YOJANA January 2026

The following topics are covered in the YOJANA January 2026:

Chapter 1: Gender Budgeting and Legislative Measures for Social Equality

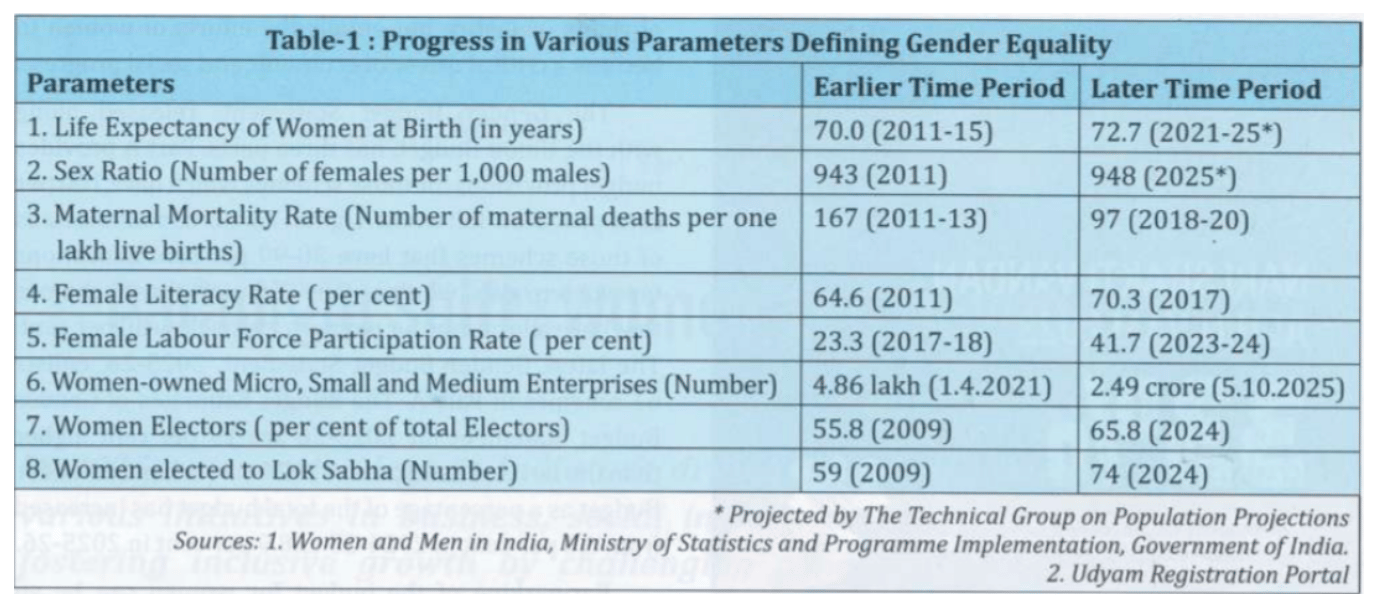

India, now the fourth-largest economy globally, demonstrates that economic growth and social justice are mutually reinforcing. Democracy sets the normative foundation for gender equality, as both are anchored in inclusion, representation and rights-based governance.

- Women constitute over 48% of India’s 145 crore population, making their empowerment not merely a welfare concern but a developmental necessity.

- Achieving equality in health, education, employment, political participation and decision-making requires a robust constitutional, legislative and fiscal framework, which India has progressively strengthened since independence.

From Reforms to Results: Women as Drivers of Growth

- India’s GDP growth of 6.5% in 2024–25 reflects the increasing contribution of nearly 70 crore women to the economy.

- Economic development and social equality are inextricably linked, with gender-inclusive growth yielding multidimensional outcomes such as:

- Higher school enrolment and retention

- Improved maternal health and life expectancy

- Rising Female Labour Force Participation Rate (FLFPR)

- Growth of women entrepreneurship

- Enhanced political representation

- These trends indicate a structural shift from welfare to empowerment, reinforcing women as agents of change rather than passive beneficiaries.

