YOJANA January 2024

Chapter 1- Jan Vishwas (Amendment Of Provisions) Act, 2023

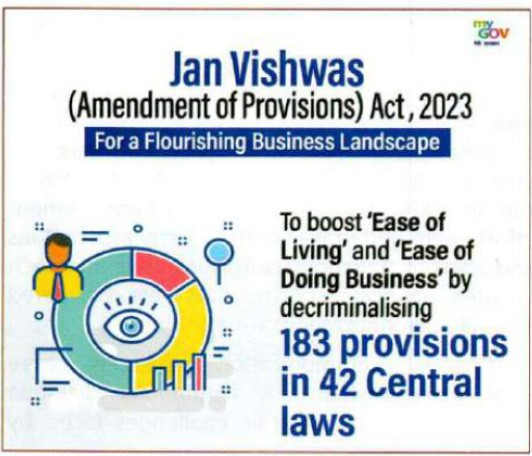

Jan Vishwas (Amendment of Provisions) Bill 2023

- It seeks to redefine the regulatory landscape of the country with decriminalisation of minor offences under 42 Acts to reduce compliance burden and promote ease of living and doing business in the country.

- It was tabled in Parliament by the Union Ministry of Commerce and Industry last year and later referred to a Joint Parliamentary Committee (JPC) for review.

- The JPC presented its report with recommendations to Parliament during the Budget Session.

- As per reports, most recommendations of the JPC have been approved by the Union Cabinet, clearing the way for its passing.

What does the Bill Propose?

- Decriminalising of 180 offences across 42 laws governing environment, agriculture, media, industry and trade, publication, etc.

- It seeks to completely remove or replace imprisonment clauses with monetary fines, to provide a boost to the business ecosystem and improve the well-being of the public.

- The Bill also proposes compounding of offences in some provisions.

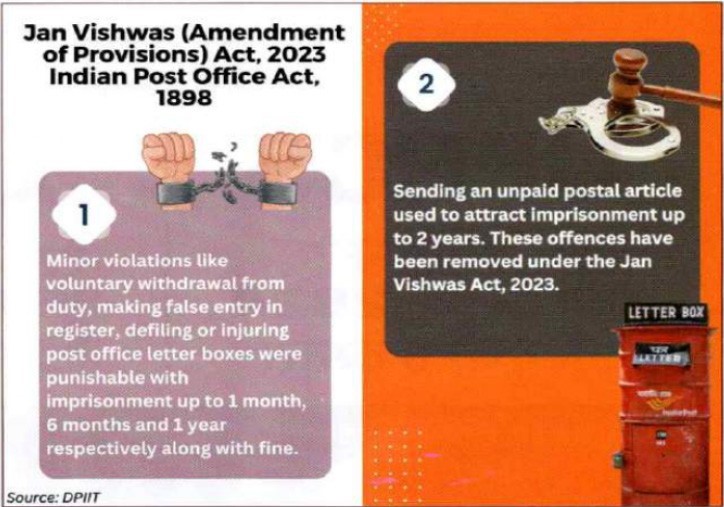

- The Bill removes all offences and penalties under the Indian Post Office Act, 1898.

- Changes in grievance redressal mechanisms and the appointment of one or more Adjudicating Officers for determining penalties.

- A periodic revision of fines and penalties (an increase of 10% of the minimum amount every 3 years) for various offences in the specified Acts.

Some Key Laws in the Draft Legislation:

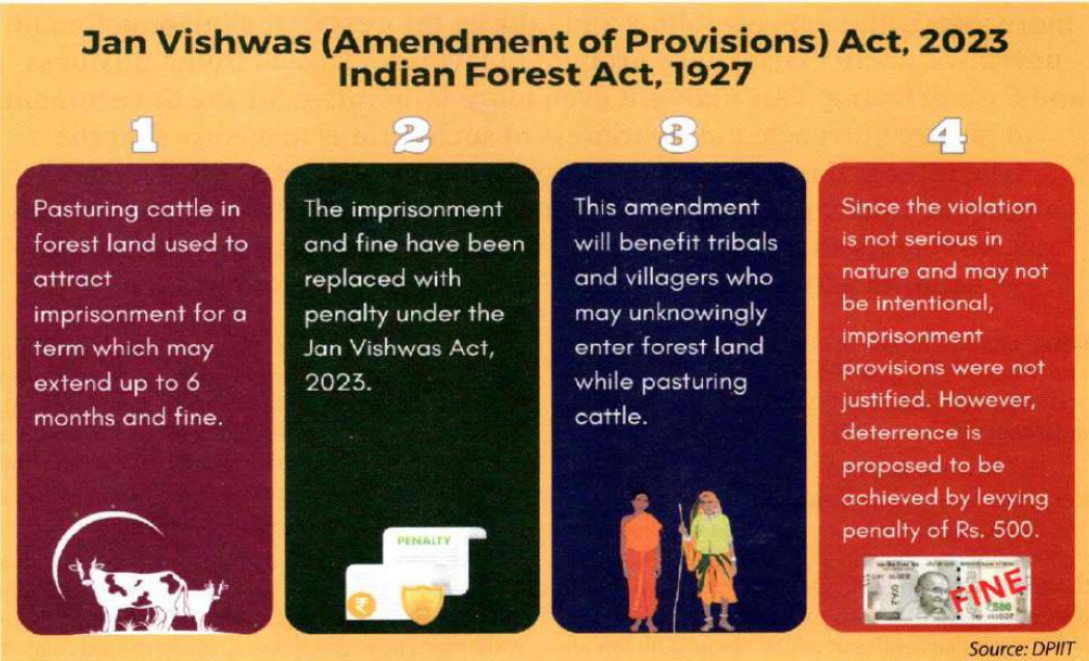

- The Indian Forest Act, 1927

- The Air (Prevention and Control of Pollution) Act, 1981

- The Information Technology Act, 2000

- The Environment (Protection) Act, 1986

- The Copyright Act, 1957

- The Motor Vehicles Act, 1988

- The Railways Act, 1989

- The Cinematograph Act, 1952

- The Agricultural Produce (Grading & Marking) Act, 1937

- The Food Safety and Standards Act, 2006

- The High Denomination Bank Notes (Demonetisation) Act, 1978, etc.

Need for such a Law

- MSMEs are the backbone of the Indian economy and contribute significantly to the GDP.

- For these enterprises to make a shift to the formal sector and generate jobs and income, there must be effective and efficient business regulations in place that eliminate unnecessary red tape.

- Currently, there are 1,536 laws which translate into around 70,000 compliances that govern doing business in India.

- A 2022 report by the ORF on imprisonment clauses in business laws revealed that among the 69,233 unique compliances that regulate business in India, 26,134 have imprisonment clauses as a penalty for non-compliance.

- These excessive compliances have proved onerous for business enterprises, especially MSMEs, creating barriers to the smooth flow of ideas and the creation of jobs, wealth and GDP.

- Moreover, the lengthy processing times for the needed approvals can escalate costs and dampen the entrepreneurial spirit.

Significance of the Bill

- Reducing compliance burden gives impetus to business process reengineering and improves ease of living of people.

- It would accelerate investment decisions due to smoother processes and attracting more investment.

- The Bill is also aimed at reducing judicial burden. As per the National Judicial Data Grid, out of a total of 4.4 crore pending cases, 3.3 crore cases are criminal proceedings. Settlement of a large number of issues, by compounding method, adjudication and administrative mechanism, without involving courts, will save time, energy and resources.

- Thus, the Bill seeks to bolster ‘trust-based governance’.

Concerns

- The monetary fines or penalties are not a good enough attempt at ‘decriminalisation’. Hence, the Bill undertakes ‘quasi-decriminalisation.’

- The blanket removal of imprisonment provision might also remove the deterrence effect of the environmental legislation, especially for large corporations profiteering from the offence.

- Adjudicating Officers may lack the technical competence necessary to decide all penalties under the Air (Prevention and Control of Pollution) Act, 1981 and the Environment (Protection) Act 1986.

- Many offences proposed to be removed in the Bill have nothing to do with its objective of decriminalisation to promote ease of doing business - like theft or misappropriation of postal articles.

Chapter 2- Government E-Marketplace

- Government e-Marketplace is a world-class, robust digital portal that facilitates end-to-end procurement of goods and services by various Central and State Government departments, organisations, and allied public sector undertakings (PSUs).

- It provides a paperless, cashless, and contactless ecosystem for government buyers to directly purchase products and services from pan- India sellers and service providers through a unified online infrastructure.

- It was set up in August 2016.

