Syllabus: GS3/Economy

Context

- The fourth International Conference on Financing for Development (FfD4) is being held in Spain which brings focus on the massive debt burden on developing countries.

- Public Debt or Sovereign debt is the money borrowed by a national government from either domestic or international sources, usually through the issuance of government bonds or loans.

Sovereign debt on Developing Countries

- Since 2010, sovereign debt in developing countries has grown twice as fast in developed economies — with its share in global total increasing to 30% in 2023, from just 16% in 2010.

- As per the World Bank 2024 Report, Developing countries spent a record $1.4 trillion to service their foreign debt as their interest costs climbed to a 20-year high in 2023.

- Currently, more than half of developing countries allocate at least 8% of government revenues to interest payments, a figure that has doubled over the past decade.

- The rising pressure of interest payments is substantial across regions, particularly in Africa and Latin America and the Caribbean.

Reason and Factors Contributing to Debt Burden

- Oil Price Shock (1970s): The 1970s saw a sharp rise in oil prices due to geopolitical tensions, including the 1973 Arab Oil Embargo.

- Oil-importing developing countries faced a financial squeeze due to rising import bills.

- Petrodollar Recycling: Oil-exporting Arab nations deposited their surplus “petrodollars” in Western banks.

- These funds were loaned to developing countries, enabling them to afford higher oil prices and continue purchasing Western exports.

- This system supported Western economies by keeping factories open and avoiding recession.

- Rise of Private Lending: Private Western banks began overtaking official sources (like governments or IMF) in lending.

- By 1982, banks lent $63 billion annually—nearly double the official lending.

- Many developing countries experienced rapid economic growth in the 1970s as a result.

- The Debt Crisis (1980s): A global recession and high interest rates hit in the 1980s.

- Developing countries struggled to repay their debts and began borrowing more just to pay interest—a classic debt trap.

- Case of Brazil: From 1972–1988, Brazil paid $176 billion in interest on a $124 billion debt.

- High Interest: The UNCTAD report showed that developing regions borrow at rates that are 2-4 times higher than those of the US and 6-12 times higher than those of Germany.

- This is largely because developing countries are perceived to have a more “high-risk environment”, and thereby face higher cost of borrowing.

- Biased Sovereign Credit Ratings: Sovereign credit ratings are meant to be independent measures of a country’s ability to pay its debts.

- Such ratings are important because they determine the interest rates a country faces in the global financial market and, therefore, its borrowing costs.

- Sovereign credit ratings are negatively biased towards the Global South.

Read our detailed article on Sovereign Credit Ratings.

Concerns

- Rising Interest Burden: In 2023, a record 54 developing countries (38% of total) allocated 10% or more of their government revenues to interest payments.

- Nearly half of these countries were in Africa, highlighting regional disparities.

- Outpacing Public Spending: Interest payments are increasing faster than critical public expenditures, including on healthcare, education, and infrastructure.

- According to the Centre for Science and Environment (CSE), many low- and middle-income countries (LMICs) now spend more on debt payments than what is needed to meet their climate goals.

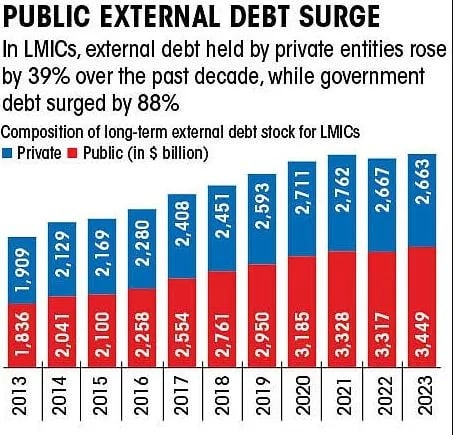

- Growing Debt Service Load: External debt service bills for LMIC governments doubled from $182 billion (2013) to $368 billion (2023).

- For one dollar of Gross National Income (GNI) earned, the average developing economy spent 1.6 cents on external sovereign debt servicing in 2013, which rose to 2.5 cents in 2023.

- For LMICs, the figure increased from 1.8 cents in 2013 to 2.8 cents in 2023.

- Currency and Financial Instability: Heavy external borrowing in foreign currencies exposes countries to exchange rate volatility.

- Loss of Sovereignty and Policy Autonomy: Reliance on International Monetary Fund (IMF) bailouts and bilateral lenders often comes with conditionalities that influence domestic policies.

- Climate and SDG Commitments at Risk: Rising debt diverts resources away from climate finance, sustainable infrastructure, and UN SDG targets.

Recommendations for Debt Management

- Restructuring Debt: First, governments should assess the level of their debt sustainability and their ability to reduce it.

- Restructuring government debt with creditors before debt levels reach highly unsustainable levels would be an advisable move for any government.

- Greater economic growth: To improve economic growth and attract large-scale foreign investment, developing countries need to improve the ease of doing business and reduce red tape.

- Improve tax administration and expand the tax base (e.g., via digital tax compliance, reducing exemptions).

- Encourage financial inclusion to increase savings and investment in the formal economy.

- Strengthen Debt Management Capacity: Build institutional capacity in debt analysis, forecasting, and risk management.

- Use tools like Medium-Term Debt Management Strategies (MTDS) and develop domestic debt markets.

- Foster International Support and Policy Space: Seek enhanced support from IMF, World Bank, and regional development banks via concessional financing and policy advice.

Source: DTE

Previous article

8 Years of Goods and Services Tax (GST)

Next article

10 Years of the Digital India Journey