Constitutional Architecture for Gender Justice

India adopted universal adult suffrage at inception, a landmark step compared to many democracies. The Constitution provides a strong affirmative action framework, including:

- Article 14 – Equality before law

- Article 15 – Prohibition of discrimination (enables special provisions for women)

- Article 16 – Equality in public employment

- Article 21 – Right to life and dignity

- Article 23 – Prohibition of trafficking and forced labour

- Article 39(d) – Equal pay for equal work

- Article 42 – Just and humane working conditions

- Article 51A(e) – Renunciation of practices derogatory to women’s dignity

- Articles 243D & 243T – Reservation for women in PRIs and ULBs

- Article 325 – Inclusion in electoral rolls

Political Empowerment through Constitutional Amendments

- 73rd & 74th Constitutional Amendments:

- Mandate minimum 33% reservation for women in Panchayati Raj Institutions and Urban Local Bodies

- Deepened grassroots democracy and participatory governance

- 106th Constitutional Amendment (Nari Shakti Vandan Adhiniyam):

- Reserves 33% seats for women in Lok Sabha, State Legislative Assemblies and NCT of Delhi

- Includes SC/ST women within the quota

- Landmark step towards substantive political equality

Legislative Measures for Safety, Dignity and Equality

India has enacted gender-responsive legislations to address structural and social vulnerabilities:

- Sexual Harassment of Women at Workplace Act, 2013- Ensures safe, dignified and inclusive workplaces

- Revamped SHe-Box (2024) enables online grievance redressal

- Protection of Women from Domestic Violence Act, 2005- Recognizes domestic violence as a violation of human rights

- Dowry Prohibition Act, 1961- Addresses entrenched patriarchal social practices

- Indecent Representation of Women Act, 1986- Regulates objectification in media and advertisements

- Commission of Sati (Prevention) Act, 1987- Criminalizes Sati and its glorification

Labor Law Reforms and Gender Inclusion

The codification of 29 labour laws into 4 Labour Codes (effective 21 November 2025) marks a major governance reform:

- Code on Wages, 2019

- Industrial Relations Code, 2020

- Code on Social Security, 2020

- Occupational Safety, Health and Working Conditions Code, 2020

Key gender-relevant outcomes:

- Simplified definitions and compliance

- Enhanced formalization of women’s work

- Improved social security and workplace safety

- Greater transparency and equal opportunity

- Direct contribution to inclusive growth and productivity

Criminal Justice Reforms and Institutional Support

- Bharatiya Nyaya Sanhita, Bharatiya Nagarik Suraksha Sanhita, Bharatiya Sakshya Adhiniyam (effective 1 July 2024)

- Aim at a modern, efficient and victim-centric criminal justice system

- Nirbhaya Fund (2013)

- Dedicated funding for women’s safety infrastructure

- National Commission for Women (1992)

- Statutory body for rights protection and policy advocacy

International Commitments

- India’s domestic efforts are reinforced by global obligations, including:

- CEDAW

- UN Protocol on Trafficking in Persons

- ILO Conventions on women’s rights

These commitments align India’s gender agenda with international human rights norms.