- It covers the entire gamut of the procurement process, right from vendor registration and item selection by buyers to receipt of goods and facilitation of timely payments.

Need for a Digital Solutions to Public Procurement

- To make this system transparent which was very opaque.

- To make the system faster, easy-to-use and make system corruption free.

- facilitate the Ease of Doing Business without any barriers to entry and establish a competitive marketplace

- to enable the procurement of quality goods and services at reasonable rates.

- The new system was envisioned to replace age-old manual processes that were riddled with inefficiencies and corruption.

Genesis of GeM

- GeM has led to higher process efficiencies, information sharing, improved transparency, reduced process cycle times, and a higher level of trust among bidders.

- It has resulted in greater competition and higher savings.

Growth Trajectory

- Switchover to GeM has likely been one of the largest digital transformation exercises undertaken by any government globally.

- Despite the challenges, the portal has witnessed significant year-on-year growth in terms of the numbers of sellers registered, total procurement made, and cumulative order value transacted through the platform.

- In the first year, GeM recorded a total Gross Merchandise Value (GMV) of ~INR 420 crore. In the following years, transactions conducted through GeM (in terms of order value) grew from aroundINR 38,000 crore in FY 20-21 to INR 1 lakh crore in FY 21-22.

- In FY 22-23, GeM registered an 88% growth, surpassing a historic milestone of INR 2 lakh croreworth of GMV.

- GeM is a category-driven e-marketplace that has a robust listing of more than 11,600 product categories and 300+ service categories.

GeM - Promoting Ease of Doing Business

- GeM as a Facilitator: It connects buyers, sellers, and service providers on a unified platform to facilitate procurement of public goods and services.

- Transformation through Cost Reduction and Efficiency

- Inclusive empowerment of sellers- empowers sellers of diverse background including Women Entrepreneurs.

- Seamless registration process

- Dynamic Goods and Services Platform

- Diverse buying modes- It facilitates procurement through various modes, including direct purchase, L1 procurement, bidding, reverse auction, forward auction, single packet bidding, and push-button procurement.

- Contract Management: GeM auto-generates a contract between buyers and sellers on the basis of specified technical parameters and the details chosen by the buyer, such as delivery period and delivery terms.

- Cashless payments and timely transactions: The platform supports 100% online payments, providing a truly cashless environment.

- Information Visibility: It ensures visibility for MSEs, local sellers, and startups, allowing sellers to indicate the percentage of domestic content of the goods uploaded on the portal, aligning with the ‘Make in India’ initiative.

- Trust-based Rating System

- Demand Forecasting: GeM displays historical procurement data on the platform based on the inputs provided by buyers as part of their annual procurement plan.

- Establishing Price Reasonability: GeM provides buyers with multiple tools to help them ascertain price reasonability.

- Training: GeM provides adequate training materials and support to help users navigate the platform.

- Communication and Support: GeM provides a standardised and single channel for communication with stakeholders.

- Responsive Contact Centre: GeM’s well equipped contact centre, accessible in multiple languages, addresses user queries across various communication channels.

- Dispute resolution features: GeM introduced the Vivad se Vishwas-Il (Contractual Dispute) functionality, a valuable feature for resolving disputes between buyers and sellers.

- AL-ML-Based Decision Support: GeM is in the process of implementing Al/ML-based advanced analytics on GeM, which will help GeM reduce anomalies and frauds.

- GeM Sahay: It is a mobile application that provides frictionless financing for MSEs and startups, allowing them to obtain a loan at the point of order acceptance on the GeM platform.

- Next-Gen GeM Platform: GeM has successfully onboarded a new Managed Service Provider, viz. Tata Consultancy Services, for designing and developing the Next-Gen GeM platform with extensive use of cutting-edge technologies for ease of its users and for bringing in more efficiency and transparency.

Roadmap for the Futures

- Platform has partnered with a leading IT firm to revamp, re-design, and build a new modern solution leveraging new technologies while maintaining the current platform.

- The upgraded platform intends to use advanced Artificial Intelligence and Machine Learning technologies to identify potential frauds, provide improved data analytics to forecast more accurate projections, and improve supply chain management.

- GeM is also expanding its catalogue of ‘Green’ products and services to help the country achieve its net zero carbon emissions commitment.

- The platform is focused on prioritizing the listing and availability of environmentally sustainable products and services by targeting the largest-selling products and services on the portal.

