In News

Recently, Renewable Energy Market Update Report 2021 has stated that India’s renewable energy (RE) capacity addition in 2020 declined by more than 50 per cent since 2019.

Renewable Energy Market Update Report 2021

- It is a report published by the International Energy Agency (IEA).

- It forecasted new global renewable power capacity additions for 2021 and 2022.

- It also provided updated biofuel production forecasts for these years, as the sector suffered significant losses with declining transport demand during the pandemic.

Major Highlights of the Report

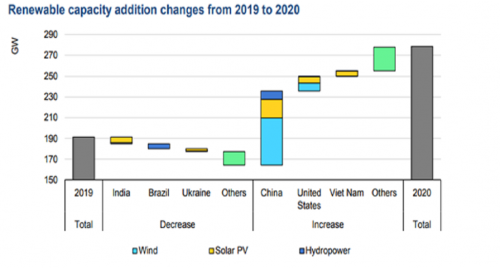

- Global Level

-

- Renewables were the only energy source for which demand increased in 2020 despite the pandemic, while consumption of all other fuels declined.

- Globally, annual renewable capacity additions increased 45 per cent in 2020 to almost 280 gigawatt (GW). It is the highest year-on-year rise since 1999.

- This has been attributed mainly to capacity expansion for solar and wind energy, which amounted to 135GW and 115GW respectively. A 20GW capacity of hydropower and about 10GW of other renewable energy, led by bioenergy, also contributed to the growth.

- After 2022, the annual growth in China will slow down. However the rest of the world will continue to see a growth in renewables.

- IEA has asked governments to prioritise policies that encourage greater investment in solar and wind energy. They must focus on other renewable technologies such as hydropower, bioenergy and geothermal energy too.

- Related to India

-

- India may set new records for renewable energy capacity expansion in 2021 and 2022, since the delayed projects from previous competitive auctions have been commissioned.

- Photovoltaic (PV) capacity addition is expected to be three times in 2021 compared with 2020, as delayed large-scale utility projects become operational.

- The Government of India awarded 27 GW of photovoltaics in central and state auctions in 2020, which is expected to drive growth in solar energy capacity this year and the next.

Image Courtesy:International Energy Agency

Reasons for Decline

- The decline in renewable energy (RE) capacity addition is primarily due to construction delays brought on by the novel coronavirus disease (COVID-19) pandemic.

- It has raised concerns over the financial health of power distribution companies (discom) too. It remains the primary challenge to renewable energy deployment in India.

- In India, the distributed PV expansion (residential installations) remained sluggish due to administrative and regulatory challenges in multiple states.

- The challenges of integrating renewable energy into the grid also acted as an impediment.

Renewable Energy Sector in India

- As on 31st October 2020, India’s total renewable energy installed capacity (excluding hydro power above 25 MW) had reached over 89.63 GW.

- The government has made a commitment that 175 GW of renewable energy capacity will be installed by the year 2022. This includes 100 GW from solar, 60 GW from wind, 10 GW from biomass and 5 GW from small hydro power.

- India’s wind power potential at hub height of 120 meters is 695 GW. The wind power installed capacity has grown by 1.8 times during the past 6.5 years to about 38.26 GW (as on 31st October 2020) and India now has the 4th largest wind power capacity in the world.

- Sector wise details of Installed Capacity from renewables excluding large hydro above 25 MW is as follows:

|

Sector |

Installed capacity (GW) |

Under Implementation (GW) |

Tendered (GW) |

Total Installed/ Pipeline (GW) |

|

Solar Power |

36.32 |

37.10 |

21.21 |

94.63 |

|

Wind Power |

38.26 |

8.99 |

0 |

47.25 |

|

Bio Energy |

10.31 |

0 |

0 |

10.31 |

|

Small Hydro |

4.74 |

0.46 |

0 |

5.20 |

|

Wind Solar Hybrid |

0 |

1.44 |

1.20 |

2.64 |

|

Round the Clock (RTC) Power |

0 |

1.60 |

5.00 |

6.60 |

|

Total |

89.63 |

49.59 |

27.41 |

166.63 |

- India has worked systematically for putting in place facilitative policies and programmes for achieving the goal. The success is mainly attributed to several diverse policy instruments.

Major Programmes in Renewable Energy Sector

- National Solar Mission (NSM)

-

- In January 2010, the NSM was launched with the objective of establishing India as a global leader in solar energy, by creating the policy conditions for solar technology diffusion across the country.

- The initial target of NSM was to install 20 GW solar power by 2022. This was upscaled to 100 GW in early 2015.

- Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan (PM-KUSUM)

-

- An ambitious scheme for providing water and energy security to farmers and enhancing their income by making “Annadata also a Urjadata”.

