In News: Union Budget has proposed privatisation of two banks in addition to IDBI Bank and General Insurance company.

- It may give the private sector a key role in the banking landscape after 51 years of nationalisation in 1969.

- Currently, there are ten nationalised banks in addition to IDBI Bank and SBI.

Reasons behind the proposal

- Bare Minimum Presence: Government wants to minimise its presence in different sectors where private industry is relatively more competent.

- This market-led approach also reflects in the creation of Asset Reconstruction Company for solving financial crunch.

- Huge losses: Even after years of capital infusion and governance reforms, the health of the public banks have not changed significantly.

- Public banks lag on profitability, market capitalisation and dividend payment record.

- The Government infused Rs 80,000 crore in 2017-18 and Rs 1.06 lakh crore in 2018-19 in public banks through recapitalisation bonds.

- Bank Mergers were less effective: In 2019, 10 banks were merged in 4 which didn’t change the scenario too much. This privatisation drive will compliment those reforms.

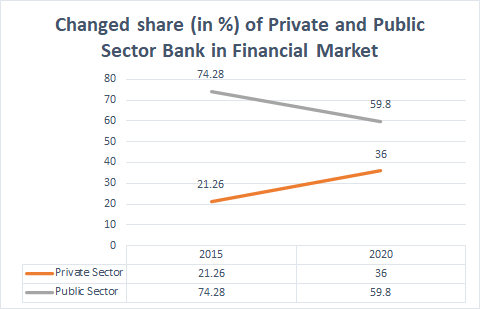

- Increasing Private Bank’s Market Share and Competitiveness

- Private banks’ market share in loans has risen to 36% in 2020 from 21.26% in 2015, while public sector banks’ share has fallen to 59.8% from 74.28%.

-

- Competition heated up after the RBI allowed more private banks since the 1990s.

- They have expanded the market share through new products, technology, and better services, and also attracted better valuations in stock markets. Eg.

- HDFC Bank (set up in 1994) has a market capitalisation of Rs 8.80 lakh crore while SBI commands just Rs 3.50 lakh crore.

- India has 22 private banks and 10 small finance banks.

- Many Committees and Working Groups have proposed privatisation. Few Examples

- Narasimham Committee: Proposed bringing down the government stake to 33%.

- P J Nayak Committee: suggested reducing Government stake below 50%.

- RBI Working Group recently suggested the entry of business houses into the banking sector.

Issues plaguing PSU Banks

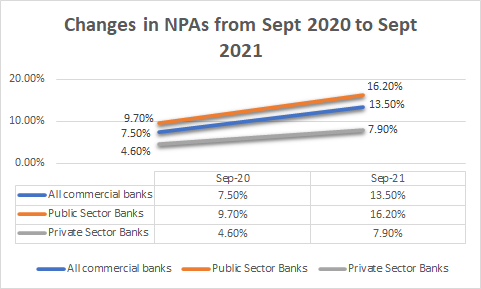

- High non-performing assets (NPAs) and stressed assets.

- After Covid regulatory relaxations are eased, NPAs and loans losses are expected to soar.

- As per RBI’s recent Financial Stability Report, Gross NPA ratio of Public Sector banks may increase significantly.

Nationalisation in Past

Then-Prime Minister Indira Gandhi, who was also Finance Minister, decided to nationalise the 14 largest private banks on July 19, 1969. The prime reasons were

- Socialist Goals: The nationalisation aligned the banking sector with the socialist approach. State Bank of India had been nationalised in 1955 itself, and the insurance sector in 1956.

- Large Number of Private Bank Failures: According to RBI’s History series-

- The number of commercial banks was brought down sharply from 566 in 1951 to 91 in 1967 in order to consolidate commercial banking, which was very fragile.

- By the mid-1960s, Indian banking had become far more viable than ever before.

- Financial Inclusion: The expansion of branches was mostly in urban areas, and rural and semi-urban areas continued to go unserved. (RBI History’s Volume 3 notes)

- No consensus among the changing regime: Even the changing ruling parties didn’t agree on privatisation.

- Disagreements of RBI Governor: former RBI Governor Dr Y V Reddy once said, nationalisation was a political decision, so privatisation too will have to be one.

Is this push for Privatisation a Panacea?

- Concerns regarding Private Bank’s Performance:

- Governance issues:

- ICICI Bank MD and CEO Chanda Kochar was sacked for allegedly extending dubious loans.

- Yes Bank CEO Rana Kapoor was not given extension by the RBI and now faces investigations by various agencies.

- Lakshmi Vilas Bank faced operational issues and was recently merged with DBS Bank of Singapore.

- Under Reporting of NPAs:

- In the 2015 Asset Quality Review by RBI, private sector banks including Yes Bank were found to be under-reporting NPAs.

- Former Axis Bank MD Shikha Sharma too was denied an extension.

- Governance issues:

- Concerns regarding successful disinvestment:

- Initial plan was to privatise four public sector banks.

- The recent target of privatising two banks this fiscal year will act as a case study for the next two.

- May Defeat goal of Financial Inclusion:

- PSBs met their Priority Sector Lending (PSL) targets for agriculture of 18 per cent while private banks and foreign banks failed to meet the targets at 16.2 percent and 16.7 percent, respectively in 2019. (RBI data)

- Distancing from Socialist Goal mentioned in Preamble

- Violation of DPSP under Article 38 which mandates the government to work for the welfare of people via socio-economic justice.

- Private sector banks don’t share the government’s social responsibilities.

Conclusion:

Privatisation is likely to succeed in the present changed scenario. Reasons are as follows.

- Private banks are now more responsible towards the fulfilment of social goals rather than narrow profit motives.

- Private banks are now with more diverse loan portfolios and taking the help of technology to increase their customer base.

But the government should also be cautious and ensure enough safeguards to ensure pre 1960s situations of rampant private banks failures do not re-emerge. Few steps which can be taken are as follows:

- Strengthen RBI’s regulation over PSBs.

- Implementation of Kotak Committee Recommendations on Corporate Governance of Banks.

Source: IE

Previous article

Tholpavakoothu

Next article

Facts in News