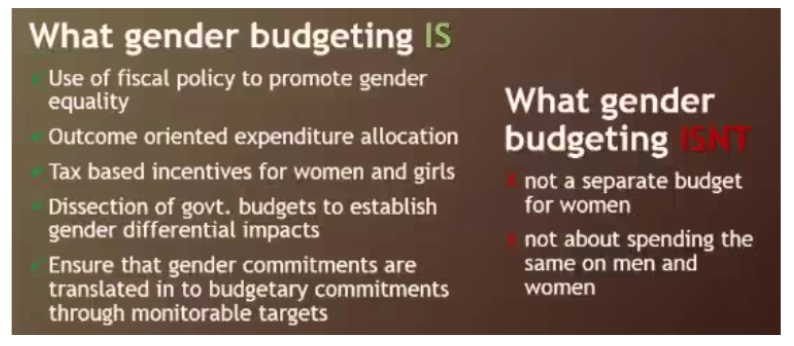

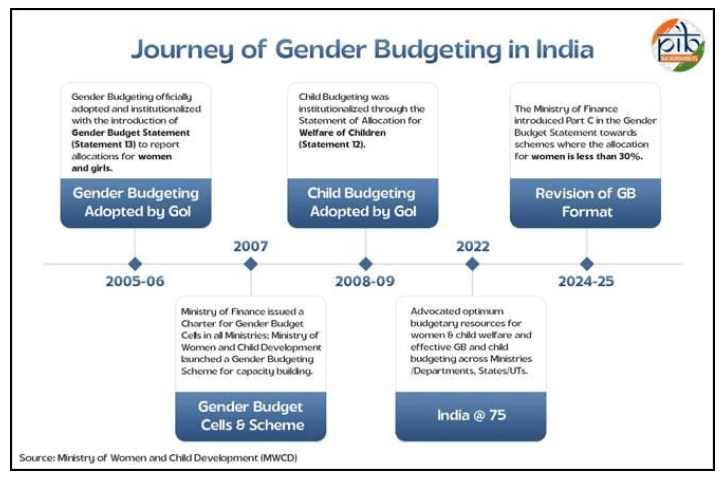

Gender Budgeting: Fiscal Commitment to Equality

The Gender Budget Statement (GBS), released with the Union Budget, institutionalizes gender-responsive public finance:

- Part A: Schemes with 100% allocation for women

- Part B: Schemes with 30–99% allocation

- Part C: Schemes with below 30% allocation

Key Trends (GBS 2025–26):

- 61 schemes in Part A

- 19% increase over Revised Estimates of 2024–25

- Gender Budget rose from 6.8% (2024–25) to 8.9% (2025–26) of total budget

Significance:

- Targeted resource allocation

- Improved accountability and outcome monitoring

- Catalyst for long-term sustainable and inclusive growth

The Output–Outcome Monitoring Framework by NITI Aayog enhances transparency and performance tracking.

The Way Forward: Viksit Bharat @2047

- For India to realise the vision of Viksit Bharat by 2047, especially during Amrit Kaal (2025–2047), women’s empowerment must be social, economic and political.

Key imperatives:

- Higher female literacy and skill development

- Increased workforce participation and leadership

- Breaking systemic and cultural stereotypes

- Transition from formal equality to substantive equality

Conclusion

Women are not merely beneficiaries of development but co-creators of national progress. A combination of constitutional morality, legislative safeguards, gender-responsive budgeting and democratic participation can transform India into a republic of equals, ensuring that growth is not just rapid, but just, inclusive and sustainable.