- Convergence of Scheme with PM-KSY and Agriculture Infrastructure Fund has also been provided for

- For ease of availability of finance the Reserve Bank of India included the three components of the Scheme under Priority Sector Lending (PSL) Guidelines.

- During the budget for 2020-21, the expansion of the scheme was announced to increase the quantity of standalone solar pumps covered under the scheme from 17.5 lakh to 20 lakh pumps and the quantity of solarisation of grid connected pumps from 10 lakh to 15 lakh.

- Atal Jyoti Yojana (AJAY) Phase-II

-

- A Scheme for installation of solar street lights with 25% fund contribution from MPLAD Funds was discontinued from 1 April 2020 as the Government decided to suspend the MPLAD Funds for next two years i.e. 2020-21 and 2021-22.

- However, installation of 1.5 lakh solar street lights sanctioned under the scheme till March 2020 was under progress.

- Solar Parks Scheme

-

- To facilitate large scale grid connected solar power projects, a scheme is under implementation with a target capacity of 40 GW capacity by March 2022.

- Solar parks provide solar power developers with a plug and play model, by facilitating necessary infrastructure like land, power evacuation facilities, road connectivity, water facility etc. along with all statutory clearances.

- So far, 40 solar parks have been sanctioned with a cumulative capacity of 26.3 GW in 15 states.

- Scheme for procurement of blended wind power from 2500 MW ISTS connected projects

-

- The objective is to provide a framework for procurement of electricity from 2500 MW ISTS Grid Connected Wind Power Projects with up to 20% blending with Solar PV Power through a transparent process of bidding.

- Solar Energy Corporation of India Ltd. (SECI) is the nodal agency for implementation of the Scheme.

- SECI has awarded 970 MW of projects under this scheme at a discovered tariff of Rs. 2.99-3.00 per unit.

- Green Energy Corridor (GEC)

-

- To facilitate renewable power evacuation and reshaping the grid for future requirements.

- Inter-state GEC component with target capacity of 3200 circuit kilometer (ckm) transmission lines and 17,000 MVA capacity sub-stations, was completed in March 2020.

- Intra-state GEC component with a target capacity of 9700 ckm transmission lines and 22,600 MVA capacity sub-stations is expected to be completed by May 2021.

- A total of 7175 ckm of transmission lines have been constructed and substations of aggregated capacity of 7825 MVA have been charged.

- To facilitate renewable power evacuation and reshaping the grid for future requirements.

Challenges in the Renewable Energy Sector

- Finance and investment: Gearing up the banking sector for arranging finances for larger deployment goals, exploring low-interest rate, long-term international funding, and developing a suitable mechanism for risk mitigation or sharing by addressing both technical and financial bottlenecks are major challenges.

- Land acquisition: It is one of the major challenges in renewable power development. Identification of land with RE potential, its conversion (if needed), clearance from land ceiling act, decision on land lease rent, clearance from revenue department, and other such clearances take time.

- Technological Barriers: Renewable energy technologies are still evolving in terms of technological maturity and cost competitiveness, and face numerous market related, economic and social barriers.

- Innovation & Seamless Supply: Creating an innovation and manufacturing eco-system in the country; enabling supply of firm and dispatchable power from renewables etc. are issues which need urgent attention.

- Integration to grids: To economically integrate a larger share of renewables with the grid is a tough task.

- Penetration in other sectors: Enabling penetration of renewables in the so called hard to decarbonize sectors is going to be difficult.

- Impact of Covid-19: The COVID-19 pandemic has thrown up tough challenges. The pace of renewable energy projects development and commissioning has been adversely impacted.

Way Ahead

- Focus on domestic manufacturing: There is a need to strengthen the steps to promote domestic manufacturing in the Renewable Energy sector (Atma Nirbhar Bharat Policy). Procurement and use of domestically manufactured solar PV cells and modules has to be mandated for all entities.

- Risk Mitigation & Easing Approvals: The ongoing efforts for mitigating investment risks and easing approval processes need to be strengthened. The State governments have to play a major role in acquisition of land for RE projects.

- Overcoming from Covid-19 crisis: Due to Covid-19, the operation of renewable energy generation plants was declared as an essential service, and a policy for granting extension of time for various renewable energy projects treating the lockdown as force majeure has been put in place.

- Make RE an attractive option: With progressively declining costs, improved efficiency and reliability, renewable energy is now an attractive option for meeting the energy needs across different sectors of the economy. The GOI has been driving a vibrant renewable energy programme aimed at achieving energy security, energy access and reducing the carbon footprints of the national economy.

|

International Energy Agency (IEA)

State of India’s Environment Report

|

Source: DTE