis it is facing if India is serious about its stated goal of a $5 trillion economy.

- This requires a bullish sentiment in the economy.

- A bad bank can provide such an impetus to the industry by freeing up the books of banks.

- Lesser need for recapitalisation of banks: Recapitalisation of banks is required to fulfil the capital adequacy ratio of the banks.

- With the formation of a bad bank, it is expected that this amount can be utilised elsewhere, including towards public welfare and infrastructure creation.

Issues associated with the bad bank

- Shifting the problem: A bad bank is expected to take over the debts of commercial banks under it. However, to what extent it will be successful in resolving the NPA crisis is not clear. This is because almost all of the remedies which are available in the market have been tried by the existing commercial banks. Therefore, the bad bank can only be expected to aggregate, but not resolve the problem.

- Haircut for the banks: When the bad loans are being taken over by a bad bank, the banks are expected to transfer such a loan at a discount to its original value. In such a scenario, the value of discount might prove to be controversial as both the entities, i.e. commercial bank as well as the bad bank, are being financed by the exchequer and are subject to public scrutiny. Also, banks have been cautious of taking big hair cuts because of the scrutiny from the 3 Cs (CBI, CVC and CAG).

- Losses for the banks: Similar to the last point, the haircuts taken by the banks would reflect on its profit and loss account and affect its profitability. This might raise questions on both the management of the bank as well as its decision making regarding both earlier and future haircuts.

- Fear of unethical practices: Since there would be pressure on the bad bank to perform, it is possible that the employees might turn towards unethical practices to boost recovery out of a bad loan. This has been a continuing problem earlier as there have been reports of harassment of the banks’ clients, who were unable to pay their dues.

Way Forward

- Improve the fundamentals: Experts have consistently pointed to the need for improving the examination process during the initial stages of the lending process.

- Usually the cause of bad loans has been traced to reckless lending undertaken by the banks to meet their lending targets.

- Asset Quality Review: While the spike in NPAs was a result of RBI-mandated Asset Quality Review, it is to be understood that the process was a mere recognition of the extent of the problem facing the financial sector of India. It is important to gauge the extent of the issue if corrective actions are expected to yield results.

- Firm steps required to address the crisis: Government has emphasised on the ‘4R strategy’ to yield result in the resolution of the NPA crisis.

- It constitutes Recognition of NPAs, Resolution of bad loans and recovery of value from the assets, Recapitalisation of the banks by the government and Reforms in the banking sector.

- Apart from that, the government has also come up with various other schemes like Indradhanush plan and Gyan sangam (meeting between government officials and the bank officials to understand and resolve the issues plaguing banking sector.

|

Non Performing Asset (NPA)

Types of NPA

|

Source: TH

Previous article

State of Environment Report 2022

Next article

India-Gulf Relations