Chapter 2: Climate Finance

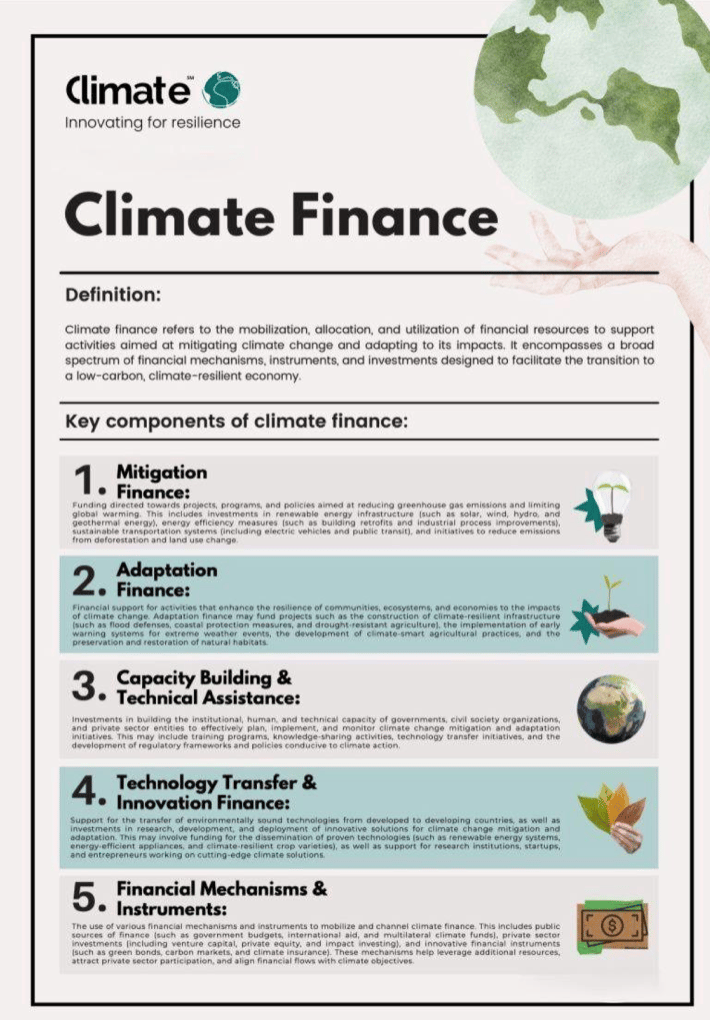

Addressing climate change is no longer limited to environmental ethics; it is fundamentally a question of finance, investment choices and economic governance.

- Mobilizing large-scale public and private climate finance, aligned with developmental priorities, is essential to achieve mitigation, adaptation and resilience goals.

- Ancient Indian wisdom reminds us that nature operates on intrinsic principles, and human excess disrupts ecological balance. In the contemporary context, this translates into the need for sustainable development pathways, integrating SDG-13 (Climate Action) with SDG-2 (Food Security) and SDG-6 (Clean Water).

Understanding Climate Finance

- Climate finance refers to local, national and transnational financial flows—drawn from public, private and alternative sources—that support:

- Mitigation (reducing greenhouse gas emissions)

- Adaptation (coping with climate impacts)

- Resilience-building (enhancing climate preparedness)

Instruments include:

- Grants and concessional loans

- Domestic budgetary allocations

- Green bonds and green deposits

- Blended finance and risk-sharing mechanisms

Climate finance operates on the principle of Common But Differentiated Responsibilities and Respective Capabilities (CBDR-RC).

Global Climate Finance Architecture

International Legal Framework

- UNFCCC

- Kyoto Protocol

- Paris Agreement (2015)

- Article 9: Developed countries to take the lead in mobilising climate finance

- Emphasis on predictability, transparency and balance between mitigation and adaptation

- Alignment of financial flows with low-carbon and climate-resilient development

Major International Climate Funds

1. Global Environment Facility (GEF) – since 1992, financial mechanism for multiple environmental conventions

2. Green Climate Fund (GCF) – established in 2010, world’s largest climate fund, country-driven approach

3. Special Climate Change Fund (SCCF) – supports adaptation in developing countries

4. Least Developed Countries Fund (LDCF) – adaptation support for LDCs

5. Adaptation Fund (AF) – finances concrete adaptation projects

6. Loss and Damage Fund – established at COP-28 (2023), operationalized with World Bank support

Standing Committee on Finance (SCF)

- Enhances coordination, coherence and assessment of climate finance under UNFCCC

Climate Finance and India’s Developmental Vision

India’s vision of Viksit Bharat@2047 integrates economic growth, social equity and environmental sustainability. However, climate finance gaps remain a major constraint.

India’s Climate Commitments

- Enhanced 2030 NDCs

- Net-zero emissions by 2070

- Demand for USD 1 trillion climate finance over the next decade

- Estimated requirement of USD 2.5 trillion by 2030 for mitigation alone

- Additional USD 1 trillion for adaptation (2015–2030)

Currently, less than 25% of India’s climate finance needs are met, largely through domestic public sources.

National Climate Finance Mechanisms in India

National Adaptation Fund for Climate Change (NAFCC)- Established in 2015, NAFCC focuses on climate-vulnerable States and Union Territories by supporting adaptation-oriented projects.

- National Adaptation Fund for Climate Change (NAFCC)- Established in 2015, NAFCC focuses on climate-vulnerable States and Union Territories by supporting adaptation-oriented projects.

- It is aligned with State Action Plans on Climate Change (SAPCCs) and National Action Plan on Climate Change (NAPCC) missions, with NABARD as the implementing agency, ensuring institutional coordination and effective fund utilisation.