- Conclusion- With improved functionalities, the platform is committed to adapting new-age technologies to transform public procurement with an aim to further enhance user experience, improve transparency, and induce greater inclusivity in public procurement process.

Chapter 3- GST And Ease Of Doing Business

- Goods and Services Tax (GST) is the biggest indirect tax reform since independence to promote ‘One Nation, One Tax, One Market.

- Subsumed numerous Central and State levies such as Central Excise duty, Service tax, VAT, Purchase tax, Entry tax, Central Sales tax, Local body tax, Luxury tax, Octroi, etc.

- It has brought down the economic barriers and paved the way for an integrated economy at the national level.

- In the last six and a half years, the GST tax base has almost doubled from 67.8 lakh to around 1.4 crore and witnessed the highest GST revenue collection of Rs 1,87,035 crore in April 2023.

- GST focuses on reducing compliance, ensuring the free flow of goods across states, harmonizing laws, procedures, rates of tax, common definitions, and interfaces through the Goods and Service Tax Network (GSTN).

- All processes in GST for a business cycle, starting from application for registration, filing of returns, refund application, replying to notices, appeal filing, etc. are completely online, which eliminate the physical interface with the tax officers.

Essential ingredients of ‘ease of doing business are as follows-

- Registration: GST registration is PANbased and state-specific. Any business beyond a threshold of all India aggregates annual turnover of Rs 40 lakh in the case of supply of goods (Rs 20 lakh for specified States) and Rs 20 lakh in case of supply of services (Rs 10 lakh for specified States needs to take GST registration.

- Return Filing: In GST, taxpayers need to file various returns every month, e.g., GSTR-1 for outward supply, GSTR-2A/2B for inward supply, which is auto-populated, GSTR-3B for tax payment, and GSTR-9 is the annual return

-

- the calculation of late fees and interest for delayed filing of returns is being done by the system itself.

- For Ease of Doing Business, the requirement of furnishing an annual return in‘FORM GSTR-9” has been waived off for taxpayers with annual turnover up to Rs 2 crore, and the requirement of furnishing a reconciliation statement in ‘FORM GSTR-9C’ has been waived off for taxpayers with annual turnover up to Rs 5 crore.

- E-Way Bill: It is a document required for the movement of goods, having details such as the name of the consignor, consignee, transporter, point of origin of the movement of goods, and its destination.

- It facilitates faster movement of goods, improves the turnaround time of trucks, increases the average distance travelled, and reduces the cost.

- It resulted in the elimination of state boundary check posts prevailing in the erstwhile tax regime.

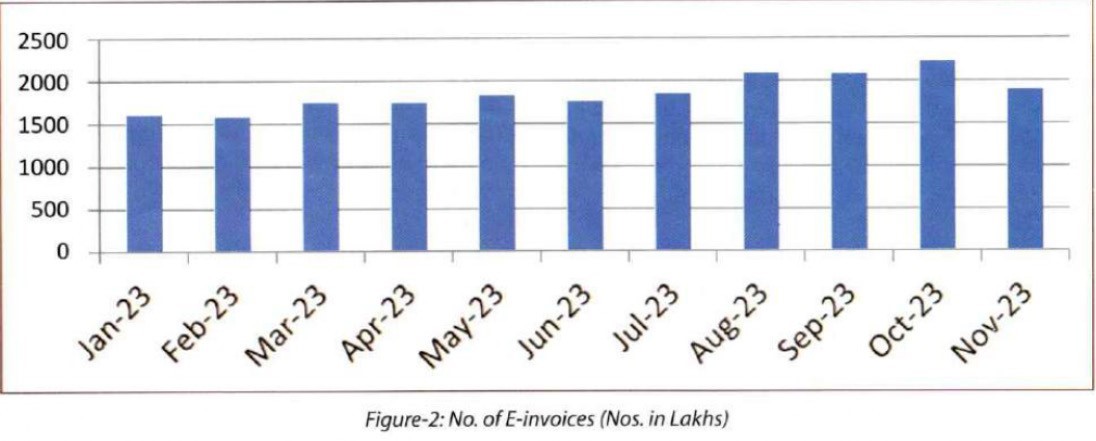

- E-invoicing- It is mandatory for registered persons whose aggregate annual turnover in any preceding financial year is more than Rs 5 crore.

- E-invoice facilitates standardization and interoperability leading to a reduction of disputes among transacting parties, improving payment cycles, reducing processing costs, and thereby improving overall business efficiency.