- Priority Sector Lending (PSL) for Renewable Energy- Under PSL norms, bank loans up to ₹35 crore for renewable energy are classified as priority sector credit, improving access to finance.

- It covers solar, wind, biomass, micro-hydro and decentralised renewable energy, thereby promoting energy transition, financial inclusion and low-carbon growth.

- Green Bonds and Green Deposits- Green Bonds are debt instruments used to finance environmentally sustainable projects, while Green Deposits channel household savings into eco-friendly investments.

- India’s first green bond was issued by YES Bank (2015). The framework is regulated by SEBI, ensuring transparency, standardization and prevention of greenwashing.

- Sovereign Green Bonds (SGrBs)- Announced in the Union Budget 2022–23, Sovereign Green Bonds mobilize public funds for renewable energy, waste management and sustainable agriculture.

- They enhance India’s climate credibility, deepen green capital markets and attract ESG-oriented global investors.

- Sustainable Finance Group (SFG) – RBI- Established in 2021, the Sustainable Finance Group within the Reserve Bank of India addresses climate-related financial risks and works towards integrating sustainability considerations into monetary policy, banking regulation and financial supervision.

- Network for Greening the Financial System (NGFS)- India, through the RBI, joined the NGFS in 2021, enabling participation in a global network of central banks and regulators focused on climate risk management, scenario analysis and financial system resilience.

- Climate Risk Information System (RB-CRIS)- RB-CRIS is a standardised national database providing information on carbon emission factors, physical climate risks and transition risks.

- It supports evidence-based financial decision-making, risk assessment and climate-aligned lending.

- Climate Change Finance Unit (CCFU)- Established in 2011 under the Ministry of Finance, the CCFU serves as the nodal agency for climate finance.

- It coordinates domestic policies, international climate finance engagement, and interactions with multilateral climate funds and negotiations.

Challenges & Way Forward in Climate Finance

| Challenges | Way Forward |

|---|---|

|

|

Conclusion

Climate finance is the backbone of global climate action. For India, it is not merely about meeting international commitments but about ensuring development without ecological collapse. Instruments such as sovereign green bonds, climate-risk regulation, adaptation funds and sustainable finance frameworks are critical enablers.

Achieving Viksit Bharat@2047 demands that climate finance be treated as a strategic investment in national resilience, not a peripheral environmental expense.

Chapter 3: Microfinance in India

Microfinance has emerged as a critical pillar of India’s financial inclusion architecture, aimed at extending affordable credit to low-income households, small borrowers and vulnerable sections.

- Since the late 1990s, the recognition of microfinance by the Reserve Bank of India (RBI) as a new development paradigm has significantly transformed access to institutional credit among the financially excluded.

- The evolution of a robust regulatory framework for NBFC–Microfinance Institutions (NBFC-MFIs) has ensured that credit delivery to marginalized sections is transparent, borrower-centric and prudentially regulated, thereby supporting India’s broader objective of inclusive and sustainable growth.

Evolution of Microfinance in India

The roots of microfinance in India can be traced to the Self-Help Group–Bank Linkage Programme (SHG-BLP) launched as a pilot initiative by NABARD in 1992. The programme proved successful in:

- Promoting group-based lending

- Enhancing financial and technological capabilities in rural areas

- Reducing dependence on informal moneylenders

In the late 1990s, microfinance gained further momentum when the RBI recognised it as a mainstream financial inclusion tool.

Role of RBI in Strengthening Microfinance

Over the years, the RBI has undertaken multiple initiatives to deepen and strengthen the microfinance ecosystem:

- Vision Document on Financial Inclusion (2015)

- Focus on universal access to basic financial services

- Greater reliance on technology-enabled delivery

- National Strategy for Financial Inclusion (NSFI) 2019–2024

- Measures financial inclusion across three dimensions:

- Access

- Usage

- Quality

Despite rapid expansion, issues such as over-indebtedness, multiple lending and borrower protection necessitated regulatory intervention.

Regulatory Framework for Microfinance

2011 RBI Regulatory Framework (Post Expert Committee)

Key features:

- Small, collateral-free loans to low-income households

- Emphasis on borrower protection and fair lending practices

- Measures against:

- Coercive recovery

- Excessive interest rates

- Multiple lending and over-borrowing

This framework laid the institutional foundation for inclusive credit delivery.

Revised Regulatory Framework (March 2022)

- Uniform, Borrower-Centric Regulation: Introduced by the Reserve Bank of India, the principle-based framework applies to all regulated entities, defines microfinance borrowers as households with annual income ≤ ₹3 lakh, and mandates grievance redressal while prohibiting harsh recovery practices.

- Prudential and Capital Norms: Prescribes Net Owned Funds of ₹5 crore (₹2 crore for North-Eastern Region), a minimum CAR of 15%, and caps Tier-II capital at 100% of Tier-I, ensuring institutional stability.

- Interest Rate and Borrower Protection Safeguards: Imposes a margin cap of 12%, maximum interest rate of 26% p.a. (reducing balance), and processing fee cap of 1%. To prevent over-indebtedness, total loan repayment ≤ 50% of household income, with lending restricted to a maximum of two NBFC-MFIs per borrower.

- Risk Weight Rationalization: While consumer credit risk weights were raised to 125% (Nov 2023), a Feb 2025 review excluded microfinance loans, reducing their risk weight to 100%, recognizing their distinct developmental role and lower systemic risk.

Government & Institutional Initiatives

- Pradhan Mantri Jan Dhan Yojana (PMJDY) – near universal bank account coverage

- Banking Correspondents (BCs) – last-mile credit delivery

- Expansion of brick-and-mortar branches with digital support

- Establishment of:

- Small Finance Banks (SFBs)

- New universal banks

- Bank lending to NBFCs for on-lending included under Priority Sector Lending (PSL)

Performance of the Microfinance Sector (2023–24)

Institutional Spread

- MFIs operating in:

- 730 districts

- 28 States and 8 UTs

Growth Indicators

- Loan accounts increased by 6.1%

- Gross Loan Portfolio grew by 16.2%

- Average loan size:

- ₹46,636 (2023–24)

- Up from ₹41,369 (2022–23)

Asset Quality

- GNPA ratio declined:

- From 10.31% (2022–23) to 8.72% (2023–24)

- Lowest GNPA observed in NBFC-MFIs

- Asset quality concerns persist in:

- SFBs and Non-Financial Entities (limited systemic impact)

Key Challenges & Way Forward

| Key Challenges | Way Forward & Policy Suggestions |

|---|---|

|

|

Conclusion

Microfinance has evolved from a social experiment to a regulated financial instrument, playing a vital role in inclusive growth, poverty alleviation and entrepreneurship development. A balanced approach—combining regulatory oversight, technology adoption, financial literacy and ethical lending practices—is essential to ensure that microfinance remains borrower-centric, sustainable and resilient.

In the journey towards Viksit Bharat, microfinance will continue to act as a bridge between formal finance and the economically vulnerable, provided its growth is guided by prudence, transparency and social responsibility.

Chapter 4: Innovation in Governance

21st-century governance is shaped by technological disruption, socio-economic complexity, climate risks, and rising citizen expectations. India’s living Constitution, rooted in justice, liberty, equality and fraternity, and the Fundamental Duties—scientific temper, inquiry, reform and excellence—mandate continuous innovation in governance.

- This innovation is a precondition for democratic deepening, efficient service delivery and social justice on the path to Viksit Bharat@2047.

Why Innovation in Governance Is Imperative- Traditional efficiency-driven governance is inadequate in the face of demographic change, digital disruption, climate risks and urbanization.

- Contemporary challenges require responsive, inclusive, data-driven and resilient governance systems. Hence, innovation must go beyond technology to reimagine institutions and citizen–state relations, firmly anchored in democratic values, accountability and the rule of law.

Democratizing Policy Frameworks: From Centralization to Cooperative Federalism

The creation of NITI Aayog in 2015 marked a decisive shift from centralized planning to cooperative and competitive federalism, supported by data analytics, performance benchmarking, and decentralized problem-solving.