- Refund: Timely sanction of refunds is essential for the availability of working capital for expansion and modernisation of existing plants and machinery.

- The process of refund in GST has been envisaged as standardised, simplified, time- bound, and technology-driven with minimal human interaction between the taxpayer and tax authorities.

- Exporters are facilitated by the grant of a provisional refund of 90% of their claims within seven days of their application.

The following trade friendly initiatives, have ease compliance in GST-

- Interest-related measure: Section 50 of the Central Goods and Services Act, 2017 (CGST Act) has been amended to provide that interest is required to be paid on the wrongly availed Input Tax Credit (ITC) only when the same has been availed, as well as utilised.

- The rate of interest on wrongly availed and utilised ITC has also been reduced to 18% from 24%, with a retrospective effect from July 2017.

- Refund-related measure: Amendment has been made to the formula prescribed under Rule 89(5) of the CGST Rules for the calculation of refunds for unutilised ITC on account of the inverted rated structure. This would result in a higher amount of refunds on account of the inverted rate structure.

- Measures for Small Taxpayers for Supply through Electronic Commerce Operator (ECO): To facilitate small taxpayers in making supply of goods through ECOs, and to provide parity among intra-state offline and online supply of goods, a waiver of the requirement of mandatory registration up to threshold turnover.

- Measure for enhanced cash flow: Provision has been made to provide for the transfer of unutilised balances from the electronic cash ledger of a registered person to the electronic cash ledger of CGST and IGST of a distinct person having the same PAN.

- Facilitation to Exporters: UPI and IMPS have been provided as additional modes for payment of GST to facilitate taxpayers and further encourage digital payment by amending Rule 87(3) of CGST Rules.

- Option for withdrawal of an application of appeal up to a certain specified stage- provision for automatic restoration of provisionally attached property after one year; decriminalisation of certain sections of GST, etc. are additional measures that were undertaken for ease of doing business.

- The taxation system of a country is one of the key criteria used to assess countries in the World Bank’s Ease of Doing Business Index.

- Due to myriad economic and tax reforms, India steadily climbed up this index ladder from 142 in 2014 to 77 in 2018 and further to the 63 position in 2019.

Conclusion and Way Forward

- The Department for promotion of industry and internal trade (DPIIT)’s Business Reform Action Plan, 2020 also indicates a significant enhancement in the ease of doing business across the country.

- Despite initial hiccups while adopting the new tax structure, GST is widely regarded as a paradigm shift and an enabler for ease of doing business and improved supply-chain efficiency.

- GST regime has its own shortcomings, but the positives outweigh the negatives, and this, coupled with the sincere efforts of the GST Council to make it more equitable and effective, has made this reform a roaring success.

Chapter 4- Decriminalisation India’s Continued March Toward Ease Of Doing Business

- Jan Vishwas (Amendment to Provisions) Act, 2023 strives to strike a balance between the severity of the violation and the gravity of the prescribed punishment.

- The key objective of the JV Act is to decriminalize and rationalize offences to enhance trust-based governance for ease of doing business and living.

- While doing so, it also helps to de-clog the Indian judicial system so that it can focus on more burning matters.

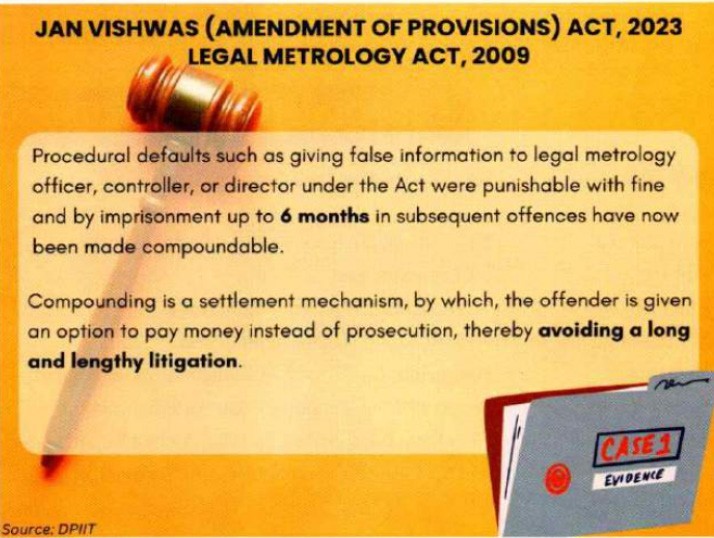

- Some of the Acts with great implications for ease of doing business in the country include the Pharmacy Act of 1948, the Copyright Act of 1957, the Patents Act of 1970, the Environment (Protection) Act of 1986, the Motor Vehicles Act of 1988, the Trade Marks Act of 1999, the Information Technology Act of 2000, the Prevention of Money Laundering Act of 2002, the Food Safety and Standards Act of 2006, and Legal Metrology Act of 2009.