Aspirational Districts and Blocks

- Aspirational Districts Programme (2018)- Covers 112 underdeveloped districts

- Uses 49 Key Performance Indicators (KPIs) across health, nutrition, education, agriculture, and infrastructure

- Real-time dashboards and rankings incentivise performance

- Aspirational Blocks Programme (2023)- Extends the same model to 500 blocks across 329 districts

- Focus on last-mile governance

These programmes illustrate outcome-based governance, peer learning, and reputational incentives as tools of reform.

Urban Governance and Reform-Oriented Policymaking

Smart Cities as Living Laboratories

The Smart Cities Mission (2015–2025) integrated:

- Citizen participation

- Data-driven decision-making

- Sustainability and resilience

Integrated Command and Control Centers (ICCCs) function as real-time urban “nervous systems”, integrating traffic, safety, water, waste, and emergency services. Studies indicate improved women’s safety and service responsiveness across smart cities.

Structural Economic Reforms

- Four Labor Codes (effective 21 November 2025)

- Consolidated 29 labor laws

- Expanded social security, simplified compliance, and accelerated formalization

- GST, Startup India, PLI 2.0

- Improved ease of doing business

- DPIIT-recognized startups increased from ~500 (2016) to ~1.6 lakh (January 2025)

These reforms reflect policy innovation aligned with growth, welfare, and enterprise development.

Digital Governance and Digital Public Infrastructure (DPI)

- India’s Digital Public Infrastructure (DPI) has emerged as a global governance model, enhancing state capacity, inclusion and service delivery.

- Platforms such as Aadhaar (~140 crore IDs), UPI (20+ billion monthly transactions), DigiLocker (54 crore users), DIKSHA–SWAYAM, and Ayushman Bharat Digital Mission (79.9 crore ABHA IDs) have transformed the government–citizen interface through DBT, transparency and service portability.

- India’s DPI framework has gained international recognition, including in G20 declarations, shaping global digital governance norms.

Citizen Participation and Feedback Loops

Citizen-centric innovation strengthens governance by transforming citizens into co-creators of policy. Platforms like MyGov (2014) and UMANG (2300+ services) enable participation and seamless service delivery, while CPGRAMS has reduced grievance redressal timelines to 21 days (2024) through dashboard-based oversight.

- Tools such as National e-Services Delivery Assessment (NeSDA) institutionalize performance benchmarking, transparency and reputational accountability, improving state responsiveness.

Incentivizing Excellence and Capacity Building

- Innovation in governance is reinforced by incentive and capacity-building mechanisms. The Prime Minister’s Awards for Excellence in Public Administration promote experimentation and outcome-oriented solutions, while Mission Karmayogi shifts civil services from rule-based to role-based, future-ready competencies, emphasizing technology, creativity and citizen-centric governance.

Future Roadmap: Governance 2.0

- Governance 2.0 must be driven by measurable outcomes and behavioral design. Key priorities include AI-enabled performance benchmarking (e.g., 30% reduction in disease forecasting error or pendency), default digital, time-bound services with auto-escalation, and design thinking with behavioral nudges.

- Strengthening collaborative federalism, risk-informed district planning, and institutionalized citizen feedback loops will enable disciplined learning, proactive course correction and scaling of best practices.

Conclusion

As India advances towards Viksit Bharat@2047, innovation in governance has become existential for democracy. Trust—the bedrock of democratic governance—deepens when the state listens, learns and delivers. By integrating technology, citizen participation, behavioural insights, cooperative federalism and outcome-oriented administration, India is strengthening the constitutional ideals of justice, liberty, equality and fraternity, making transformative governance both challenging and inevitable.

UPSC MAINS PRACTICE QUESTIONS

Q1. Why is the traditional model of efficiency-driven governance inadequate in the 21st century? Discuss the imperatives for responsive, inclusive and resilient governance in contemporary India.

Q2. How has India’s shift towards cooperative and competitive federalism strengthened innovation in governance? Illustrate with suitable examples.

Q3. India’s Digital Public Infrastructure has transformed the state–citizen relationship. Discuss its key components and examine its significance for inclusive and transparent governance.

QUICK LINKS