- Complete decriminalization of many offences promises to save corporations from going through rigours of criminal trial before being convicted for an offence that is now punishable merely with a ‘penalty’, meaning that court prosecution is not required to administer punishments.

- Confederation of Indian Industry has always been a strong advocate of moving towards a system of self- governance where criminal provisions exist only as an exception for serious offences, whereas for minor violations, it recommended for the replacement of ‘imprisonment’ and/or ‘fine with penalty; which is an executive decision.

- JV Act offers huge potential to save businesses from the strenuous and time-consuming process of legal trials and the consequent build-up of case pendency with an already overburdened judiciary at the same time.

- In sum, the decriminalization journey, which started with amendments to the Companies Act, as gained momentum with the JV Act.

- Conclusion- However, a fine balance between ease of doing business and adequate deterrence for serious contraventions needs to be ensured so that responsible decriminalization is achieved rather than blanket overhauls.

Chapter 5-Delicate Balance Regulatory Enforcement & Favourable Business Environment

- One of the most noteworthy aspects of the Jan Vishwas (Amendment to Provisions) Act is its substantial modification of penalties.

- It replaces imprisonment with a system of higher fines/penalties for various offences.

- This shift aims to create a more effective deterrent against violations, ensuring a stronger enforcement mechanism without disrupting businesses.

- FICCI has formulated some basic general principles of decriminalization while submitting suggestions and these are as follows:

- Directors (or at least independent directors) not to be held liable for operational non-compliances.

- No criminal liability for technical errors/lapses only financial penalties.

- No criminal liability for first-time offences under the majority of the laws.

- Graded penalty system as a deterrent for subsequent non-compliances

- Establishing mens rea for offences committed.

It is suggested that:

- For technical lapses/errors such as maintenance of records, filing of returns, etc., only monetary penalties are to be there, which could be graded for subsequent lapses.

- First-time offences should only have monetary penalties, which could be enhanced further to create a deterrent effect.

- Provision for compounding an offence where otherwise there is compliance with the law.

- Criminal prosecution for minor offences leads to disruption in business operations as the focus shifts to defending prosecution.

- Provisions under the Occupational Safety, Health, and Working Conditions Code - Sections 94, 96 and 97 have been completely decriminalized with enhanced penalties.

- Legal Metrology Act, 2009- While Vishwas Act addresses many provisions, Section 36 related to the penalty for selling nonstandard packages was not included in the decriminalization. There is a need to remove imprisonment provisions and have only graded fines and monetary penalties for this provision as well.

- Rationale: Currently, packaging regulation provides opportunities for legal metrology inspectors to issue notices on frivolous grounds of minor/technical non-compliance. For example, even a difference in font size makes a package nonstandard, even though it is readable.

- Labour Codes- Some of the new codes enacted have retained the provisions of criminalisation. For instance, the Occupational Health, Safety, and Working Conditions Code 2019 under Sections 102 and 103 prescribes enhanced penalties involving both imprisonment and fines.

- Way Forward- It is important to address the issues of decriminalization at the State level. Due to the existence of overriding Central Legislations, State Governments are unable to decriminalize minor criminal provisions. We need a targeted approach for the examination of such identified Central Acts that will have profound effect through the subsequent decriminalization of all subordinate State Legislations.

Mains Practice Question: - (In Around 250 Words)

Q1. What are the implications of Jan Vishwas (Amendment to Provisions) Act, 2023 recently passed by the Parliament? How will this help in promoting Ease of Doing Business in India ?

Q2. What is GeM? What is the aim of this initiative? How will it affect the government system of purchase of goods and increasing transparency in the system?

Q3. Discuss various factors that has led to rise in india’s ease of doing business ranking. Do you think this would help drive Indian economic growth?

QUICK LINKS